How Apple shares behave after the release of new devices

- Transfer

After a certain number of financial quarters with predictable results, Apple surprised with its sales figures, which were 3.74% higher than expected [the original article was published in the 2nd quarter of 2014 - approx. transl .]. This may not seem so important, but since the company introduced a new forecasting technique in the first quarter of last year, the announced revenue of the company exceeded the previously established limit by about 1%.

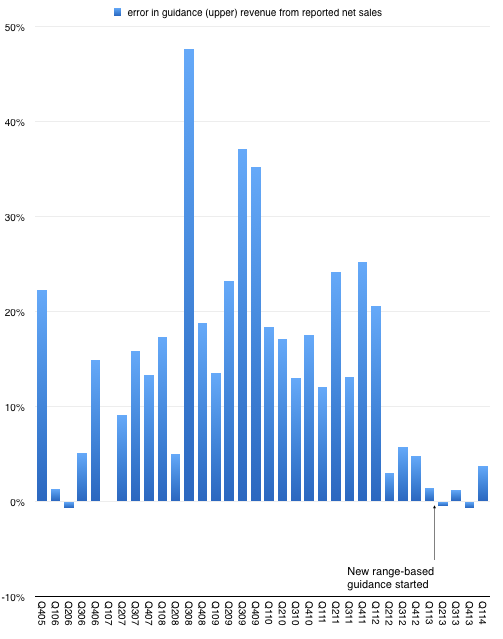

This is in stark contrast to the values of previous years. Below is a graph that shows the “error” in the forecast as a percentage difference between announced sales and projected. [1] Clicking the image will open in full size.

So, until the last quarter, we mistakenly believed that the forecast with almost perfect accuracy determines the future of the company. As I wrote on Twitter, because of this, making forecasts for Apple has lost its excitement. All that analytics needed to do was take the growth indicators of the main product, which would allow them to reach the estimated sales volume, and then subtract the operating expenses (the indicators of which are kindly provided by the company) and the tax rate (also kindly provided) to get the amount of profit. The only hitherto unknown value in determining earnings per share is the number of shares outstanding. [2]

Knowing Apple, I can say that the average selling price is also very rigidly fixed, so that the degree of freedom of analysis became extremely limited.

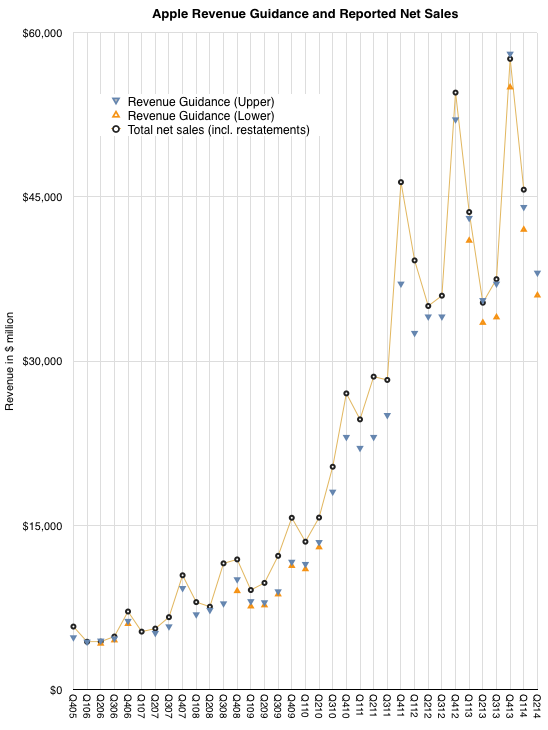

But at the moment when it seems to you that you understand how the system works, it changes. The company surprised with the results of the activities of third-party analysts. The graph below shows the estimated range and actual revenues. [3]

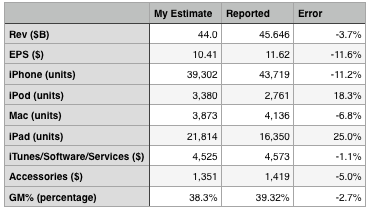

The answer seems to be that iPhone sales have improved. The following table displays my expectations, which were built in accordance with the profitability indicator in the upper part of the forecast range. Regarding supply / sales, I underestimated the iPhone and Mac, and also overestimated the iPad and iPod. I definitely rated iTunes and underestimated the sale of accessories by 5%. Also, by and large, I very closely determined the level of profitability, however, I indicated 1 point less in terms of gross profit. The conclusion was that the unexpected level of income and profits can be attributed to the significant outperforming dynamics of iPhone sales, which could compensate for the less significant failure to meet planned targets for the iPod.

IPhone sales grew by 14% - this was enough to offset the drop in iPad sales by 13% and allow total revenue to grow by 5%. Since the company did not expect a growth spurt, these 5% were a big surprise.

One might ask if a 14% increase in iPhone sales will result in significant changes in the long-term product development strategy. This is a difficult question. The way the iPhone is positioned makes it successful in the premium segment of the market, but does not put it in competition with an estimated 80% of the market, which, apparently, are formed from the point of view of lower prices.

Still, let's not forget that pricing correlates with the market, but is not determined by it. Making a purchase decision is a complex process, and price is just one of the aspects that influence that decision. But there are many other factors. Availability of goods, communication channels, service, brand - all this matters. The mistake of many analysts is that they believe that the price and only the price affects the behavior of the buyer. This may be the case with respect to the commodity, but let me remind you that these products are new, and have recently begun to use them, and the perception of their value has changed rapidly. Buyers adhere to a learning curve in terms of discovering use cases and product value.

We don’t know where exactly on the learning curve is the iPhone in a particular region, which means that we can still expect a surprise in the dynamics of its growth.

Notes:

The link contains an interview with Horace Dediu about surprises in the market after the release of the new iPad that he gave to Bloomberg reporters in October 2014: www.bloomberg.com/video/apple-s-ipad-unveil-were-there-any-surprises-bqKlwc4sSqCSupwehzbsJA .html [en].

Related posts and links:

PS If you notice a typo, mistake or inaccuracy of the translation - write in a personal message, and we will quickly fix it.

This is in stark contrast to the values of previous years. Below is a graph that shows the “error” in the forecast as a percentage difference between announced sales and projected. [1] Clicking the image will open in full size.

So, until the last quarter, we mistakenly believed that the forecast with almost perfect accuracy determines the future of the company. As I wrote on Twitter, because of this, making forecasts for Apple has lost its excitement. All that analytics needed to do was take the growth indicators of the main product, which would allow them to reach the estimated sales volume, and then subtract the operating expenses (the indicators of which are kindly provided by the company) and the tax rate (also kindly provided) to get the amount of profit. The only hitherto unknown value in determining earnings per share is the number of shares outstanding. [2]

Knowing Apple, I can say that the average selling price is also very rigidly fixed, so that the degree of freedom of analysis became extremely limited.

But at the moment when it seems to you that you understand how the system works, it changes. The company surprised with the results of the activities of third-party analysts. The graph below shows the estimated range and actual revenues. [3]

So what happened?

The answer seems to be that iPhone sales have improved. The following table displays my expectations, which were built in accordance with the profitability indicator in the upper part of the forecast range. Regarding supply / sales, I underestimated the iPhone and Mac, and also overestimated the iPad and iPod. I definitely rated iTunes and underestimated the sale of accessories by 5%. Also, by and large, I very closely determined the level of profitability, however, I indicated 1 point less in terms of gross profit. The conclusion was that the unexpected level of income and profits can be attributed to the significant outperforming dynamics of iPhone sales, which could compensate for the less significant failure to meet planned targets for the iPod.

IPhone sales grew by 14% - this was enough to offset the drop in iPad sales by 13% and allow total revenue to grow by 5%. Since the company did not expect a growth spurt, these 5% were a big surprise.

One might ask if a 14% increase in iPhone sales will result in significant changes in the long-term product development strategy. This is a difficult question. The way the iPhone is positioned makes it successful in the premium segment of the market, but does not put it in competition with an estimated 80% of the market, which, apparently, are formed from the point of view of lower prices.

Still, let's not forget that pricing correlates with the market, but is not determined by it. Making a purchase decision is a complex process, and price is just one of the aspects that influence that decision. But there are many other factors. Availability of goods, communication channels, service, brand - all this matters. The mistake of many analysts is that they believe that the price and only the price affects the behavior of the buyer. This may be the case with respect to the commodity, but let me remind you that these products are new, and have recently begun to use them, and the perception of their value has changed rapidly. Buyers adhere to a learning curve in terms of discovering use cases and product value.

We don’t know where exactly on the learning curve is the iPhone in a particular region, which means that we can still expect a surprise in the dynamics of its growth.

Notes:

- The upper edge of the range in those quarters where the range of oscillation is given.

- The company itself cannot know what the number of shares in circulation will be, since their purchase during the quarter is unplanned.

- The next quarter is also taken into account.

The link contains an interview with Horace Dediu about surprises in the market after the release of the new iPad that he gave to Bloomberg reporters in October 2014: www.bloomberg.com/video/apple-s-ipad-unveil-were-there-any-surprises-bqKlwc4sSqCSupwehzbsJA .html [en].

Related posts and links:

- Statistics: why you should not buy Apple shares after the release of the new iPhone

- How to buy stocks of IT companies before, during and after an IPO

- Alibaba IPO: what investors will actually buy

- Stock Market Analytics

PS If you notice a typo, mistake or inaccuracy of the translation - write in a personal message, and we will quickly fix it.