Ruined by the harpies. The history of high-speed trading

- Transfer

On January 28, 1790, Georgia State Representative James Jackson spoke in the rather young House of Representatives at that time at a meeting in New York. His goal was to expose high-speed traders.

“Three ships, sir,” shouted Congressman Jackson, “sailed for two weeks from this port with the intention of speculating; they are going to acquire the entire State and other securities of the ignorant ... "

Jackson scolded these people, calling them "greedy wolves ... who profit from the failures of others and use their hopeless position for selfish ends."

What terrible crime did these people commit? Murder? Cheating?

Unlikely. Jackson and one of his fellow congressmen were discussing a proposal by Treasury Secretary Alexander Hamilton that the then new US government should pay off the long-standing debts incurred by the states and the Continental Congress during the Revolution; the proposal, known as the Debt Payment Act of 1790 [eng. Funding Act of 1790 ].

Traders who learned about the discussion immediately chartered high-speed vessels to get ahead of the messengers, and began to redeem the old debt, reasoning correctly that the adoption of the Law would raise the market value of the old debt, which in some cases was sold for 10% or less of its nominal value.

Jackson was indignant: he demanded that Congress take measures to "rescue distant residents from the ruin of these robbers." The “remote inhabitants” Jackson spoke of were his voters from Georgia; although we are, in a sense, the “distant inhabitants” of Congressman Jackson, who still hope that they will be saved from the robbers.

Criticism of the information advantage owned by the “speculators” has been a common occurrence in American society from the moment the country was formed until today. Now many complain that "high-frequency traders" who use mathematical algorithms have an unfair advantage over those whose algorithms are not so good, or that their (HFT-traders) and raiding systems are faster than other players.

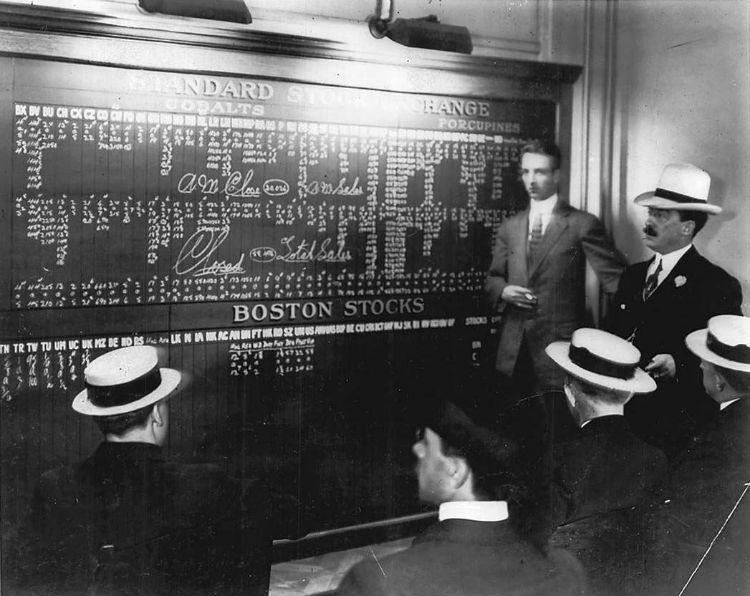

New York Stock Exchange clerks at ticker, approx. 1915

From the very beginning, there was a deep concern in society with brokers who were ready for a certain amount to buy or sell your stock, bond or your product. It was suspected that these intermediaries knew something that buyers and sellers did not know.

One way or another, this discontent is emphasized by one more significant historical fact: any technology that increases the speed of information flow was immediately adopted by the community of traders both in Europe and in the United States. Traders used all known vehicles to carry out transactions faster and put less effort into it. They were among the first to master speed boats, faster crews and private courier services. Securities trading was one of the first telegraph applications.

The development of these methods of high-frequency trading had two characteristics: 1) they significantly reduced the price difference between markets, and 2) those who mastered them more slowly bitterly complained that new technologies created an unfair advantage in relation to all market participants.

Then, as now, the people involved in the purchase and sale, and the government were desperately trying to maintain the situation at the same level. In 1792, Congress established the US Postal Service with the specific goal of "transmitting information" to "every part of the United States." By setting low rates for transporting newspapers containing market-sensitive information, all that was left was to hope that citizens would be able to keep abreast of events affecting the market and be ahead of “robbers”.

But speculators were much faster than newspapers. In 1817, when a vessel arrived in London from New York with news that caused a sharp increase in stocks, three speculators immediately jumped into the crew, heading to Philadelphia to buy up stocks. Thanks to significantly improved road quality, travel time between New York and Philadelphia was reduced to two days, leading to a lively securities trading between the Philadelphia Stock Exchange (founded in 1790) and the early version of the New York Stock Exchange (founded in 1792 )

When the station carriage broke down, they hired their own crew and arrived in Philadelphia before the news crew arrived. They immediately bought stocks, and when the mail arrived, prices rose sharply. It seemed to the laggards that the speculators paid the cabman to delay the mail.

Traders instantly created networks of high-speed “private express trains” moving along newly created highway networks and wide postal routes from New York to New Orleans. By 1825, postmaster General John McLean, outraged by speculation in the cotton market, was trying to convince Congress to shut down these high-speed trading networks and build a government system that would deliver newspapers at the same speed as letters to prevent speculators.

“By all principles of fair conclusion of transactions,” McLean wrote, “the owner of the property must be aware of its value before parting with it ...”.

The government’s attempts to block the roads for agents of high-speed traders were so serious that the United States Postal Service used high-speed horse carts, which from 1836 to 1839 connected New York and New Orleans and delivered news reports on paper from loose material instead of much more expensive newspapers.

Traders who are constantly in search of trading advantages soon shortened the time period for transmitting information - they stopped using horses and carts! In the late 1830s, a broker from Philadelphia, William Bridges, had a personal signal station between New York and Philadelphia, broadcasting stock market news to him and his patrons (and no one else). The signals were transmitted using an “optical telegraph”, which consisted of a series of shields on a support mounted on a hill, which could be seen through a telescope. Messages indicate that they could transmit stock market information anywhere from New York to Philadelphia in 10-30 minutes. In the 1830s, this was high-speed trading!

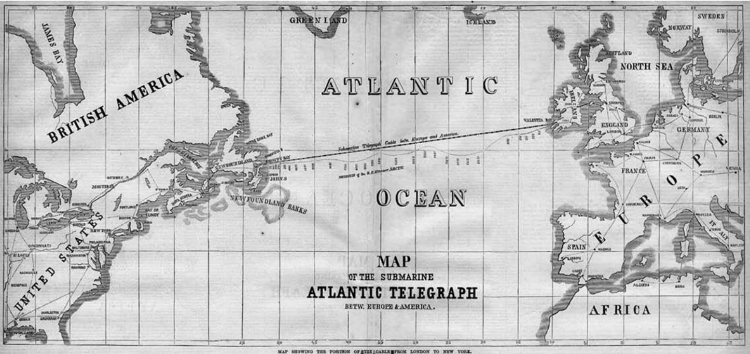

Map showing the location of the transatlantic cable between New York and London

It is not surprising that complaints began to come from speculators from New York who were not involved in this system and, until that time, had enjoyed a significant advantage. Philadelphia residents were also unhappy. When the system was closed after the telegraph appeared in 1846, a local newspaper report wrote that “speculators who contributed to the creation of the telegraph were responsible for many ingenious moves in the Philadelphia stock and commodity markets. Undoubtedly, speculators paid well to its creators. ”

Undoubtedly. Unfortunately, the “organized” community of traders did not strive much for openness. In its initial stages, the NYSE (New York Stock Exchange, then known asNew York Stock and Exchange Board ) did not allow the public to listen to trading sessions (the sessions were inaccessible to the public until 1869). Competing traders (over-the-counter traders working literally from the outside) who intended to sell trading information on the NYSE were furious that they could not be near the exchange. In 1837, the NYSE discovered that over-the-counter traders drilled a hole in the brick wall of a stock exchange building in order to eavesdrop on the course of trading.

While the public was pondering how to get ahead of fast horses, a new technology appeared on the arena that turned trading into a field of truly high speeds: a telegraph that came into use after 1844.

He was the greatest invention of his time. It took time to produce newspapers, and for the most part they were published at regular intervals. But the telegraph worked constantly, and it could be used for personal communication.

He was a high-speed trader's dream come true. The first customers were stock brokers and speculators selling lottery tickets. On March 3, 1846, the New York Herald reported that "certain groups of individuals used telegraphs to speculate on stocks in New York and Philadelphia."

As expected, using the telegraph to transmit “secret knowledge” caused outrage. Several inventors of the first telegraphs were forced to stop their experiments, warning that they could be prosecuted for distributing information faster than mail. Leading inventor of telegraph Samuel F.B. Morse supported the introduction of telegraph into mass production for personal and public purposes, in particular, to protect it from use for speculation.

Everything was in vain. Congress ultimately refused an attempt to introduce a telegraph system, partly because competition for having information on market changes and the limited length of wires available at that time were quite sensitive factors. This competition arose not only between traders, but also between them and their main competitor - the press.

In the early 1800s, modern newspaper production was born, and one of the main goals of the first such newspapers was the accelerated publication of financial news. James Gordon Bennett Sr., who founded the New York Herald in 1835, one of the first "tabloid" publications in the country, emphasized that the nascent press had destroyed the minority information monopoly:

“Speculators should not have an advantage in getting news before the general public gets it,” he said.

Suddenly, newspaper publishers got boats. And optical telegraphs. At the Trade Journal Publishing House Journal of Commerce ], formed in 1827 with the goal of providing news to the financial community, had at its disposal high-speed boats that were met by vessels arriving from abroad. Optical telegraph systems, like the private systems between Philadelphia and New York, were laid between Sandy Hook, New Jersey and New York City and informed the editors of the arrival of the ships.

The Commerce Magazine and its rival, The Courier and Enquirer, even organized competing mail services on cross-country horses, operating between New York and Philadelphia, and later reaching Washington. Even pigeons were involved in their rivalry: a group of tabloid newspaper owners paid $ 2,000 for a flock of carrier pigeons to send news about Philadelphia, Washington, and Baltimore.

In turn, traders were given great support for a certain price. One news entrepreneur, Daniel Craig made a fortune selling traders information from European news. Combining pigeons with couriers of express services, he received news from European steamships that moored in harbors from Halifax in Nova Scotia to Boston, earlier than anyone else. Then the information was transmitted by telegraph to New York.

An attempt to convey a message using carrier pigeons, 1898

Craig was so good at gathering information before the others that he was later invited to work at the newly formed New York Associated Press. The press was dissatisfied with the traders and agents supplying them with information. Telegraph companies, which were believed to have close relations with traders, displayed particular hostility; the editors complained that the telegraph fell into "bad hands."

Getting the first information was so valuable that during the time of cooperation with telegraph companies, some speculators after receiving the news could cut the telegraph wire! Due to the fact that the telegraph companies were one of the first to receive valuable information, some of them supplanted all speculators and began to do this business on their own. This went on for decades: when a civil war broke out, some Western Union employees became rich in the gold market, using early information about news from the front.

Forty years later, the telegraph was still the main instrument of stock speculators. In 1887, the president of Western Union said that 87% of the company's revenues came from speculators in the stock and commodity markets and those who made races.

Acquiring a faster ship that would cruise the Atlantic Ocean was even more profitable for traders. In the mid-19th century, the Atlantic Ocean could be crossed in eight days, and anyone who could learn important news from across the ocean could profit more quickly from this. A vivid example: when in 1865 it became known in New York that the Southerners had lost the war, financier Jim Fisk chartered several ships faster than the postal ships of the time, and sent them to London, ordering their brokers to sell short-term Confederation bonds. When the defeat of the southerners became known in London, the value of bonds fell to zero, and Fisk, of course, became rich.

Just as the telegraph was immediately mastered by stock traders in the United States, stock trading and other commercial activities were one of the first uses of the transatlantic cable. The first successfully laid cable began to be used in 1866 between New York and London and significantly reduced the information advantage that traders had previously used; brokers could now telegraph to London and receive confirmation within five minutes. Soon, the difference in securities prices began to decline.

The stock ticker, which appeared in 1867, became the next greatest electronic device, immediately mastered by the community of traders. Until its appearance, exchange transactions, as a rule, were carried out with the help of “runners” [eng. "Pad shovers"] - the boys who ran back and forth from the stock "hole" to the brokerage houses. He had a huge superiority over the telegraph for several reasons: 1) traders no longer needed to be physically in the stock "hole"; 2) its appearance has reduced operating costs; 3) he helped to disseminate information continuously, in real time; and 4) his invention reduced the number of annoying intermediaries such as telegraph companies and newspaper editors. It is not surprising that journalists and editors were worried that the introduction of a ticker would force them out of the lucrative trade in financial news.

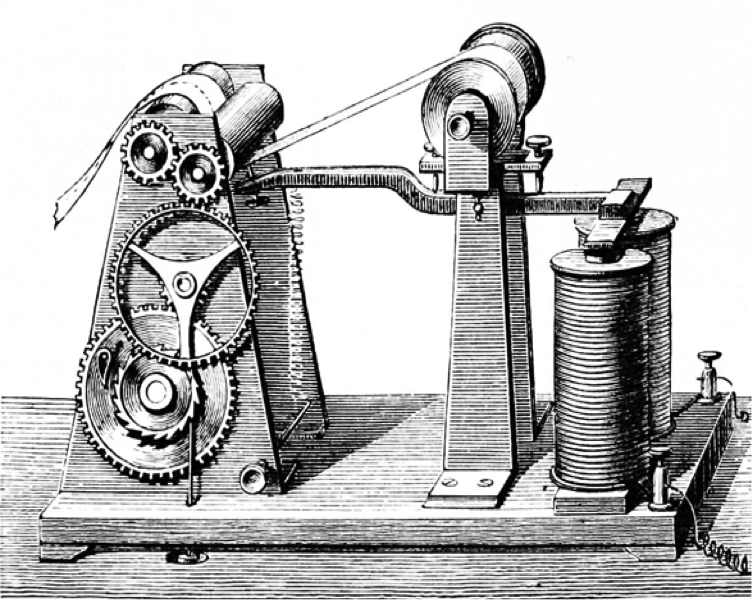

Morse telegraph drawing, which appeared in Popular Science Monthly, approx. 1872-1873

The ticker was not invented by Thomas Edison, but the latter made a number of significant improvements in its design, including the invention in 1873 of a quadruplex, which allowed four messages to be transmitted simultaneously on one wire. Western Union found this additional bandwidth to be used well: they leased lines to private networks controlled by Wall Street companies. By 1879, these firms had connections with their telegraph-based offices in Boston and Philadelphia, and by 1881 in Chicago. These private lines were faster than the "public" telegram. In addition, they were more reliable and kept secret.

All of Wall Street happily invested its money in this project, since the quickest access to market data, as always, played a crucial role in making a profit: by 1894, brokers on the Boston Stock Exchange had learned about transactions on the NYSE within 30 seconds .

Among other things, the use of the stock ticker marked the beginning of a new wave of speculation in the stock market, which this time was carried out by working class investors who began to speculate through the newly created over-the-counter brokerage houses, also equipped with ticker machines. Professional traders, who had previously enjoyed a tremendous advantage, complained bitterly: "The erratic distribution of stock quotes in beer bars and other establishments has greatly impeded doing business," said John T. Denny, a broker from New York in 1889. “Everyone could go to the bar and look at the quotes.”

Despite the fact that over-the-counter brokerage houses were engaged in fraud (there was no actual transfer of shares, therefore, "depositors" merely bet against other players in the brokerage "kitchen"), many laid out a tidy sum for quick telegraphic communications; in 1887, the NYSE discovered that one of the over-the-counter brokerage houses received stock quote data seven minutes before the “normal” data transfer via a ticker, thanks to the support of Western Union.

This went on further, with the advent of the exchange trading system in the 1860s, the invention of the telephone (first tested by Bell in 1876; by 1878, the NYSE had its own telephone in the pit), and somewhat later, with the creation of airmail, a computer in the 1950s , punch card in the 1960s, with the first appearance of electronic trading, when in 1971 the Nasdaq exchange started its work, and algorithmic trading in the 1990s. The same disputes arose: someone received information earlier than the others, and some could bid because they had a faster ship / horse / carriage / telegraph line / computer connection / algorithm.

A man using the new “high-speed” ticker ticker, 1930. The initial signature read: “Western Union ordered 10,000 [tickers] and started installing them in brokers' offices across the country. The company will spend $ 4.5 million to try to speed up the transfer of stock quotes ... to keep up with the new era, when six or eight million shares are traded on the stock exchange per day. ”

The reactions of society and government to the “thirst for speed” of traders differed, but one factor remained almost unchanged: the informational advantages, after mastering any new technologies, seemed to disappear over time. From the very beginning, perspicacious observers have noted this fact.

Let us return to Congressman Jackson and disputes in 1790, the main problem of which was the question of whether Congress should take measures and prohibit “speculation” (lease of high-speed vessels). After the protests of several congressmen who claimed that it was impossible to stop such activity, and it always has been, Jackson objected that he understood very well that “there was speculation in the fund of every country that had a state debt,” but in this case it was different: people traded, owning information that others did not. This, he said, was vile and frankly unfair.

One congressman, Elias Budino, a spokesman for the state of New Jersey, agreed: while speculation had risen to a “troubling mark," he said, the only effective solution to stop it would be to "recognize public debt how the data in the hands of lenders will gain their true meaning. ”

Budino argued that the only way out was to acknowledge that the amount of debt had increased, and added that the active dissemination of information — greater openness — was the most effective salvation. Budino fully recognized that the early beneficiaries of any new technology (in this case, the creation of faster ships) received the initial advantage. Despite this, the advantages in question were short-lived, as others adopted new technologies. This is especially evident in cases with the telegraph and stock ticker.

So what happened to the debate around the debt and the "robbers" trying to cash in on it? The bill was passed in 1790, the US government claimed responsibility for the debt of the Continental Congress and the states, and the new government issued bonds.

Immediately followed by a lively trade in these bonds among wholesalers and auctioneers, those same "robbers" whom Congressman Jackson complained about. This business turned out to be so profitable that some began to specialize in trading these very securities. Two years later, on May 17, 1792, 24 brokers gathered at a plane tree on Wall Street and allegedly tried to form a monopoly on the sale of this debt and several shares available for trading, promising to "give preference to each other in their negotiations." This group of people has become what is now known as the New York Stock Exchange.

Bob Pisani - CNBC Channel Financial Correspondent