"Throw money into the furnace of business" or problems associated with the control of the business by its owners

In a previous article on Habr, I tried to directly present the required format of digitized information necessary for controlling a business.

They didn’t understand ...

On the eve of my first seminar on the topic “How to control a business without going into details”, I decided to describe in more detail the prerequisites for the conclusions made in the last article. And in unsuccessful story format, using examples from personal experience.

The size of the business does not matter, as does the industry, technological effectiveness, etc. If you are the founder and / or owner of the business, you are obliged to control it, and this could be a verdict. And if you do not control, you will lose it.

Personal experience.

In 97, I organized my first startup in the form of a small car service to install additional equipment. I clearly remember now that I wanted to be rich and free. In any case, the development and growth consisted in the fact that after the organization of one enterprise, it was possible to start organizing another, receiving passive income from the previous one . I took risks and worked from morning to night so that I would not work later .

But I became the owner, and this became my sentence. The next five years since the organization of this car service, I worked 12 hours 7 days a week. I didn’t even dream about vacation. I have never been on a hunt (my favorite pastime) for 5 years. Everything was justified by an attempt to present the situation as "work is life, life is work, and I enjoy life."

Such incredible efforts led to good growth. I became rich and free to choose what to do at any moment. Since I delved into all the details every day and managed everything myself, everything was fine.

It was good until the business grew, and I was no longer enough for everything. I lost control because the principle approach was personal participation and direct management. This again became a sentence. For a while I grabbed for the weak spots. There was a feeling that one was picking up, the other was falling. I went to study at MBA (this was the biggest mistake). As a result, I lost several hundred thousand dollars and most of the business over the year.

Then again hard labor to restore their condition.

Another example.

Once three friends decided to open a taxi. They had their own profitable business. They saw taxis as a simple tool for making money. Those. they considered these investments solely in the interests of passive income, justifying the initial investment and risks.

They threw off 6 million rubles and bought 20 new Volga.

Then they laid these Volga in the bank, received a loan of 5 million and bought another 15 cars. They pledged them too ...

Altogether, 100 cars worth 30 million were obtained, of which 24 were loans.

I do not take into account the costs of service and park, etc. For simplicity.

Hired management and launched a business.

During the year, management paid monthly to them 600 thousand rubles of unofficial dividends.

Thus, they believed that the payback of the project is 120% per annum, and even boasted to everyone and cited this case as an example of an excellent investment.

After a year, they stopped paying, and friends had to figure out what was the matter.

It turned out that 100 cars were in poor condition, and could only be estimated at 30% of the initial cost.

those. they had 10 million cars left. The

loan to the bank was repaid by a third (the loan was three years old).

The total loan left 16 million.

Considering that they received 7.2 million in money over the year. They not just did not pay off, but lost 4.8 million rubles.

Those. six were invested initially, and then almost five more were sown. In other words, the actual return on investment is minus 80%.

Intermediate conclusions.

These and many other stories in practice made me seriously think about the causes of such problems. Why couldn’t I normally control the business? Why was I so busy? Why can not you leave a business without close daily attention to detail? The desire to find an answer to these questions predetermined the direction of my activity for many years to come.

In any case, the goal was set: to find ways, or even create a system so that you could control the business without going into details and direct management (initially only for yourself).

Where is that coveted directorial button, clicking on which you can immediately see what is happening in your business at any given time ?!

But the question was not in the button itself, but in what should be seen and how to look at it.

Analogy

Imagine the situation that we decided to control what is happening outside the window. Nobody taught us this process, we will do it naturally.

Give it a try!

At first you will look at the big picture without concentrating on the details. If something moves (changes, attracts attention), then you concentrate on it, peering into the details and analyzing them. Having understood, you again look at the big picture.

This is a natural principle of control. He does not need to learn, he is laid down on an intuitive level. From the big picture to the details. We constantly monitor the overall picture and, if necessary, concentrate on the details.

Let's get back to business control. How do we do this?

In fact, we constantly concentrate on the details and do not see the big picture.

Every day we plunge into a huge amount of detailed information, and if the business is not big, then we have a chance to control, therefore, the overall picture. And if the business has grown, then we lose our understanding of what is happening.

And what is the overall picture for business?

What do we control the window in our analogy? If nothing changes, then something is unlikely to attract our attention. Thus, we can conclude that we control the condition and the ongoing changes.

The state of the business. How is it expressed in numbers?

Since a business is created with the goal of making a profit (making money), its condition must also be expressed financially (financial condition), i.e. in monetary terms. It evaluates what the business has on the one hand, and on the other, the sources of funds that were raised in order to acquire all that the business has are evaluated. The first in accounting (initially, it is a science designed to digitize a business) is called Assets, the second is Liabilities (Liabilities (liabilities, borrowed funds)). Naturally, the sum of what a business has is equal to the sum of the sources used to form this economy. In this way, the digital state expressed financially (in monetary terms) in accounting represents the state of the enterprise (business). This representation is called balance.

But this is bad luck. Traditionally, the balance sheet (report on the financial condition of the enterprise) is formed from time to time. Namely, only once at the end of the reporting period. In addition, it is usually difficult to detail his articles.

Thus, to constantly observe this picture will not work.

This is not all the problems.

.The balance formed in accounting is subject to the principles laid down in national accounting standards dictated by the state, whose interests can determine how to collect taxes. These interests do not overlap with the interests of the direct owner, therefore, the format and content of such a balance is not suitable. Many enterprises today use international financial reporting standards that are developed in the interests of shareholders. In the modern world, dividends per share are so small that this factor ceases to matter. The value is the valuation of shares, which is formed directly by supply and demand, and not the real state of affairs in the business. The goal of the shareholders is to buy a stock cheaper and sell it more expensive. It is unlikely that such goals in reality can normally intersect with the interests of the direct owners. It turns out that even using IFRS standards we do not get an adequate reflection of the financial condition for owners. One can argue with the latest statement, but think about what the shareholder does when the company has visible problems? .. That's right, they are selling. And what does the owner do? .. Rather, trying to help solve problems. In this comparison lies the main behavioral difference and, accordingly, the difference in interests and information requirements. A Swiss friend of mine recently said: “This is for shareholders to have beautiful reports, and I want to see what’s really going on in my business.” that even using IFRS standards, we do not get an adequate reflection of the financial condition for owners. One can argue with the latest statement, but think about what the shareholder does when the company has visible problems? .. That's right, they are selling. And what does the owner do? .. Rather, trying to help solve problems. In this comparison lies the main behavioral difference and, accordingly, the difference in interests and information requirements. A Swiss friend of mine recently said: “This is for shareholders to have beautiful reports, and I want to see what’s really going on in my business.” that even using IFRS standards, we do not get an adequate reflection of the financial condition for owners. One can argue with the latest statement, but think about what the shareholder does when the company has visible problems? .. That's right, they are selling. And what does the owner do? .. Rather, trying to help solve problems. In this comparison lies the main behavioral difference and, accordingly, the difference in interests and information requirements. A Swiss friend of mine recently said: “This is for shareholders to have beautiful reports, and I want to see what’s really going on in my business.” Rather, trying to help solve problems. In this comparison lies the main behavioral difference and, accordingly, the difference in interests and information requirements. A Swiss friend of mine recently said: “This is for shareholders to have beautiful reports, and I want to see what’s really going on in my business.” Rather, trying to help solve problems. In this comparison lies the main behavioral difference and, accordingly, the difference in interests and information requirements. A Swiss friend of mine recently said: “This is for shareholders to have beautiful reports, and I want to see what’s really going on in my business.”

It’s actually worse. It turned out that 90% of Russian enterprises have no habit of generating financial statements (including a balance sheet) for direct owners, even once a period. The business owner is simply forced to be content with the information that various accounting systems form, not taking into account his interests.

Perhaps the owner, the direct owner of the business, cannot clearly articulate his information requirements. Gives this work to the level of specialists in finance and accountants, and they were taught to generate information in the interests of other parties. But he directly pays for everything. This seems like the truth, I think, recalling how I demanded one button, clicking on which, everything that is happening in my business will be visible. But in fact, he got into every little detail every day and lost sight of the general state of things. I thought I could feel him. By the way, the calculation of their own chuyku characteristic of most owners.

The second point of control of the overall picture will be the total monetary value of all changes in the time scale. We are talking about the monetary value of the economic profit of the enterprise. This is the second mandatory financial report on income and expenses (profit). Probably, it is necessary to start with constant online monitoring of real profit. So that every operation that occurred in a business would instantly reflect on its size. And this is the main point. Many believe that the problem of ensuring this condition lies in the inability to record all transactions online. It is not right! There are no big technological problems of online registration in the modern world. At least with daily discreteness. I without such difficulties achieved such results. The problem begins at the time of compiling two interrelated reports from this data. Balance sheet and income statement. Any change reflected in income and expenses changes the financial condition. Thus, these two reports cannot be divided and considered separately from each other. And the problem turned out to be exactly at the moment of their interconnected receipt. This relationship ensures the maintenance of data reliability throughout the accounting system.

If we return to the version of the natural principle of control, it turns out that you need to constantly see the total financial condition in the form of a balance sheet and a report on income and expenses, as a report on changes in this state.

We must look at the business, or rather at its digital reflection, just like what is happening outside the window. We must constantly have a general picture of the state (balance sheet) and any changes in real time (Report on income and expenses).

But that is not all.

At any moment, I should be able to concentrate on any point in this big picture. In other words, it should be possible to detail these reports, plunging into the details that interest us. An opportunity to compare these details, and also to consider from various points of view. For example, there are different points of view on valuations (for real estate: market, investment, accounting), and they can all be adequate in different versions of the analysis.

Some conclusions.

Analyzing my mistakes that led to such a sad default, after such great efforts on my part, I came to the following conclusions:

- It is necessary to reduce the amount of time spent on control and management.

- To do this, you must initially focus on the overall picture of the state and results. If everything is fine, then do not touch, let them work, and if there are problems, then already understand.

- The general picture of the status and results is visible through the reports Balance sheet and ODR (report on income and expenses). In general, I need just such a form.

- It is necessary to get an accounting automation system in your business so that all ongoing operations are recorded in real time, and the system can give me easily daily balance and ODR reports, with the possibility of any detail. The detailing of these reports is necessary in order to concentrate on the details in the right places, so the system should allow easy detailing, without additional requests and the participation of any performers.

Of course, there are other options that successful owners use.

A few examples:

You can limit the growth of a business to a level where there is still the opportunity to feel and understand the general condition through direct management of details.

You can put on the key positions of "their" people.

You can try to filter out the most important and significant details and lock their control on yourself, for example, to personally sight all cash payments over 100,000 rubles.

An interesting analogy comes to mind.

Imagine that you came to the stadium to watch a football match. Naturally, you control the big picture, concentrating on interesting details only at the right time. This is normal.

Now imagine that you are watching this match through a telescope. What will be the effectiveness of your control? And you try ...

Duck why then we control the business looking in a shameful pipe ?!

In rare cases of well-established accounting, we periodically break away from this pipe to see the general situation, which does not add much efficiency.

The question I asked myself:

There is a clear understanding of the form that I want to receive daily. I can organize everything in such a way that all transactions in accounting will be recorded in a timely manner, this is not such a difficult technical task. Those. I can provide an input accounting system. There is a magnificent and very powerful calculator in the form of a personal computer that is capable of processing millions of operations per second.

Duck why, as a direct owner, I don’t have such a system that would allow me to constantly monitor the big picture, and only if necessary immerse myself in the details?

Lyrical stumbling.

At the dawn of our business activities, my friends and I joked “Throw money into the furnace of business” (The joke arose just after the story of the taxi). Today I am amazed at how accurately this phrase reflects the problems of direct owners and direct investors who do not have the practical ability to monitor the general condition and results of their business in real time. They are for some reason identified in a number of managers and offered to use managerial accounting data in their interests. In other words, make them look constantly at the shameful pipe.

A poem from childhood comes to mind:

Englishman Mr. Hopp

Looks through a long telescope.

Sees mountains and forests,

Clouds and skies.

But he does not see anything,

That under his nose.

Suddenly he stumbled on a stone. He

plunged right into the river.

Although there is not quite an adequate analogy. Rather, in this example, the analogy is closer to criticizing the immense passion for budgeting, while there is no normal ability to control the current fact (look under your feet).

My next steps were to study existing systems.

. As a representative of small business, high hopes were assigned to 1C, then fresh from 8.0. I bought and began to implement units for all of my functioning business units. Six months later, he dismissed all 1s nicknames and rolled back the accounting system to the initial position before implementation.

Perhaps I just "don’t know how to cook it."

Very well understanding the requirements for the generated information from the source data, I began to finance the refinement of the system that I used, according to my requirements.

That's how I “dived” into IT development.

Then they began their own development, searches, experiments. And all this for the sake of one goal: to find a way of online monitoring of the general condition and results with the ability to concentrate on the necessary details, detailing and comparing this information.

The path turned out to be a long one, but the task is not easy. Along the way, I studied all the basics of accounting and financial management, became a certified specialist in IFRS. In addition, he has grown a lot as the head of IT development in an extremely Agile format.

We must already finish this article somehow.

Today I have achieved my goals. And these are no longer solutions for themselves, but real products that solve existing problems of business owners. Problems associated with the control of their own business so that direct investment does not look like "throwing money in the furnace of business."

In the near future we will resume the company’s blog on the hub and we will describe in detail all the nuances of automation of accounting in the interests of direct owners and direct investors.

The key position was described in that article that they did not understand. But the questions are not in the reporting itself, and not even in its form, but, as it turned out, in the technological capabilities of the accounting itself. These opportunities today are extremely poorly coordinated with new information technologies and the requirements of the business world.

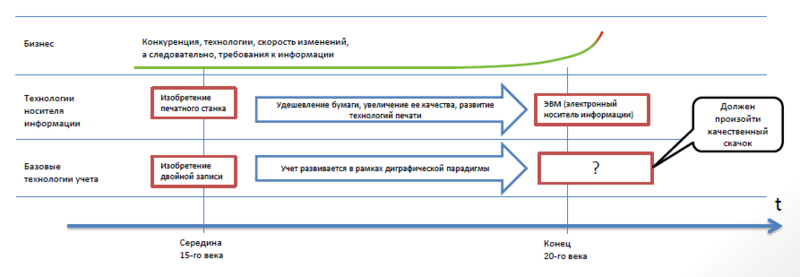

ps Another small illustration:

the idea of this illustration is to show the ripe moment for the change of the digraphic paradigm in accounting, which is today fundamental in all computer accounting systems. (Probably with the exception of 1C Enterprise).

For those who have read to the end, it may be interesting to attend a free seminar on a relevant topic. Here is a link to register.