Back to the future or the main stages of development of accounting in history

In a previous article, I illustrated a ripe moment for the change of the digraphic paradigm in accounting, which is today fundamental in all computer accounting systems. The topic is very deep. I'll try to parse it in more detail.

The third law of dialectics asserts that “in the forward movement there is a return back, the new features of the old are repeated”

Sometimes, to understand the upcoming revolutionary changes, it is enough to carefully look into the past.

Trends in the emergence of breakthroughs can be seen in the critical accumulation of quantitative changes in the framework of one of the existing paradigms. (The second law of dialectics)

If we mentioned two of the three laws of dialectics, then we will not disregard the remaining. The first law of dialectics states that development proceeds through the solution of mutually exclusive contradictions.

Now you can apply all three laws in considering the subject of business accounting yesterday, today and possible future formats.

For reasoning, I’ll take three parallel and interconnected processes:

- Business

- Information Technology

- Accounting

And consider them through the gloom of centuries.

Business

People always produced and sold something, rendered services to each other. The beginning of the use of electricity, an internal combustion engine, and other great discoveries led to a rapid change in the structure of the business and its requirements.

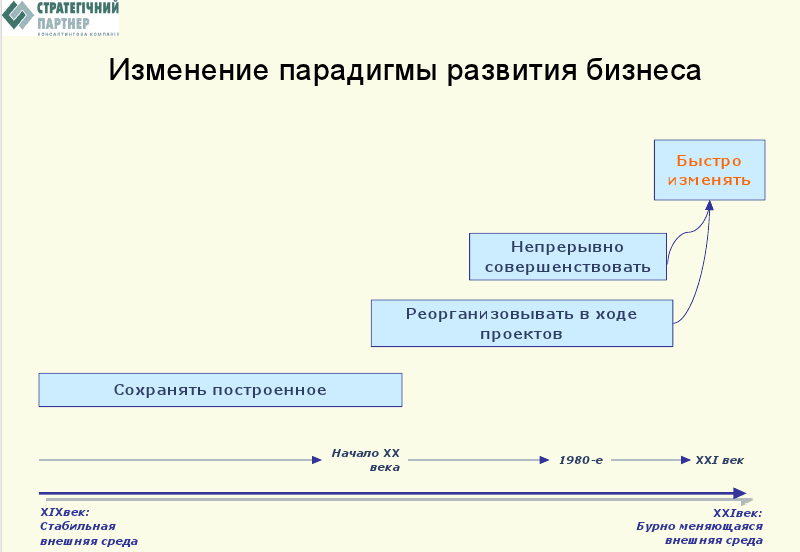

In one webinar V.P. Savchuk (partner of our project, my teacher in fin. Management, author of wonderful books ) presented the change in business requirements on the timeline.

After that, by analogy with the pyramid of the hierarchy of human needs of Mr. Maslov , I transformed this visualization into a pyramid of the hierarchy of business needs.

So it seemed to me more adequate to the current moment, because the business cannot only change, it is necessary to provide all the requirements consistently from the bottom up.

Thus, we all, without unnecessary chewing, understand that in recent years, the growth of business requirements has a tendency towards geometric progression. In a way, we can regard this as the limit of quantitative content, but this is not about that in this article.

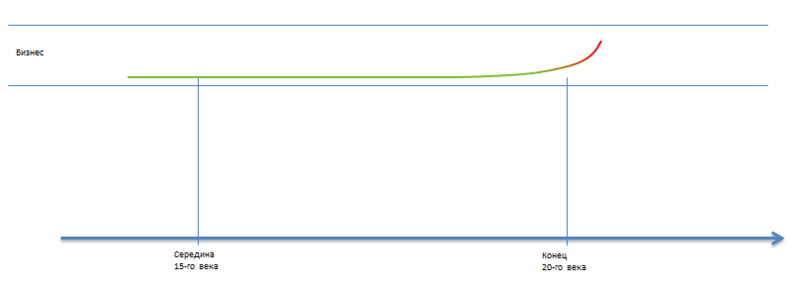

We will depict this phenomenon on the chart and move on.

Information Technology

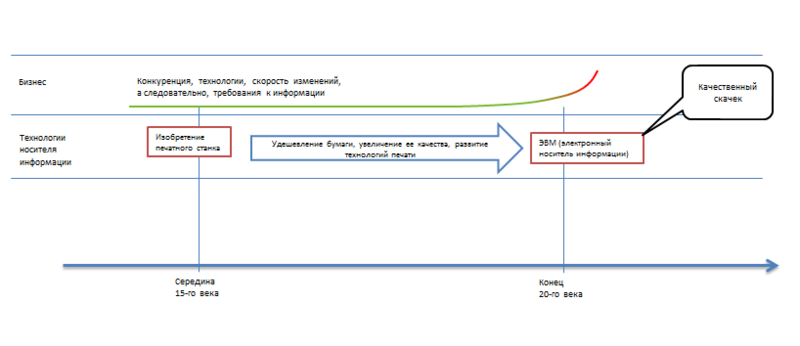

Consider information technology in terms of information carrier.

Once upon a time, people applied information to stones, wooden planks. Then there were options with papyrus.

But the real breakthrough (revolution) of media technology was the emergence of paper and printing press. This happened in the middle of the 15th century. Those. some great quality leap. The size of the information storage and the complexity of operating it are reduced by tens and hundreds of times.

Further, over the course of five centuries, information technology has been developing in the framework of the paper paradigm. Improving methods for making paper, which is correspondingly cheaper. Methods for applying information on paper, as well as methods for structuring information in the framework of new exceptional (compared with stone tiles) capabilities, are also being improved.

But what happens at the end of the 20th century? A new kind of storage medium is emerging. Call it a computer or computer, for simplicity. You don’t even have to say that now the city library can fit in 1 square millimeter. And the possibility of entering information, storage, retrieval, processing, etc.? It is difficult to determine the number of zeros of the order of increasing quality.

To a large extent, the leap in the quality of information technology has determined the leap in business requirements. We are talking about interconnected things.

On the graph, I highlight two global leaps in the quality of information technology:

Accounting

Of course, in this case we consider accounting as an attempt to reflect the occurring events in the business in the form of numbers and other records. I like to define: Accounting is a digital reflection of life. In our digital world, such a definition makes it possible to draw adequate analogies. For example, we draw an analogy of photography and accounting. Accounting should reflect the state at various points in time. A photograph is able to capture (record) a visible state at a point in time. Sometimes accounting balance is called a state photograph. In modern accounting, a bunch of conventions that only specially trained specialists know, but everything seems normal to a normal person, is very complicated and confusing. Conditional reflection is not a photograph, but a drawing. Here is an analogy. Before, when there was no color photo (technical limitation of photography), artists painted black and white photographs with paints (I think many will find such instances left from their grandmothers). Our bookkeeping is not an exact digital reflection of reality, but a black-and-white photograph, painted by a specialist in conditional images.

Finished with the lyrics and see how accounting technologies have evolved in history.

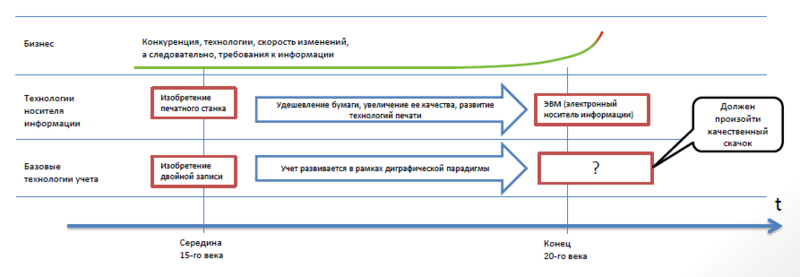

It is funny that the first documented evidence of the use of double-entry falls into one decade with the invention of the printing press.

In general, it is accepted in science that there are three main accounting paradigms:

- Unigraphic (without using double entries)

- Digraphic (using double entries)

- Cameral (sawing ... budget , and also for pure DDS, we will not take it into account) .

Who cares, here is a link to a good article on paradigms .

Double recording is the basic principle of data recording. It is very simple (mathematics is the fifth grade) and is the basis for various structural systems, the input of which is the primary documents, and the output reports on the status and results (balance sheet and income statement expenses). Such structural systems in science are called forms of bookkeeping. Those. the form of bookkeeping (a set of definitely interconnected labels) is a certain technical device, limited by the level of technology used (this is important, since paper and how to apply information to it is the level of information technology), inside which one or another method of recording, processing and extracting data is used (I specially translate everything into the language of modern IT).

One can imagine that before the invention of double-entry, accounting developed, one way or another, within the framework of the unigraphic paradigm, after, respectively, within the framework of the digraphic paradigm.

Namely, in parallel with the improvement of papermaking technologies and the technologies for applying information to it, various systems (forms of bookkeeping) arose that optimized accounting, but within the framework of all one digraphic paradigm.

It's time to draw the whole schedule.

Now you can see the full relationship and what I’m all going to.

First, the relationship between the needs of the business and its corresponding accounting requirements, which are developing within the limits imposed by the level of information technology, is visible.

Secondly, it is clear that a qualitative leap in information technology generates a qualitative leap in basic accounting technology.

And finally, it is clear that a new accounting paradigm should arise, corresponding to the new qualitative capabilities of information technology. At the same time, it becomes clear that what is called managerial accounting in the modern world works exclusively within the framework of a unigraphic paradigm and cannot realize such a breakthrough.

This entire article is strongly theorized, but in another way it will not be possible to tear off attention from practical problems that are solved daily by accounting and automation specialists. For the most part, these problems are only a consequence or a chain of consequences of a key problem, which, in turn, lies at such a theoretical level. And if you solve a key problem, then all the problems that are the consequence will be solved. So says common sense and theory of restrictions (CBT) Ilyahu Goldratt. Goldratt also claims that if practical rules were formed during the period of the limitation, then even if the technological limitation itself is lifted, then these rules themselves will become a limitation.

Everything that he says about the rules is very relevant to accounting, because the five-century history of development in the mode of restriction of paper information technologies formed a huge number of rules and stereotypes. And, as you know, stepping on the throat of stereotypes is extremely difficult.

In conclusion, I confess that we have made this breakthrough. We had to spend several years to destroy stereotypes in our own heads (it is good that there were not many of them). But now we are faced with the problem of external misunderstanding, i.e. with an even more difficult task - to destroy stereotypes in the minds of others.

I hope this article, even if it is too theoretical, is at least to make us think more carefully and impartially (on top of stereotypes and rules) to look at the technologies and methodologies we developed.

I wish you success and prosperity, and the ability to control your own business or yourself as a business will definitely lead to this.

ps The second and third laws of dialectics are viewed in the text. What place is the first law of dialectics here, it will be possible to understand from a future article about why there is a division of financial and managerial accounting.