A detailed review of HFT trading: Who does it, trading strategies and impact on the financial system

In our blog, we have repeatedly written about high-frequency or HFT trading. Readers do not always understand some points related to this type of trade, for example, is it clearly a harmful speculative phenomenon, or can it have some positive effect on the financial system? Who does this in general and what trading strategies allow them to earn?

In today's article we will try to give answers to these questions.

Who engages in high frequency trading

A private investor can create a trading robot and connect it to trading using direct access to the exchange technology, however, the main players in the global HFT segment are, of course, various companies.

To make a profit, they use private money, private technology and strategies. Three main types of HFT firms can be distinguished.

The most successful organizations involved in HFT trading are independent proprietary trading companies that conduct operations on the exchange with their own funds, and not with clients' money. Accordingly, all the profit goes to the company, not to the customers.

Sometimes HFT affiliatesmay exist with brokerage and dealer companies. In this case, the broker simply has a separate “prop-trading desk”, the employees of which carry out high-frequency trading. In this case, the company should separate the direction of client trading and prop.trading - such operations should be performed at the organization’s own funds.

Sometimes HFT firms can work as hedge funds . Their main focus is to profit from the inefficiencies in pricing different stocks and financial instruments using arbitrage strategies.

In some countries, there are legislative restrictions aimed at prohibiting speculation for financial institutions (for example, commercial banks) - the US Walker Rule applies, which led to the fact that banks were forced to close their HFT units.

How they make money - some strategies

There are several types of trading strategies that allow HFT companies to make money. Some of them carry constructive grain, and some are perceived by market participants as dangerous tools that upset the current balance of the financial system.

Market making

A passive marketing strategy involves generating a huge number of Limit orders “on both sides of the price” (higher than the market in the case of a sale, and slightly lower in the case of a purchase). This creates market liquidity, which makes it easier for private traders to find an opportunity to complete a transaction. In this case, the HFT trader earns on the difference between the demand and supply spreads.

Popular stocks and financial instruments often themselves have good liquidity, but in the case of less popular securities for an investor, finding a buyer may not be such an easy task.

An investor who bought such a not very liquid share will not be able to just take and sell (buy) it - he will have to wait until the buyer (seller) appears. Or, agree to a deal at a slightly less favorable price offered by the market maker’s HFT algorithm, but right now. Thus, high-frequency traders earn on this difference. In addition, it often happens that market makers receive an additional fee from exchange platforms for the very creation of liquidity.

Arbitration

Another way of earning HFT traders is to search for inconsistencies in the prices of financial instruments at different trading floors.

Statistical arbitrage strategies seek to profit from price inequalities between related markets or instruments. Using various algorithms, HFT traders try to identify correlations between different financial instruments and capitalize on the imbalance between them. An example of related instruments is a stock and futures on it.

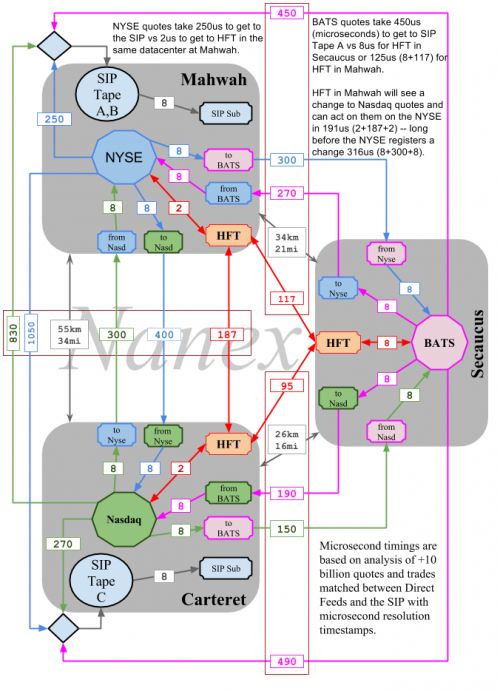

There is another type of arbitration - latency arbitrage, in which an HFT merchant takes advantage of earlier access to information. To do this, servers with trading software are located in exchange data centers ( colocation) next to the equipment on which the cores of exchange systems are located - this allows you to get more important data an instant earlier than other market participants.

There are two colocation options on the Moscow Exchange - placement in the free colocation zone ( broker server in the local exchange network ) and the immediate colocation zone of the exchange:

Consider the situation using an example. Suppose there is a certain investor who wants to complete transactions on related instruments on two different exchanges (A and B). Assume also that exchange B is geographically located farther from the investor, so that its order “reaches” Exchange A in 1 millisecond and executes, and the order reaches the second platform in 2 milliseconds.

In this situation, the HFT-trader, who has located his servers in the exchange’s colocation zone, will receive a notification about the first transaction 0.5 milliseconds after its execution, which will leave him the same amount of time to take some actions until the second transaction realized on the exchange B. And there are a number of possible ways to profit in this case.

For example, an HFT trader can use an algorithm that estimates the likelihood that the first transaction is part of a larger block transaction covering different sites. If the algorithm decides that it is dealing with such a big deal, then it can be assumed that related orders will soon appear on another exchange, say, for the purchase of shares. Further, he can use his advantage in speed and access to data to cancel his orders for sale on the exchange B and re-exhibit with a higher price. If the algorithm can send a signal to this exchange in 0.3 milliseconds, then when 0.2 ms later the order sent by the investor arrives there, it turns out that the price has risen during his journey!

As a result, the investor will encounter the phenomenon of “phantom liquidity” when the orders for buying or selling at a certain price in the queue disappear just before they could pass at that price at that price, and slippage - as a result, the transaction will go at a higher price than the investor expected when sending the order.

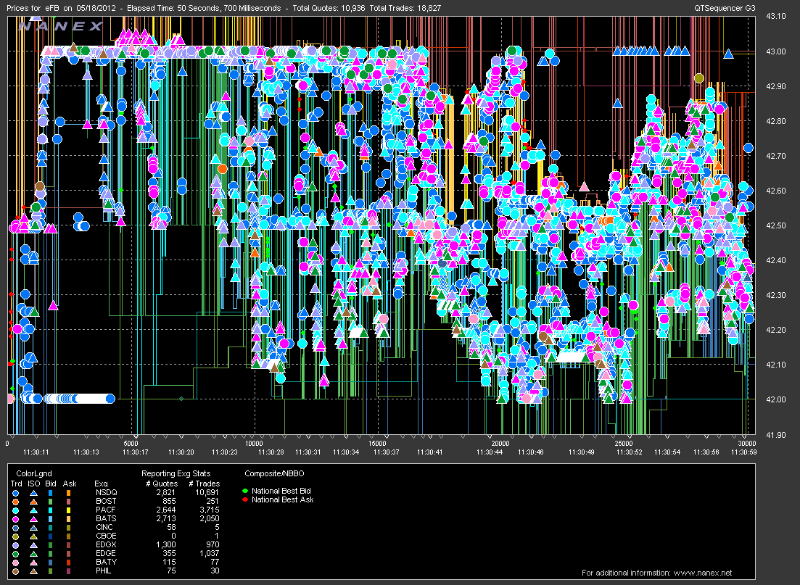

The following is a diagram created by Nanex analysts that shows the benefits that HFT traders can get by using arbitrage delays on various US exchanges:

"The ignition pulse" (momentum ignition)

Sometimes HFT-traders try to provoke market participants to fast trading, causing sharp price movements. Consider an example of applying this strategy. In December 2012, Nanex analysts discovered large-scale market manipulations that occurred on several exchanges at once.

When fast market movement occurs, price spreads expand, which makes the use of momentum strategies profitable. For example, the bid of the stock (for how much the buyer is willing to buy) is $ 100, and ask (how much the seller asks) is $ 100.01, and then everything changes to the bid of $ 99 and ask $ 100. That is, the ask becomes the previous bid - the execution of the last remaining orders in the queue for the purchase of $ 100 will allow the trader to then resell the stock for $ 100.

Financial instruments traded on different platforms may have interconnections, which means that price changes on one exchange will entail changes on others. At the same time, the information does not move instantly - between the exchanges of New York and Chicago over 1200 kilometers or ~ 5 milliseconds. This means that trading robots working in New York will not know about what is happening in Chicago for 5 milliseconds.

When there is a surge in market activity, then “synchronization” between different exchanges occurs for a short time - the price of futures may lag behind the price of shares or vice versa.

In this case, the basic strategy aimed at assuming an impending price fall may look like this:

- Execute transactions on the last in the queue of orders for the purchase of shares, which should follow the future movement.

- Buy put options and sell call options on these shares.

- Prepare to place orders for sale at the old bid price, so as to be the first in the stock market.

- When the last orders to buy shares in New York remain in line, you need to execute transactions at these prices, and at the same time sell futures on the Chicago Stock Exchange.

- When the market goes in the right direction, the time will come to exit the position. Since various trading systems are in a state of overload, this can be used to quickly fluctuate futures prices and fill impulses using HFT algorithms. The picture below illustrates these fluctuations:

Pros and cons of HFT for the market

In a normal situation, the work of HFT-traders creates liquidity, which positively affects the results of investor trading. Trading algorithms analyze the available situation and update prices, so the market quickly and sensitively responds to all changes and irritants.

For ordinary traders, the influence of HFT can also be negative when using manipulative mechanics - a vivid confirmation of this, the so-called "instant collapse" (Flash Crash). Then one of the traders, using the layering technique, that is, placing a large number of sell orders, which he then wanted to cancel, created the illusion of pressurein the market towards lower prices. As a result, the algorithms reacted to the imaginary movement, which allowed the trader to earn money by buying shares at a low price and selling after stabilization.

In general, increasing liquidity and market efficiency also leads to an increase in the number of HFT-traders, which means that the profitability of their operations will decrease. At the same time, expenses (for example, for technology and equipment) continue to grow, which means that soon work in the HFT niche will become unprofitable for many traders. As a result, they will become smaller, again there will be market inefficiencies that can be exploited, which will again lead to the development of HFT. About the trends and prospects of such trade on the Russian stock market, we wrote back in 2013 .