Financial Management: How to estimate the cost of services provided

The IT department in any organization is a consumer of the budget and a source of income at the same time. The information technology budget every year signs for several dozens of items of expenditure, while revenues often turn out to be unstructured, so it is difficult to assess their role in achieving business goals. Understanding the scale, characteristics and costs of classified services provides better infrastructure management and IT control in general. Therefore, in today's article we would like to talk about how the cost of services is calculated and what tools for financial management the ServiceNow platform offers. / Flickr / GotCredit / CC

The goal of financial management for IT services is

maintaining an acceptable level of funding for the design, development and delivery of services that meet the organization’s business strategy. It also allows you to achieve transparency in operations and provide the service provider with new decision-making opportunities.

Financial Management for IT services is part of building a service strategy in ITIL and contains three processes: budgeting, accounting and charging.

Budgeting is the process of planning income and expenses in an organization with the definition of a range of services. Planning is carried out periodically (usually once a year), and gives the company the ability to track where the money is spent. The next process is effective cash accounting. It allows you to detect areas in which you can increase financial efficiency, that is, save. In this case, several components of the cost are taken into account at once:

As for charging, this is the process necessary for the delivery of services, and is responsible for determining how much customers must pay for the service (pricing) and receiving compensation (billing).

Thus, the main tasks of the Financial Management process are: determining the IT services provided by the division, developing a costing methodology, monitoring the work of the IT department and, finally, budgeting, taking into account all factors. Therefore, further we will move on to the issue of financial management of IT and determining the cost of services.

According to the ITIL Service Delivery book, two approaches are used to evaluate the cost of a service : cost accounting by cost centers and cost accounting by activities or services. In the first case, all costs are distributed to customers, and the total total cost is divided equally between them. In the second, all costs are distributed by services: if you calculate all the costs of a service, you can determine the unit of costs and use it as a tool to calculate the consumption of services by each customer.

Since the IT Guild company actively implements and uses the service management model, we will consider the option of calculating the costs of services. To do this, all services must be defined and published in the service catalog and indicated in the client account in accordance with SLA (agreement on the level of service provision) and CMDB (for CI). The figure below shows how the principles of direct, indirect and overhead costs form the whole picture of calculating the cost of a service.

When establishing indirect or overhead costs, an element such as component services should be considered. A component service is a fully valued service that is not explicitly stated in the user accounts or in cost recovery mechanisms. Therefore, such services should be taken into account additionally. An example of a component service can be a network data service if the organization decides to consider its costs as overhead or indirect.

The process of calculating the cost of a service consists of several steps: determining IT services and IT systems, classifying services and modeling services and systems in CMDB, selecting services and systems indicated in user accounts, determining a methodology for cost allocation for component IT services and, finally, determining the unit of cost for services visible to the subscriber based on the method of their use.

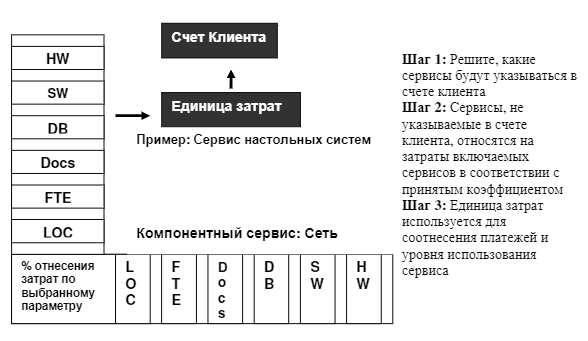

An example of calculating an IT service is shown in the diagram below. Here HW - equipment, SW - software, DB - databases, Docs - documents, contracts, licenses, FTE - allocated human resources, and LOC - buildings.

Calculation of costs for a service ( source )

Calculation of costs for a service ( source )

The above diagram shows two fully regarded IT services, one of which (desktop systems) is included in the client’s account, and the other is considered as a component service (network). A percentage of the cost of the latter is included in the total cost of desktop service.

Consider an exampleprocess of forming the cost of a service, but with some assumptions. Of course, it includes the cost of licenses for the application, 100% providing this service. The following is the license for the database that our application uses. Suppose that we need 1 out of 5 licenses for the database, so we will take into account only 20% of the total cost. Next, consider the server itself, on which the application is running, but there is another similar application on it, so only 50% of its cost will be included in the cost of the service.

We also take into account the cost of server support by an external organization. If it supports 4 servers (and costs are distributed evenly), then we need only a quarter of the cost of support. But only 10% of them will participate in the formation of the cost of one service and 50% of the cost of another service. Total we get: 15% = 2.5% (10% of 1/4) + 12.5% (50% of 1/4).

It is also necessary to take into account the cost of the ServiceDesk service, we will consider it in a uniform breakdown by service (the total number of which, say, 20), that is, 5%. We add here related operational services, for example, network support - this is also 5%, if we assume that the costs are evenly divided by services.

We also give a general formula for calculating the cost of ownership of a service for the required period. It looks like this:

COService = 100% Sla + 50% Ss2 + 20% Sdb + 10% Ss1 + 15% Ssup + 5% Ssd + 5% Snet

In the above formula: Ss1 - cost of equipment (Server 1), Ss2 - cost equipment (Server 2), Sla - cost of application licenses, Sdb - cost of database licenses, Ssup - cost of server support, Ssd - cost of SD support, Snet - cost of system service network support.

Financial Management (Financial Management) is made by the type of incident management, so that IT professionals and managers are more convenient to carry out operations in the familiar interface. Several processes are used to calculate the cost of Financial Management services in ServiceNow. Here are the main ones, for each of which the platform provides ready-made tools:

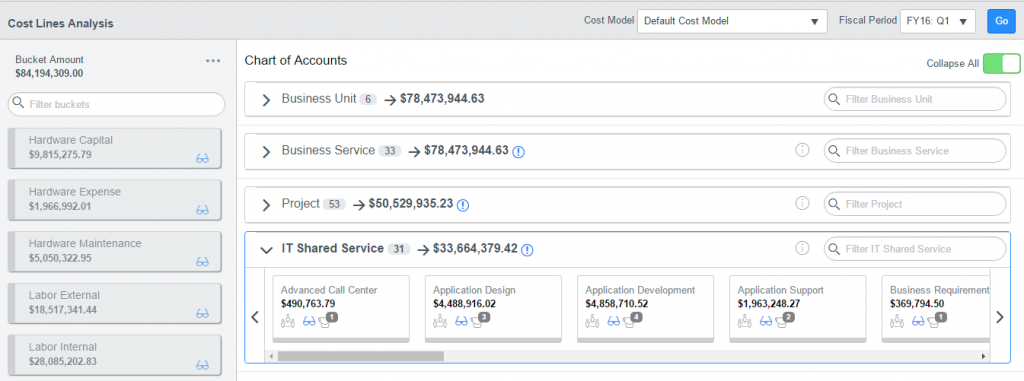

ServiceNow allows you to set budgets and set amounts for a specific period. Cost centers can be budgeted to show the actual total cost of all associated costs. In the ServiceNow console, you can analyze your budgets and costs.

For each item of expenditure, you can get extended information, as well as detailing the costs.

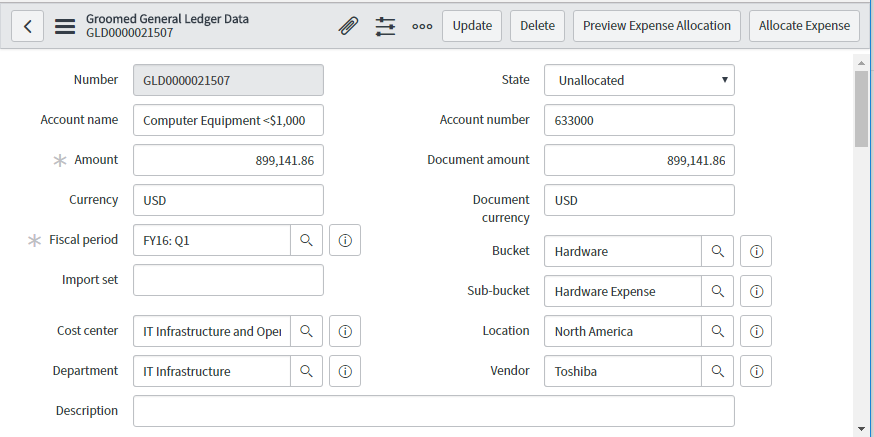

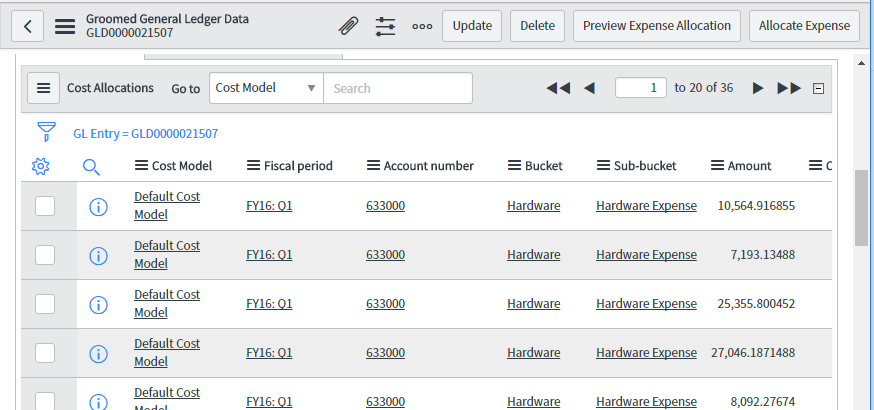

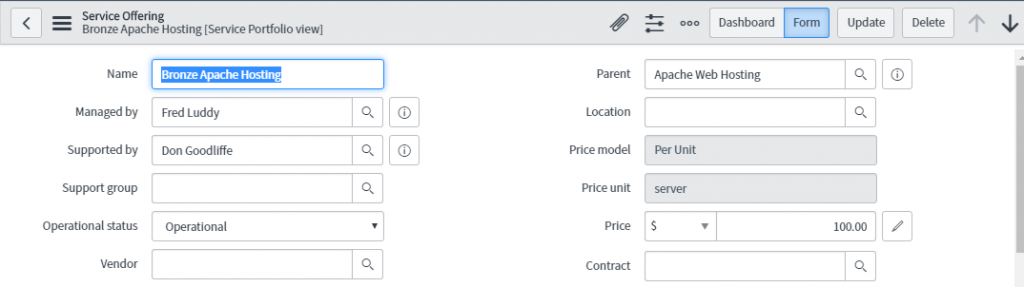

Cost lines are used to indicate costs for various activities. They can be created manually, imported into the system or generated automatically when a user requests a service. The set of cost lines can be used in billing the customer for the services that he uses.

Here you can set the price for using the services provided. When you create a configuration unit, cost lines are created automatically.

The combination of knowledge on calculating the costs of services and ServiceNow tools allow the IT department to effectively plan and use the budget, as well as receive high profits from the services provided. These are just the core processes that Financial Management ServiceNow provides. You can find out more about its functions, installation, configuration and use in the ServiceNow documentation library or contact the IT Guild specialists, the official certified partner of ServiceNow.

PS A few more materials on the topic from the blog "IT Guild":

maintaining an acceptable level of funding for the design, development and delivery of services that meet the organization’s business strategy. It also allows you to achieve transparency in operations and provide the service provider with new decision-making opportunities.

Financial Management for IT services is part of building a service strategy in ITIL and contains three processes: budgeting, accounting and charging.

Budgeting is the process of planning income and expenses in an organization with the definition of a range of services. Planning is carried out periodically (usually once a year), and gives the company the ability to track where the money is spent. The next process is effective cash accounting. It allows you to detect areas in which you can increase financial efficiency, that is, save. In this case, several components of the cost are taken into account at once:

- Capital costs - the purchase of what will become a financial asset, such as a server.

- Transaction costs - the costs of ensuring the operation of services - electricity, employee salaries, etc.

- Direct costs are the costs of providing IT services that can be attributed to a specific customer, project, etc. For example, the cost of operating dedicated servers or purchasing software licenses.

- Indirect costs - the costs of providing IT services that cannot be fully attributed to a specific customer, for example, buying a shared server.

- Fixed costs - costs whose value does not change with an increase (decrease) in the intensity of use of the service.

- Variable costs are costs, the value of which varies depending on the intensity of use of the service.

As for charging, this is the process necessary for the delivery of services, and is responsible for determining how much customers must pay for the service (pricing) and receiving compensation (billing).

Thus, the main tasks of the Financial Management process are: determining the IT services provided by the division, developing a costing methodology, monitoring the work of the IT department and, finally, budgeting, taking into account all factors. Therefore, further we will move on to the issue of financial management of IT and determining the cost of services.

Service cost calculation

According to the ITIL Service Delivery book, two approaches are used to evaluate the cost of a service : cost accounting by cost centers and cost accounting by activities or services. In the first case, all costs are distributed to customers, and the total total cost is divided equally between them. In the second, all costs are distributed by services: if you calculate all the costs of a service, you can determine the unit of costs and use it as a tool to calculate the consumption of services by each customer.

Since the IT Guild company actively implements and uses the service management model, we will consider the option of calculating the costs of services. To do this, all services must be defined and published in the service catalog and indicated in the client account in accordance with SLA (agreement on the level of service provision) and CMDB (for CI). The figure below shows how the principles of direct, indirect and overhead costs form the whole picture of calculating the cost of a service.

When establishing indirect or overhead costs, an element such as component services should be considered. A component service is a fully valued service that is not explicitly stated in the user accounts or in cost recovery mechanisms. Therefore, such services should be taken into account additionally. An example of a component service can be a network data service if the organization decides to consider its costs as overhead or indirect.

The process of calculating the cost of a service consists of several steps: determining IT services and IT systems, classifying services and modeling services and systems in CMDB, selecting services and systems indicated in user accounts, determining a methodology for cost allocation for component IT services and, finally, determining the unit of cost for services visible to the subscriber based on the method of their use.

An example of calculating an IT service is shown in the diagram below. Here HW - equipment, SW - software, DB - databases, Docs - documents, contracts, licenses, FTE - allocated human resources, and LOC - buildings.

The above diagram shows two fully regarded IT services, one of which (desktop systems) is included in the client’s account, and the other is considered as a component service (network). A percentage of the cost of the latter is included in the total cost of desktop service.

Consider an exampleprocess of forming the cost of a service, but with some assumptions. Of course, it includes the cost of licenses for the application, 100% providing this service. The following is the license for the database that our application uses. Suppose that we need 1 out of 5 licenses for the database, so we will take into account only 20% of the total cost. Next, consider the server itself, on which the application is running, but there is another similar application on it, so only 50% of its cost will be included in the cost of the service.

We also take into account the cost of server support by an external organization. If it supports 4 servers (and costs are distributed evenly), then we need only a quarter of the cost of support. But only 10% of them will participate in the formation of the cost of one service and 50% of the cost of another service. Total we get: 15% = 2.5% (10% of 1/4) + 12.5% (50% of 1/4).

It is also necessary to take into account the cost of the ServiceDesk service, we will consider it in a uniform breakdown by service (the total number of which, say, 20), that is, 5%. We add here related operational services, for example, network support - this is also 5%, if we assume that the costs are evenly divided by services.

We also give a general formula for calculating the cost of ownership of a service for the required period. It looks like this:

COService = 100% Sla + 50% Ss2 + 20% Sdb + 10% Ss1 + 15% Ssup + 5% Ssd + 5% Snet

In the above formula: Ss1 - cost of equipment (Server 1), Ss2 - cost equipment (Server 2), Sla - cost of application licenses, Sdb - cost of database licenses, Ssup - cost of server support, Ssd - cost of SD support, Snet - cost of system service network support.

Tools for calculating the cost of services in ServiceNow

Financial Management (Financial Management) is made by the type of incident management, so that IT professionals and managers are more convenient to carry out operations in the familiar interface. Several processes are used to calculate the cost of Financial Management services in ServiceNow. Here are the main ones, for each of which the platform provides ready-made tools:

- Budgeting is the process of forecasting and controlling the income / expenses of funds within the organization.

- Cost accounting is a process that allows an IT department of a company to record expenditures.

- Charges - The process of billing customers for the services they used.

- Pricing is the process of determining the price for a service that a company provides to its customers.

Budgeting at ServiceNow

ServiceNow allows you to set budgets and set amounts for a specific period. Cost centers can be budgeted to show the actual total cost of all associated costs. In the ServiceNow console, you can analyze your budgets and costs.

For each item of expenditure, you can get extended information, as well as detailing the costs.

Accounting and accruals

Cost lines are used to indicate costs for various activities. They can be created manually, imported into the system or generated automatically when a user requests a service. The set of cost lines can be used in billing the customer for the services that he uses.

Pricing

Here you can set the price for using the services provided. When you create a configuration unit, cost lines are created automatically.

The combination of knowledge on calculating the costs of services and ServiceNow tools allow the IT department to effectively plan and use the budget, as well as receive high profits from the services provided. These are just the core processes that Financial Management ServiceNow provides. You can find out more about its functions, installation, configuration and use in the ServiceNow documentation library or contact the IT Guild specialists, the official certified partner of ServiceNow.

PS A few more materials on the topic from the blog "IT Guild":