Startup cycle: how (in general) venture investment works

Hello, Habr! I recently released a book on legal support for venture capital investments and IT businesses. I am not going to sell the book, so I am happy to post one chapter for members of the habrasociety.

The book "Startup Law":

- Startup vs. businessman

- Choose a form

- registration

- Corporate governance

How a company is built legally - Current work

Contracts and how they work

How to check an open source partner - Taxes

What pays IT-business in Russia? - Governmental support

- Startup cycle

How (in general) venture investment works - Venture deals

- Venture capital funds

- Intellectual property

- Offshore and FEA

Advantages and pitfalls of offshore

At work (I am a lawyer and a teacher), I often have to explain to students how venture investment works and why an investor should invest in an IT business, in fact, without getting anything in return. Therefore, I tried to explain the nature of the venture phenomenon. Of course, this is still a theory, in practice there are a lot of nuances and details, but as a general guide, I think it fits. If something remains unclear, ask in the comments, I will explain as much as possible ;-)

Each startup has its own characteristics, depending on the field of activity underlying its intellectual property and even on the number of founders. However, if you expand the development of a startup into several milestones, they will be common: prototype development, market entry, rapid growth, scaling, transition to the stage of smooth growth.

What else unites startups?

A startup differs from a “regular” business in that it is based on innovation - a special innovation that allows creating a new product, service, business process. Thanks to innovation, a real startup does not compete with other companies, but creates a new, completely open market.

As you remember, in 2007 Apple offered users a new mobile phone format - without a keyboard and with a touchscreen, as well as a special ecosystem for mobile applications that can be installed on the phone.

The iPhone was not a wholly competitor for the then prevailing Nokia, Motorola and other keyboard models. He had certain shortcomings, but at the same time he offered a much more extensive functionality, first of all - as a device for mobile Internet surfing. As a result, Apple created a new market, and push-button telephones turned into a narrow (niche) product.

This is the essence of a startup: the innovation laid in its foundation opens a new market that has not yet been occupied by anyone. Thanks to innovation, a startup can grow extensively. Unlike, for example, stalls with shawarma, whose market has already been established, the market for innovative products is not yet full. Therefore, a startup can occupy it completely (as Europeans occupied the American Indian market with their axes, beads and blankets).

For this reason, a startup is growing very fast, in particular in price. Investing in a “regular” business, the investor earns profit; investing in a startup, primarily on the growth of the share value.

Timur from the city of Zelenograd decided to open a pizzeria. He already had experience in the restaurant business and knew recipes for good pizza, but did not have money for the initial rental of premises and the purchase of equipment. Then Timur invited his friend Arthur to join the project as an investor, that is, to invest money. Arthur offered Timur 5 million ₽, and in return wanted 75% in the company (and, accordingly, in its profit).Now let's see how investing in a real startup works .

Why did Arthur ask for such a large share? A traditional valuation model works here. Suppose the average profit of a pizzeria of this size with proper management is 1 million ₽ per year. Given the fact that Arthur will not receive all the profit, and it will also take some time to “promote”, the pizzeria will pay off in 7-8 years. So, in fact, Arthur will invest his money at 12-14% per year, and this does not take into account the risks inherent in entrepreneurship. If the pizzeria goes bankrupt, Timur will not lose anything, but Arthur will lose 5 million ₽.

Can Arthur count on what he will earn due to the growth in the value of his share? No, because its share will grow only with the business itself. And after a year, and after five years, 75% of the pizzeria will cost about the same 5 million ₽. In addition, it will not be easy to sell the institution, and it is difficult to scale it in Zelenograd, since there are plenty of pizzerias there.

Kolya came up with a brilliant application that allows you to create beautiful pictures using neural networks. Pictures are successful - they look as if they were drawn by a real artist. Kolya made the site, but due to a weak server he manages to process only one picture per minute. Users want to process much more.

Having assessed the situation, Tanya - Kolina, a classmate and co-founder of the venture capital fund - offered investments: 5 million rubles to a new server, a new site and advertising. In return, Tanya asked for 25% in Colin's company.

Why did Tanya ask for such a small fraction? The fact is that Colin's business is promising. It can bring millions if you process a lot of pictures and take money for it. Therefore, the task is to maximize the Colin service: buy servers and conduct an advertising campaign.

When the explosive growth slows down, Tanya will be able to put pressure on Kolya to introduce monetization mechanisms on the site: show ads, charge for new pictures, etc. Then the startup will turn into an ordinary business that brings good money. Alternatively, Tanya can simply sell her share - unlike a pizzeria, this business is much more profitable, and over time its share will cost more. If she anticipates the time of sale (a little before users lose interest in Colin's technology), she can find the greedy investor who is like her and get the maximum for her share.

How a startup grows

Development of a startup is traditionally divided into several stages, which generally mean the path from a small company with innovation at the forefront to a large multinational corporation like Facebook. Of course, not every startup goes through all stages: most of the projects go bankrupt before reaching the second.

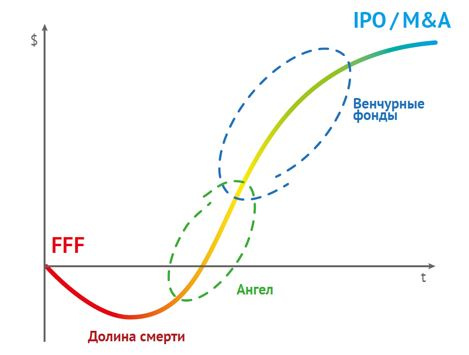

The blame for this is the lack of funding, lack of experience or the fundamental impracticability of the project. At the middle stages of development, startups are absorbed by large competitors (to mutual benefit). All stages go through only a few to the end. Here is a graph illustrating the stages of startup growth.

This graph is called the “J-curve" (J curve), guess why?

Development

At an early stage, an entrepreneur creates a prototype and develops a business plan. Usually this stage is associated with going beyond the scope of primary financing (own money or money of relatives). Therefore, funds are needed to refine the investment product to the level of the applicable prototype.

If the entrepreneur continues to develop the product at his own expense, the development phase may be delayed. This phenomenon is known as garage business. For example, the “garage entrepreneur” was Henry Ford, who, working as chief engineer at the Edison plant, in his spare time from 1891 to 1901. worked on a prototype car.

The more development is delayed, the less prospects a startup has - at any moment someone more efficient can occupy its niche in the market. And vice versa, the faster the startup captures the market, the more significant profit it will receive (and the more it will increase in price). This pattern attracts venture capitalists like Tanya, who exchange money for shares in startups.

When a startup can attract investments depends on two factors. On the one hand, the sooner this happens, the more chances there are to occupy the market. In addition, investing at the initial stage means getting a larger share for the same money. On the other hand, the longer the startup exists, the clearer the technological prospects of the innovation laid in its foundation. Early investment is accompanied by great risks, because the more conceptual the innovation, the more difficult it is to assess its real applicability and usefulness.

Thus, investors are trying to achieve a balance between the risks of technological uncertainty of the project and the losses associated with the delayed entry of the innovation into the market.

In the early stages, not all investors invest: usually seed funds, accelerators and business angels. Larger investors - venture funds and private equity funds - are waiting for the next stages, since in the early stages the transaction costs associated with the assessment, legal and accounting verification of a startup are too high in relation to the price of the investment transaction itself.

Investing

Buying a stake, an investor cannot accurately evaluate the innovation that forms the basis of a startup. The very essence of innovation implies the lack of empirical data, on the basis of which it is possible to assess its prospects. Therefore, investing in a startup, investors get back not a fixed profit, but a share in the company, thus securing their remuneration depending on the overall growth of the startup.

The investor increases the return on his contribution by launching the startup on the market as soon as possible. Due to the cost of extensive growth, a scalable and growing startup usually has no profit (there is a “cash burn” effect). Therefore, startup investors do not receive dividends, but they are not needed either: venture investors expect to receive profit not from dividends, but from the sale of their shares.

When does an investor sell his stake? This point depends on several factors. Ideally, when the market is completely covered (startup will reach the limits of scaling). In some cases, the investor sells his share earlier due to the requirements of the fund and internal restrictions (this will be discussed in the next chapter).

If a startup development strategy involves stage-by-stage scaling (for example, entering the market of a city / country / region), one can attract venture financing several times in ever-increasing volumes. These rounds of investment involve a different amount of invested funds, different financing conditions and different guarantees for investors.

Each arrival of a new investor is an important event for startup participants, because it has not yet become public and its shares cannot be sold on the stock exchange. If one of the participants wants to sell his share, then the easiest way to do this is with the arrival of a new investor.

If a startup has completely occupied the market and its development has stopped, then new investors are not in a hurry to enter it, because their shares will not grow as fast as we would like. In this case, investors holding shares can return their investments due to:

- selling shares to founders if they have enough money (LBO);

- startup takeover by a larger holding (M&A);

- public offer (placement on the stock exchange) of start-up shares (IPO).

After venture investors exit, the startup turns into a “traditional” company with its market share, makes a profit and pays dividends. Investors are looking for the following startups.

Investor and startup.

The founder’s relationship with the investor is a partnership, which in most cases leads to mutual benefit. However, we must not forget that the interests of partners differ. The investor seeks to maximize profits, and the startup is self-fulfilling as the founder of a large company. This often causes conflicts between them.

For example, a conflict may arise when evaluating a company. A startup is based on innovation - it is an asset that, in principle, cannot be accurately estimated, especially in the early stages. Therefore, an entrepreneur who buys a share in a startup, always seeks to underestimate, and a startup to overestimate. Partially, the problem is solved by the mechanisms of post-investment adjustment of shares (ratchet and convertible loan, we will discuss them a bit later).

Let me remind you once again that startups are non-public companies, their shares are not publicly traded and do not have universal market value. In addition to problems with valuation, this makes the startup shares illiquid: the founder and early stage investors will not be able to get rid of the share if no one wants to buy it. At the same time, participation in a startup, albeit highly praised, does not bring profit by itself.

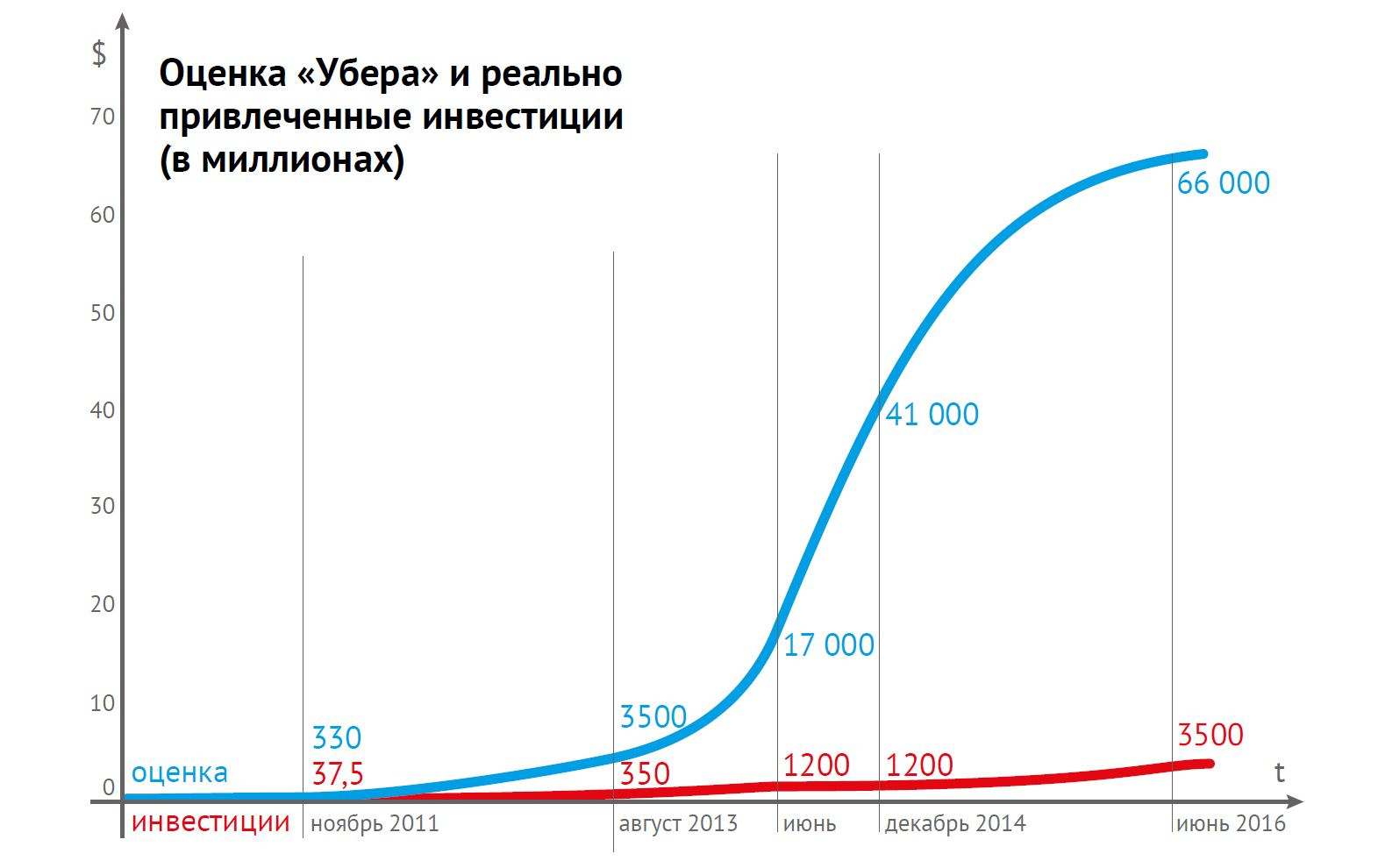

Together, this forms a “valuation phenomenon”: a startup can be valued extremely highly, up to billions of dollars. At the same time, the actual inflow of money into it will be an order of magnitude smaller, and the founders will not receive anything at all, since all investments will go “to growth”.

So, the Uber service is considered to be the most expensive startup in the world:

“Uber Technologies' mobile taxi call service raised $ 2.1 billion in investments in the next round of financing,” Bloomberg reported, citing sources familiar with the company's reporting.

American Forbes cites a valuation of $ 68 billion: the publication managed to get a copy of the statements, from which it follows that in the framework of round G, more than 43 million new shares were issued at a price of $ 48.77 per share. Thus, the status of the most expensive startup in the world has strengthened behind the service. ”

What happened Uber needed new means: for example, in order to enter the Singapore market or start developing an unmanned vehicle; in short, to do something that will increase the hypothetical expectations of future investors.

There were several investment (venture) funds that are ready to give the company money for these projects in exchange for a small share, which they will later resell. For Uber, these investments will be at least the seventh in a row (G is the seventh letter of the alphabet).

Uber issues 43 million shares and sells them to an investor at $ 48.77 apiece. Accordingly, Uber’s assets are increasing by approximately $ 2.1 billion (48.77 x 43 million) - that is the amount of money that investors commit to transfer.

“Investors estimate Uber at $ 68 billion” (in this case, we are talking about post-money valuation, that is, after investing). This means that for the purchased 43 million shares ($ 2.1 billion), investors will receive a 3% stake in Uber:

Thus, a company’s valuation is an extrapolation of the price that investors pay for a small percentage of the company to all 100% of its shares. The amount of $ 68 billion in question, Uber did not receive and most likely will never receive. This is a speculative amount, which is actually confirmed only by 3%.

So, $ 68 billion is:

- not the amount for which Uber can be sold or bought;

- not the amount that Uber has or will ever have;

- not the registered capital of Uber.

A graph illustrating the difference between Uber’s valuation and its real capitalization.

Another example to pin:

Vasya created a startup in the form of a joint stock company. Its authorized capital is 1 million shares with a nominal value of each 1 kopeck, totaling 10 thousand ₽.

A week later, Vasya asked his father to invest in a startup $ 500, offering for this one share. Father took pity on him and agreed: he bought one share for $ 500.

Now Vasya can honestly tell reporters:

- that investors valued his startup at $ 500 million (1 million shares x $ 500);

- that his startup for the week grew by about 3 million times (from 10 thousand ₽ to $ 500 million), which will give a result of 15.6 billion% per annum for future investors.

But you and I know that in fact Vasya just gave $ 500.

For those who do not want to wait for the publication of the remaining chapters on Habré - a link to the PDF of the full book is in my profile.