Why invest in unprofitable companies?

In 2018, more than 80% of companies listed on the stock exchange were unprofitable. But investors continue to invest in them, and we at United Traders continue to offer them as investment ideas that you can earn. Why is that? We are telling.

But first, what it is. IPO (Initial Public Offering) - an initial public offering of shares. This is the process during which the company offers to buy its shares to an unlimited circle of investors, that is, it becomes public. To make money on an IPO, you need to buy shares before they are placed on the exchange, choosing a company whose shares will increase in price and sell them after three months after the placement (Lock-up period lasts for three months when shares cannot be sold by the rules of the exchange).

Investment strategies differ when the investor plans to make a profit. For example, the buy-and-hold strategy is long-term: we expect that we will make a profit in a few years, therefore, when evaluating, we look at the forecast of the fair value of the company and use the cash flow discount method (DCF approach).

The horizon of investing in IPOs is several months, so we evaluate the company in terms of short-term demand. In this situation, increased investor interest is the determining driver of the stock price at the offering, and the exit multiple approach is the most suitable valuation method.

According to our studies, the most significant factors in evaluating a company by a comparative method are 2 indicators - the amount of revenue for the last 12 months before the IPO and quarterly revenue growth year-on-year (or annual revenue growth if there is no quarterly data). It turns out that the larger the growth in company revenue - the better.

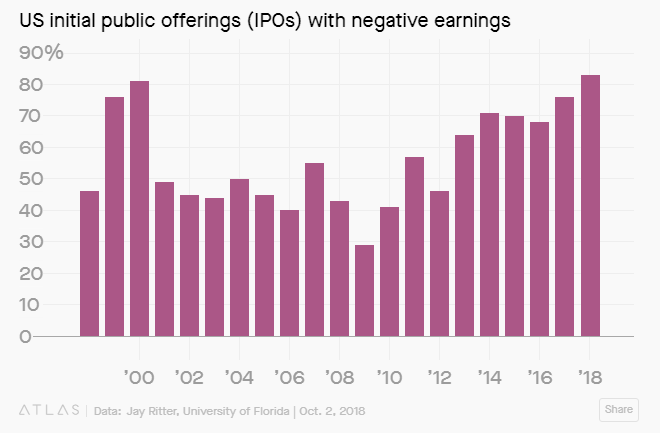

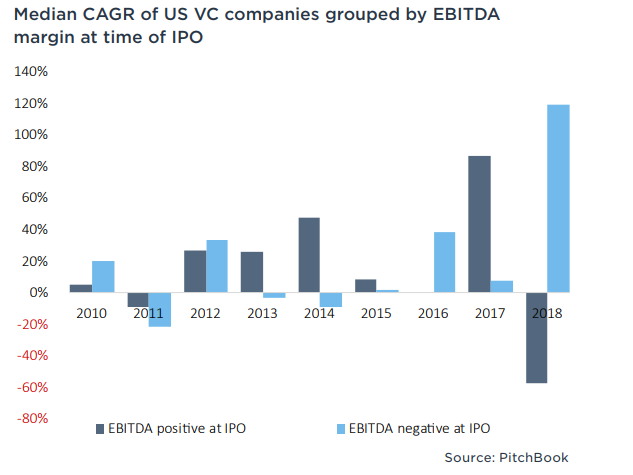

As for profitability, recent statistics from Pitchbook * showed that in 2018, more than 80% of the companies that were listed were unprofitable. Moreover, the average increase in stock prices of unprofitable companies amounted to 120% from the date of the IPO to March 2019. At the same time, the shares of profitable companies fell by an average of 57% from the moment of the IPO in 2018 to March 2019.Paradoxical as it may sound, in 2018 the demand of investors for shares of unprofitable companies far exceeded the demand for profitable companies during an IPO (Fig. 1).

Figure 1

If we talk about a long horizon, then over the past 9 years, the factor of profitability has not affected the profitability of stocks. It turns out that the company's profitability is not statistically significant for determining the future return on investment.

We looked in more detail at the US IPO statistics for 2018.

In total, in 2018, 228 companies were placed on the NYSE and NASDAQ with an average rate of return on the first day of trading of 13.2%. Usually, the success of an IPO is determined by the price dynamics on the first day of trading: if the stock price closed above the placement price on the first day, then the IPO of the company can be considered successful, and vice versa. Therefore, to determine the statistical significance of profitability in the success of an IPO, we tested the following model:

f (ipo_return) = b0 + b1 (profitability)

profitability - an independent variable that reflects the company's EBITDA - profit before interest, taxes and depreciation. In our case, this is a binary variable (Yahoo Finance information source).

ipo_return - dependent variable, reflects the yield on the first day of trading, that is, the difference between the closing price and the placement price (iposcoop information source).

Since EBITDA is not a required financial indicator of US GAAP, some companies do not reflect this data in their reports. So in our final sample there were 132 companies for which EBITDA was available.

Of these 132 companies, 38 were profitable at the time of the IPO, the remaining 94 companies showed negative EBITDA.

The median return on 38 profitable IPOs was 3%, while the median return on unprofitable IPOs was 13.5%. On average, in 2018, the profitability of unprofitable companies by IPO exceeded the profitability of profitable companies.

The results of the regression analysis are shown in the table below:

From these results it can be concluded that there is a small negative correlation between the company's IPO profitability and the first day trading profitability, but this is not a statistically significant effect. It turns out that the company's profitability factor cannot be used to predict IPO returns.

These statistics are explained by the fact that investors value the future growth of the company, that is, the growth of revenue and investment, rather than the current profitability of the business. Investors in IPOs analyze companies in terms of startup potential - consider the size of the future market and evaluate the innovativeness of the product.

1. Many current unprofitable companies can quickly become profitable if they switch their attention from growth to profit.

Spotify , a music streaming service, said the company could become profitable in the short term if it did not spend money on marketing, R&D and other investments in future growth. By the way, Spotify has recently shown profitability for the first time, less than a year after entering the exchange.

Lyftalso could show profitability last year if it had not spent money on attracting new customers and R&D. However, without investing this money in growth, the company will not be able to expand its customer base, which is a key factor at this stage of development. Reducing investment, Lyft may also not fulfill the company's dream of developing and using unmanned vehicles, which will significantly reduce costs in the future.

2. Companies that become public today have more mature products.

More recently, the average age of the company at the time of the IPO was 5 years, while today's average age at the IPO has more than doubled to 11 years. Companies that become public today have more established business models than, for example, during dotcoms. So, last year Lyft's revenue amounted to 2.2 billion dollars (an unthinkable figure for Internet companies of the late 90's).

No. 1. IPO YETI Holdings

The American company YETI, a manufacturer of products for outdoor activities, filed for an IPO on September 27, 2018. The company's revenue growth in the first half of 2018 amounted to 35%, and profit increased from $ 156 thousand to $ 15.6 million. However, a further detailed study revealed that the company's revenue is not growing at a stable pace, subject to seasonal factors and consumer sentiment. We began to doubt about the company's share in the market of products for outdoor activities - YETI has many competitors both in the US and international markets, and after analyzing other factors, we decided not to participate in this IPO. The company's shares were sold at $ 18 at the placement, and 3 months after the IPO, on January 28, the price of the shares after the close of trading was $ 17.8, the yield with commissions would be -5%.

Despite the fact that the company was profitable over the past 3 years, showed revenue growth in the first half of 2018, the company's prospects did not impress investors and the profitability in IPO would give a negative result.

No. 2. IPO Anaplan

To exclude the factor of profitability of the general market, we give an example of a company that entered the stock exchange at about the same time as YETI Holdings.

The American company Anaplan is developing a platform for financial and operational planning and modeling of business processes. The company's quarterly revenue is growing rapidly, 50% year-on-year. The company also demonstrates stable customer growth along with improved indicators of the unit economy. The size of the potential market is $ 21 billion. Given these and other factors, United Traders decided to participate in this IPO.

It is worth noting that this company is unprofitable: the company's profit fell from - $ 16 million to - $ 47 million in the first half of 2018. However, this indicator did not frighten investors - the investment return for 3 months after the IPO was + 63%.

According to a Pitchbook statistical study, as well as our own analysis, we found that the company's profitability factor on IPO does not affect the movement of the share price after the placement. The growth of the company's revenue, product innovation, the size of the potential market, the price of equity at the placement, as well as other factors are more significant for investors in IPO.

It is important to note that the company's IPO was assessed against the backdrop of a growing broad US stock market. Since investing in relatively young companies on an IPO is a risky strategy, possible reductions in the overall market will negatively affect the return on investment of this strategy.

Sources:

pitchbook.com , United Traders

analysis .

IPO is

But first, what it is. IPO (Initial Public Offering) - an initial public offering of shares. This is the process during which the company offers to buy its shares to an unlimited circle of investors, that is, it becomes public. To make money on an IPO, you need to buy shares before they are placed on the exchange, choosing a company whose shares will increase in price and sell them after three months after the placement (Lock-up period lasts for three months when shares cannot be sold by the rules of the exchange).

Investment horizon

Investment strategies differ when the investor plans to make a profit. For example, the buy-and-hold strategy is long-term: we expect that we will make a profit in a few years, therefore, when evaluating, we look at the forecast of the fair value of the company and use the cash flow discount method (DCF approach).

The horizon of investing in IPOs is several months, so we evaluate the company in terms of short-term demand. In this situation, increased investor interest is the determining driver of the stock price at the offering, and the exit multiple approach is the most suitable valuation method.

Benchmarking: revenue is more important than profit

According to our studies, the most significant factors in evaluating a company by a comparative method are 2 indicators - the amount of revenue for the last 12 months before the IPO and quarterly revenue growth year-on-year (or annual revenue growth if there is no quarterly data). It turns out that the larger the growth in company revenue - the better.

As for profitability, recent statistics from Pitchbook * showed that in 2018, more than 80% of the companies that were listed were unprofitable. Moreover, the average increase in stock prices of unprofitable companies amounted to 120% from the date of the IPO to March 2019. At the same time, the shares of profitable companies fell by an average of 57% from the moment of the IPO in 2018 to March 2019.Paradoxical as it may sound, in 2018 the demand of investors for shares of unprofitable companies far exceeded the demand for profitable companies during an IPO (Fig. 1).

Figure 1

If we talk about a long horizon, then over the past 9 years, the factor of profitability has not affected the profitability of stocks. It turns out that the company's profitability is not statistically significant for determining the future return on investment.

Comparative analysis: as we thought

We looked in more detail at the US IPO statistics for 2018.

In total, in 2018, 228 companies were placed on the NYSE and NASDAQ with an average rate of return on the first day of trading of 13.2%. Usually, the success of an IPO is determined by the price dynamics on the first day of trading: if the stock price closed above the placement price on the first day, then the IPO of the company can be considered successful, and vice versa. Therefore, to determine the statistical significance of profitability in the success of an IPO, we tested the following model:

f (ipo_return) = b0 + b1 (profitability)

profitability - an independent variable that reflects the company's EBITDA - profit before interest, taxes and depreciation. In our case, this is a binary variable (Yahoo Finance information source).

ipo_return - dependent variable, reflects the yield on the first day of trading, that is, the difference between the closing price and the placement price (iposcoop information source).

Since EBITDA is not a required financial indicator of US GAAP, some companies do not reflect this data in their reports. So in our final sample there were 132 companies for which EBITDA was available.

Benchmarking: Results

Of these 132 companies, 38 were profitable at the time of the IPO, the remaining 94 companies showed negative EBITDA.

The median return on 38 profitable IPOs was 3%, while the median return on unprofitable IPOs was 13.5%. On average, in 2018, the profitability of unprofitable companies by IPO exceeded the profitability of profitable companies.

The results of the regression analysis are shown in the table below:

From these results it can be concluded that there is a small negative correlation between the company's IPO profitability and the first day trading profitability, but this is not a statistically significant effect. It turns out that the company's profitability factor cannot be used to predict IPO returns.

So why are investors investing in loss-making companies

These statistics are explained by the fact that investors value the future growth of the company, that is, the growth of revenue and investment, rather than the current profitability of the business. Investors in IPOs analyze companies in terms of startup potential - consider the size of the future market and evaluate the innovativeness of the product.

1. Many current unprofitable companies can quickly become profitable if they switch their attention from growth to profit.

Spotify , a music streaming service, said the company could become profitable in the short term if it did not spend money on marketing, R&D and other investments in future growth. By the way, Spotify has recently shown profitability for the first time, less than a year after entering the exchange.

Lyftalso could show profitability last year if it had not spent money on attracting new customers and R&D. However, without investing this money in growth, the company will not be able to expand its customer base, which is a key factor at this stage of development. Reducing investment, Lyft may also not fulfill the company's dream of developing and using unmanned vehicles, which will significantly reduce costs in the future.

2. Companies that become public today have more mature products.

More recently, the average age of the company at the time of the IPO was 5 years, while today's average age at the IPO has more than doubled to 11 years. Companies that become public today have more established business models than, for example, during dotcoms. So, last year Lyft's revenue amounted to 2.2 billion dollars (an unthinkable figure for Internet companies of the late 90's).

Case: Investing in a profitable and loss-making company

No. 1. IPO YETI Holdings

The American company YETI, a manufacturer of products for outdoor activities, filed for an IPO on September 27, 2018. The company's revenue growth in the first half of 2018 amounted to 35%, and profit increased from $ 156 thousand to $ 15.6 million. However, a further detailed study revealed that the company's revenue is not growing at a stable pace, subject to seasonal factors and consumer sentiment. We began to doubt about the company's share in the market of products for outdoor activities - YETI has many competitors both in the US and international markets, and after analyzing other factors, we decided not to participate in this IPO. The company's shares were sold at $ 18 at the placement, and 3 months after the IPO, on January 28, the price of the shares after the close of trading was $ 17.8, the yield with commissions would be -5%.

Despite the fact that the company was profitable over the past 3 years, showed revenue growth in the first half of 2018, the company's prospects did not impress investors and the profitability in IPO would give a negative result.

No. 2. IPO Anaplan

To exclude the factor of profitability of the general market, we give an example of a company that entered the stock exchange at about the same time as YETI Holdings.

The American company Anaplan is developing a platform for financial and operational planning and modeling of business processes. The company's quarterly revenue is growing rapidly, 50% year-on-year. The company also demonstrates stable customer growth along with improved indicators of the unit economy. The size of the potential market is $ 21 billion. Given these and other factors, United Traders decided to participate in this IPO.

It is worth noting that this company is unprofitable: the company's profit fell from - $ 16 million to - $ 47 million in the first half of 2018. However, this indicator did not frighten investors - the investment return for 3 months after the IPO was + 63%.

Conclusion

According to a Pitchbook statistical study, as well as our own analysis, we found that the company's profitability factor on IPO does not affect the movement of the share price after the placement. The growth of the company's revenue, product innovation, the size of the potential market, the price of equity at the placement, as well as other factors are more significant for investors in IPO.

It is important to note that the company's IPO was assessed against the backdrop of a growing broad US stock market. Since investing in relatively young companies on an IPO is a risky strategy, possible reductions in the overall market will negatively affect the return on investment of this strategy.

Sources:

pitchbook.com , United Traders

analysis .