Money20 / 20 Europe 2016: Conference Review

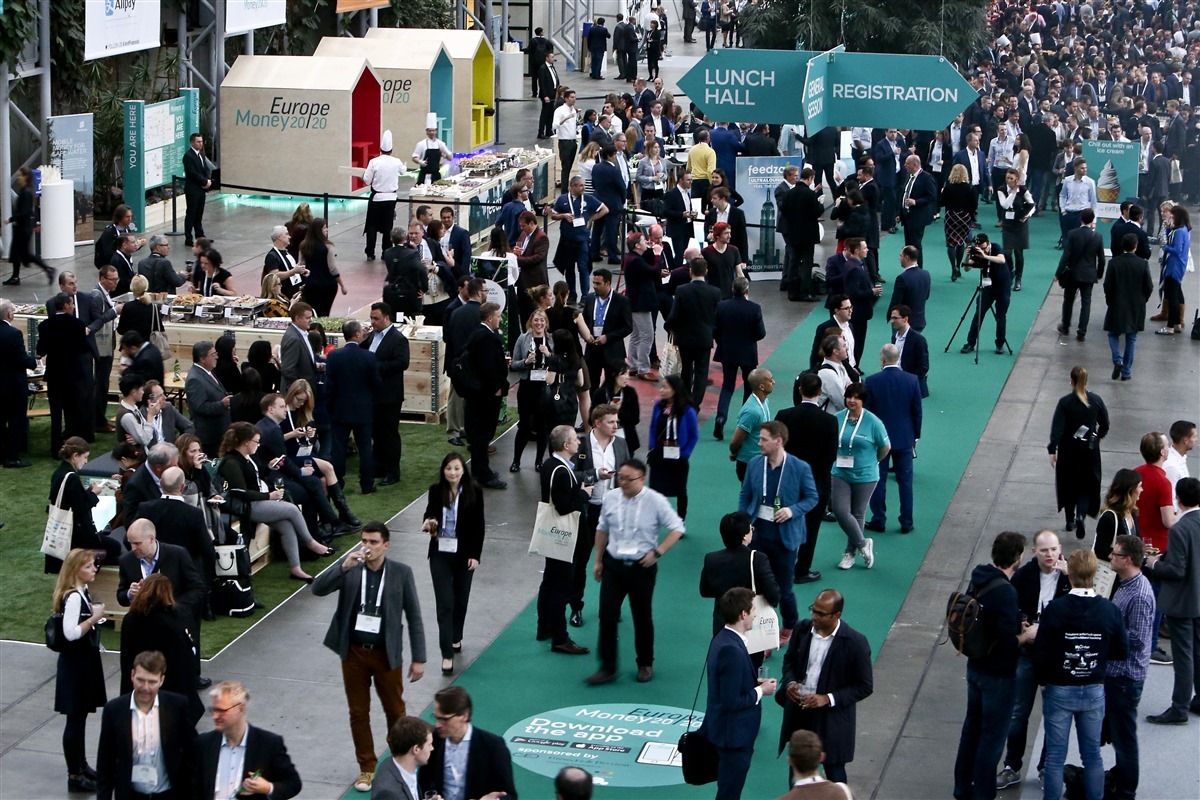

This month, the financial and technological conference Money20 / 20 Europe 2016, the European version of the famous Money20 / 20 forum, which is usually held in the autumn in Las Vegas, was held in the capital of Denmark, Copenhagen. The event gathered more than 3,700 guests and 422 speakers from 75 countries. The conference was attended by over 200 sponsors. The coverage of the main events of the four-day “marathon” was carried out by more than 100 Media20 / 20 Europe media partners.

This month, the financial and technological conference Money20 / 20 Europe 2016, the European version of the famous Money20 / 20 forum, which is usually held in the autumn in Las Vegas, was held in the capital of Denmark, Copenhagen. The event gathered more than 3,700 guests and 422 speakers from 75 countries. The conference was attended by over 200 sponsors. The coverage of the main events of the four-day “marathon” was carried out by more than 100 Media20 / 20 Europe media partners. An event of this magnitude cannot be ignored. We at PayOnline , an international payment acceptance system, have prepared for you an overview of the most interesting and significant from our point of view theses of Money20 / 20 Europe 2016.

The eventful program of the forum united conference and exhibition areas. On the very first day, experts from BBVA, Visa and MasterCard spoke at Money20 / 20 Europe, presenting the latest news from their companies. Google, Samsung, Amazon and Alipay were represented by a whole delegation of directors.

The message “We are open for cooperation” was common to all financial institutions participating in the Money 20/20 conference. All of them with great desire are ready to listen and discuss possible conditions. Yes, each of them works within the framework of its own streamlined processes, but there are also innovative units in such companies that allow them to quickly adapt. Some major players, such as ING, establish separate corporate entities with technology testing as their main business. In general, all major players understand that the consumer does not intend to wait until everything is done as usual. Therefore, large companies are ready to act now.

One of the high-profile statements made at Money20 / 20 Europe was the news that this summer the Chinese mobile payment service Alipay will be launched in Europe. Alipay will start moving west from the UK, France and Germany. In May, the company will release an updated application in which the Local Services Platform feature will be added, giving recommendations on shopping based on geolocation.

Amazon has offered online stores, whose products are presented on the retailer’s portal, their Amazon Payments payment service. The main goal of this step is the company's desire to help sales partners expand their ability to receive payments. According to Patrick Gauthier, vice president of Amazon Payments, this will also increase customer confidence. The affiliate program will be implemented through developers of e-commerce software, including Shopify, Presta Shop and Future Shop. These companies will provide ready-made links for payment services, training and marketing support. At the moment, the program is open, but so far available only in 4 countries: USA, Germany, Great Britain and Japan.

Diebold spoke about his new mobile banking concept and introducedCryptera Security Application. In addition, the company introduced a new ATM concept for mobile devices , which issues and accepts cash without a screen, card reader or keyboard. Instead, the ATM uses the client’s mobile device as the main interface. According to a company representative, the concept was developed taking into account the modern pace of life, new machines will allow customers to get faster and more convenient access to cash.

Verifone, one of the world leaders in the field of payment and commercial solutions, introduced Verifone Carbon, a beautiful, flexible payment terminal that uses all the power of modern hardware and embedded software. Verifone carbon- A business solution suitable for owners of cafes, fast-food restaurants and retail stores. A characteristic feature of the device is the presence of two high-resolution screens, optimized for the seller and the buyer.

Panasonic introduced a contactless payment terminal for aircraft, allowing passengers to pay for food and services with a contactless card. At the moment, the terminal only works with MasterCard cards. Soon Panasonic plans to complete negotiations with other payment companies, including American Express, Union Pay and Visa.

Another interesting payment solution was introduced by Droplet. Zero Touch payment service allows UK residents to make purchases using cameras. The system “identifies” the buyer and transmits all available information about him on the seller’s screen. The buyer, in turn, can pay for purchases without the need to use a card, smartphone or other payment instrument, money is automatically debited from the account after passing the identification procedure and confirming the payment.

Giants of the financial world, such as HSBC, have publicly discussed a full-fledged two-year strategy to create a bank without borders, providing services to customers from all over the world. AtomBank launch was announced at the conference , Mondo , TandemBank attendedconfirming the reality of this approach.

MasterCard has expressed interest in working with social media giants Facebook and Twitter to create their own payment services.

“We see the place that companies like Facebook and Twitter have in the social media market, so our representatives are sitting in Silicon Valley and negotiating with them,” said Ann Cairns, president of international markets for MasterCard, during an interview with CNBC.

The representative of MasterCard said that the result of the joint work could be “the emergence of something like a direct payment service between network users”. Of course, the Facebook Messenger app in some countries already allows you to make money transfers to friends. But MasterCard wants to go even further and add the ability to make payments to existing functionality. As for Twitter, this social network already offers retailers commercial services, in particular, placing the buy button on their tweets. Cairns also added that collaboration with Facebook and Twitter is likely to follow the same pattern that the company works with its other partners.

Western Union announced the launch of a new B2B platform, which allows you to create relationships between companies and provides them with the ability to make settlements. The implementation of international transfers is not an easy task for business, since the signing and implementation of the terms of individual agreements with suppliers through traditional channels requires considerable effort and attention. Floating exchange rates can also cause a lot of trouble and lead to losses. Western Union’s B2B division, Western Union Business Solutions, was created to address these issues. The platform is based on Edge, which allows businesses to establish relationships with each other and work on billing and payments.

The only Russian companies that placed their booth at the Money20 / 20 Europe expocenter were QIWI and CONTACT. At a joint stand of the companies, projects of money transfers and payment services were presented , as well as solutions for e-commerce - a direct payment and logistics gateway to Russia for merchants and consumers from around the world.

BBVA CEO Carlos Torres Vila shared the information that the bank is currently devoting the lion's share of its attention and investments to design, wanting to better adapt to new user experiences. By the word "design" an expert means not only the appearance, but also the entire process of interaction between people. Torres Vila noted:

“Many startups choose one tiny part of what banks do. However, there are so many of them that together they cover all the activities that we do. Each such tiny part has its own dozen companies that perform their work efficiently. Moreover, their capabilities are much narrower than ours, but the value for the client is greater. ”

Other topics of the European Money 20/20 were blockchain, increasing the availability of digital technologies and methods of digital and biometric identification.

Microsoft has announced a strategic partnership with R3 . The consortium members will work together to develop blockchain-based solutions suitable for use in everyday life. First of all, partners intend to modernize banking processes and simplify operations by introducing distributed registry technology, which ultimately will save billions of dollars.

Continuing the topic of blockchain, the representative of the Isle of Man government, Brian Donegan, expressed the view that it was time for the financial industry to write a law similar to the law on the Internet, signed by Bill Clinton in 1996, which actually launched the development of a global network. Monica Monaco, the founder and managing director of Trust EU Affairs, in turn, announced a trial version of the legal framework for AML and KYC for cryptocurrency in the EU, it will be presented in September 2016.

Many keynote speakers spoke about the relevance and relevance of biometric technologies to their business and how these technologies have become part of their identity management products and procedures. Anne Cairns, a spokeswoman for MasterCard, spoke about the growth in overall demand for MasterCard services that occurred after the company launched biometric selfies as an authentication strategy. Andy Maguire, chief operating officer of HSBC, also mentioned the role that biometric technologies can play in the area of compliance control and cost reduction.

The topic was continued by public discussion. The key expert who skillfully guided the conversation in the right direction was Peter O'Neill, CEO of FindBiometrics. Emilio Martinez from Agnitio, Clive Burke from Daon, Craig Ramsey from HSBC and Olov Renberg from BehavioSec also participated in the conversation. Experts unanimously concluded that the implementation and use of biometrics in large enterprises and banks require a platform approach. Not all forms of biometric interaction are equally good for each task and, as a result, they are not able to single-handedly meet the requirements of a “single-channel interaction”, which is key for both consumers and large companies. Peter O'Neill expressed a common opinion among all participants that thanks to the successes of Apple, Samsung and Android in introducing biometric technologies,

Of course, there was a discussion of the problem of protecting personal information. Are the laws governing these issues the same in different countries of the world? Of course not. Based on their international experience, HSBC speakers said that things that are considered acceptable and easily perceived by consumers in the United Kingdom are far from always acceptable in other countries. This once again confirms the need for an individual approach to the consumer in terms of the use of certain biometric technologies in each individual country, since this subject is closely related to certification in the field of security, data storage and encryption standards. Is there a need for regulation? Yes. Work ahead big and FIDOAllianceshould act as the main player, however, practical application is already taking place, so regulation is far from always keeping pace with real processes.

The review was prepared using materials from LTP and Linkedin . Subscribe to our blog, there are many more interesting posts ahead. And if you need to organize the acceptance of payments on the website or in the mobile application, please contact our specialists with pleasure we will answer all your questions and help with integration.