PIN codes of bank cards. How modern technology crowds out paper mail

Today, in banking services, the expectations of customers using mobile technologies have increased significantly. The technological leap entailed the growth of instantly accessible services, which, in turn, determined the requirements of users. Banks that are actively developing mobile capabilities offer options for providing real-time financial information, as well as the latest advances in mobile technology.

According to Salesforce, a cloud-based computing center based in the United States, nearly half of youth respondents (Generation Y, or Millennials) said they wanted to receive bank SMS alerts . Of 285 users, 43% of respondents subscribed to such alerts.

This is one of those rare types of content that users are usually willing to loyally accept on their smartphone. Still would! After all, this is money that, as you know, love account and control.

When managing or viewing personal finances, the client is fully focused on studying the information that is provided through a mobile device. This is because the bank sends data that: a) is fully relevant and b) is well protected. Thus, the task of the bank is to combine seamless integration, security and mobility.

In recent years, professional SMS platforms have spent a lot of time and resources on developing A2P SMS solutions that can cope with similar tasks. Thus, specialized providers provide banks and cardholders with SMS systems for enterprises, which include a wide range of mobile financial services.

As a result of serious research and updates to the security infrastructure, the capabilities of the new generation of SMS systems have been significantly expanded, and now they include options for the delivery of insecure data for authentication - for example, PIN codes for bank cards - in real time. This type of secure SMS process (SSMS) is in many ways close to a standard service based on letters.

We all remember these bank secure envelopes with PIN codes inside. This technology is associated with some of the risks, costs, and delivery times. In addition, cardholders cannot use new cards until the carrier pigeon arrives. Joking as a joke, but such time intervals entail financial losses. Regular postal delivery takes about a week, and banks lose time providing a PIN code. Such losses make up about 2% of the expected annual costs for each first issued card. In fact, our internal studies have shown that, on average, the savings compared to standard printed and mailed data are 40-60% per PIN.

Today, with the help of a specialized provider, such a long process can be easily replaced by convenient mobile delivery of PIN codes.

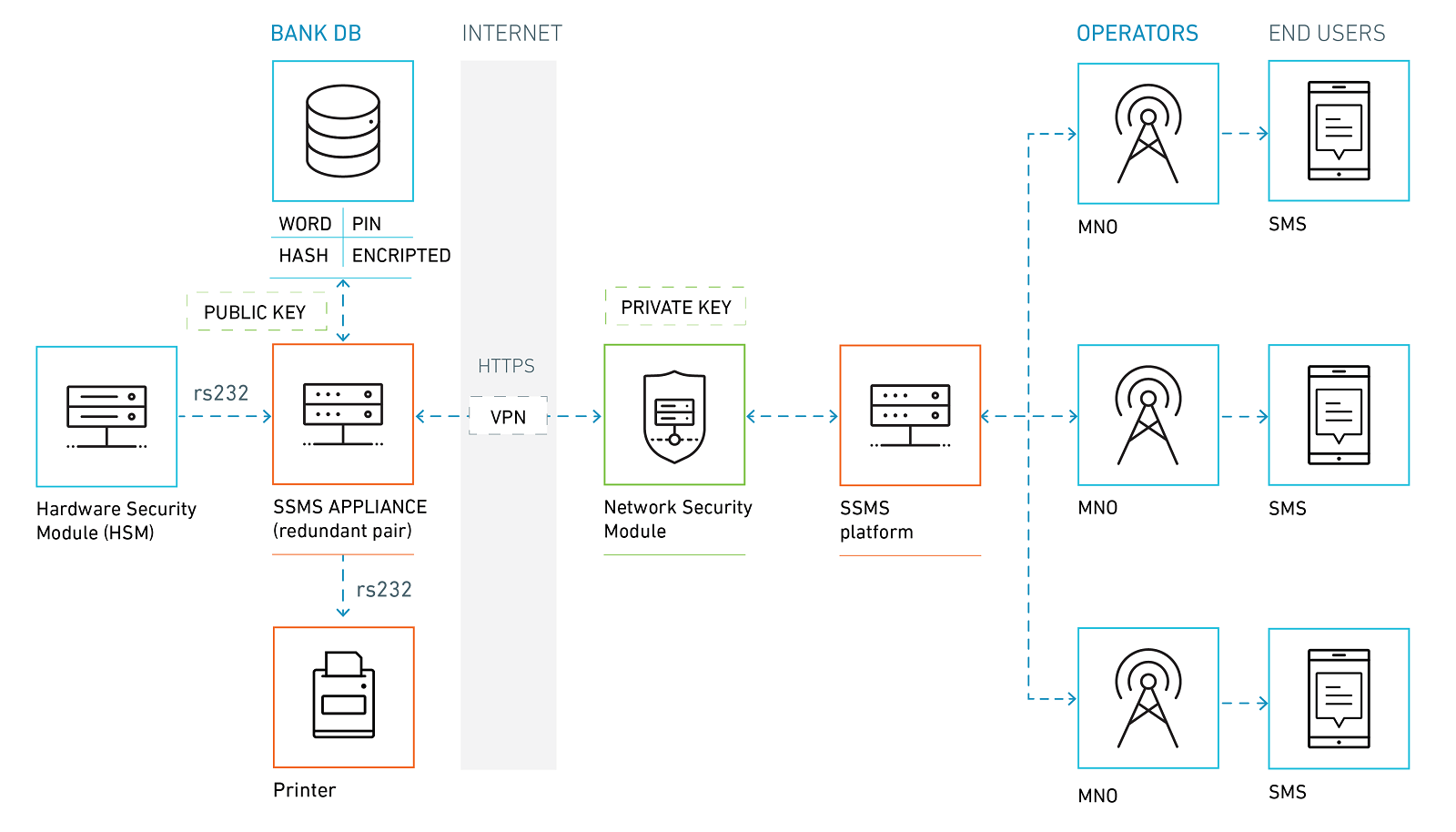

All messages sent through our SSMS platforms are delivered directly to a trusted telecommunications operator via the Payment Card Industry Data Security Standard (PCI DSS) Level 1 communication channel. This secure PIN code delivery process works without intermediaries and ensures security throughout the cycle .

RSA 2048-bit encryption, public and private keys are used to ensure security during the exchange of information. The client requests a PIN, providing the relevant secret data - a combination of the secret word, card number and phone number, which are used to select the correct PIN. After creating and encrypting the PIN code, it is stored separately from the mobile phone, and the secret word is used in the process of using the card. During this process, no one can retrieve or intercept the PIN codes for a particular card. After successful delivery, the PIN code is automatically deleted from the system.

Constantly adapting fraud detection systems for credit card transactions due to the increased number of dangerous scenarios is the main task for all major financial players. However, the incidence of fraud can be reduced by using appropriate technology.

Many cardholders travel abroad, and banks operating around the world must ensure that numerous transactions are made internationally. Using services - such as Number verification and geolocation - allows you to determine if a client is roaming and use the data to accurately assess fraud risks.

If an attempt to carry out a card transaction is registered abroad, we can determine if the client’s mobile number is roaming or not. If the number is not in roaming, then the user is probably not located abroad, and the legality of the transaction is in doubt. Thus, using the data on determining the location of an ATM, such a system allows banks to carry out additional checks before blocking a credit card in order to prevent such fraudulent scenarios.

In a world where mobile technology occupies two of the three most frequent methods of notifications from banks, preferred by a young audience, and where 27% rely entirely on mobile banking applications, it is important for banks to constantly communicate with customers on the terms and conditions proposed by customers. These technologies are becoming as familiar as voice communications or the Internet, and users expect solutions that are adequate to modern conditions from banks.

According to Salesforce, a cloud-based computing center based in the United States, nearly half of youth respondents (Generation Y, or Millennials) said they wanted to receive bank SMS alerts . Of 285 users, 43% of respondents subscribed to such alerts.

This is one of those rare types of content that users are usually willing to loyally accept on their smartphone. Still would! After all, this is money that, as you know, love account and control.

When managing or viewing personal finances, the client is fully focused on studying the information that is provided through a mobile device. This is because the bank sends data that: a) is fully relevant and b) is well protected. Thus, the task of the bank is to combine seamless integration, security and mobility.

In recent years, professional SMS platforms have spent a lot of time and resources on developing A2P SMS solutions that can cope with similar tasks. Thus, specialized providers provide banks and cardholders with SMS systems for enterprises, which include a wide range of mobile financial services.

As a result of serious research and updates to the security infrastructure, the capabilities of the new generation of SMS systems have been significantly expanded, and now they include options for the delivery of insecure data for authentication - for example, PIN codes for bank cards - in real time. This type of secure SMS process (SSMS) is in many ways close to a standard service based on letters.

We all remember these bank secure envelopes with PIN codes inside. This technology is associated with some of the risks, costs, and delivery times. In addition, cardholders cannot use new cards until the carrier pigeon arrives. Joking as a joke, but such time intervals entail financial losses. Regular postal delivery takes about a week, and banks lose time providing a PIN code. Such losses make up about 2% of the expected annual costs for each first issued card. In fact, our internal studies have shown that, on average, the savings compared to standard printed and mailed data are 40-60% per PIN.

Today, with the help of a specialized provider, such a long process can be easily replaced by convenient mobile delivery of PIN codes.

How it works?

All messages sent through our SSMS platforms are delivered directly to a trusted telecommunications operator via the Payment Card Industry Data Security Standard (PCI DSS) Level 1 communication channel. This secure PIN code delivery process works without intermediaries and ensures security throughout the cycle .

RSA 2048-bit encryption, public and private keys are used to ensure security during the exchange of information. The client requests a PIN, providing the relevant secret data - a combination of the secret word, card number and phone number, which are used to select the correct PIN. After creating and encrypting the PIN code, it is stored separately from the mobile phone, and the secret word is used in the process of using the card. During this process, no one can retrieve or intercept the PIN codes for a particular card. After successful delivery, the PIN code is automatically deleted from the system.

Security technology

Constantly adapting fraud detection systems for credit card transactions due to the increased number of dangerous scenarios is the main task for all major financial players. However, the incidence of fraud can be reduced by using appropriate technology.

Many cardholders travel abroad, and banks operating around the world must ensure that numerous transactions are made internationally. Using services - such as Number verification and geolocation - allows you to determine if a client is roaming and use the data to accurately assess fraud risks.

If an attempt to carry out a card transaction is registered abroad, we can determine if the client’s mobile number is roaming or not. If the number is not in roaming, then the user is probably not located abroad, and the legality of the transaction is in doubt. Thus, using the data on determining the location of an ATM, such a system allows banks to carry out additional checks before blocking a credit card in order to prevent such fraudulent scenarios.

In a world where mobile technology occupies two of the three most frequent methods of notifications from banks, preferred by a young audience, and where 27% rely entirely on mobile banking applications, it is important for banks to constantly communicate with customers on the terms and conditions proposed by customers. These technologies are becoming as familiar as voice communications or the Internet, and users expect solutions that are adequate to modern conditions from banks.