The course of lectures "Startup". Peter Thiel. Stanford 2012. Lesson 3

- Tutorial

This spring, Peter Thiel ( by Peter Thiel ), one of the founders of PayPal and the first investor FaceBook, held a course at Stanford - "Start-up". Before starting, Thiel said: “If I do my job correctly, this will be the last subject that you will have to study.”

One of the students of the lecture recorded and posted the transcript . In this habratopic, 9e9names translates the third lesson. Editor of Astropilot .

Lesson 1: Challenging the Future

Lesson 2: Again, Like in 1999?

Lesson 3: Value Systems

Lesson 4: Last Step Advantage

Lesson 5: Mafia Mechanics

Lesson 6: Thiel Law

Lesson 7: Follow the Money

Lesson 8: Presenting an Idea (Pitch)

Lesson 9: Everything Is Ready, But Will They Come?

Session 10: After Web 2.0

Session 11: Secrets

Session 12: War and Peace

Session 13: You Are Not a Lottery Ticket

Session 14: Ecology as a Worldview

Session 15: Back to the Future

Session 16: Understanding Yourself

Session 17: Deep Thoughts

Session 18: Founder - Victim or God.

Occupation 19: Stagnation or Singularity?

Lesson 3: Value Systems

In many ways, the story of the 90s is a story of widespread misconceptions in understanding what value is. The concept of “value” passed into the psychosocial plane, what was considered valuable by people was considered valuable. To get away from this herd of delusions of the past decade, we must make an effort and find out whether it is possible to determine the objective value of the business, and if so, how to do it.

If we return to the reasoning from the first lecture, we note that there are a number of questions that may lead us to ideas about value. These questions are highly personified. For example: What can I do? Which of these do I think is valuable? WHAT THE OTHERS DO NOT DO? If we take globalization and technology as a basis, as the two main coordinate axes of the 21st century, then all these questions can be synthesized into one high-level question: which companies whose obvious value has not been founded yet?

A slightly different view of technology - the transition from 0 to 1, if we return to our previous terminology - can be obtained from a financial and economic point of view. This point of view can also shed light on the concept of “value”; we will consider it now in more detail.

I. Great technology companies

Great companies do three things. First, they create value.

Secondly, they constantly adhere to the chosen path.

Thirdly, they become monopolists in the production of at least one of the values that they create.

The first of these statements is obvious. Companies that do not create anything of value simply cannot be great. Only the creation of values in itself will not make the company great, however, without this, they certainly will not become great.

Great companies are stable. Or, more accurately, they are durable. They do not exist on the principle of "create value and soon disappear." Consider hard drive companies from the 80s. They have added value by producing new and more advanced devices. But the manufacturing companies themselves did not stand the test of time - other companies came to replace them. It’s not worth building the boundaries between the values that you can produce and the values that you can capture and hold.

Finally - and this is no coincidence - you must capture a large part of the market of the value that you produce, after which your company will become truly great. A scientist or mathematician can create many enduring values through his discoveries. But to capture a significant part of this value market is a completely different matter. Sir Isaac Newton, for example, could not capture most of the values that he created in his work (apparently, I mean "Mathematical Principles of Natural Philosophy" - approx. Translator). Take the aviation industry as a less abstract example. Airlines, of course, create value, as life becomes better thanks to their existence. These companies create many jobs. However, airlines alone never really made money. Certainly among them there are better and worse companies. But probably not one of them can be considered truly great.

II. Rating

One of the ways that many people are trying to use for an objective assessment of the company's value is to search for a multiple analogue. To some extent, this works. However, care must be taken to avoid the use of social heuristic evaluations instead of rigorous analysis, since the analysis is usually based on current agreements and conventions. If you are creating a company as part of a business incubator, then you must take into account existing conventions. If participants invest their money in the company before reaching the mark of $ 10 million, then the company can be valued at $ 10 million. There are many formulas that include metrics such as the monthly number of page views or the number of active users. Somewhat more stringent are the factors in calculating income. As a cost estimate for a software company, its tenfold annual income can often serve as the basis. Guy Kawasaki (Guy Kawasaki ) proposed a rather unique (and possibly useful) equation:

preliminary estimate = ($ 1 million * number of engineers) - ($ 500 thousand * number of managers)

The largest common multiple is the price-earnings ratio, also known like a P / E ratio or just PER. The PER coefficient is calculated as follows:

PER = market value (per share) / profit (per share)

In other words, this is the price of the share in relation to the company's net profit. PER is a well-known characteristic, but it does not take into account the growth of the company.

To account for growth, you can use the PEG coefficient - the price / profit ratio taking into account growth. That is,

PEG = (market value / profit) / annual profit growth.

Thus,

PEG = PER / annual revenue growth.

The lower the PEG value for a company, the slower it grows, and, therefore, the lower its value. A higher PEG value typically characterizes a company's greater value. In any case, the PEG should be less than one. PEG is a good metric to keep track of your company's growth.

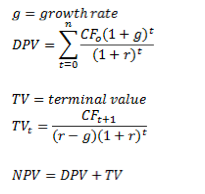

We received a cost analysis at a given time. However, in reality it is an analysis of time factors. During the analysis, you look not only at the cash flow for the current period, but also at future years. Summing up all the values, you make a profit. But the same amount of money today is worth more than in the future period. Thus, the analysis does not take into account the decrease in the cost of money over time (TVM), since the future carries a large number of risks. The basic formula for calculating the TVM value is as follows:

r - discount rate

CFt - cash profit in the accounting year

DPV - current value including discount rate

Everything becomes more complicated when the value of cash profit is not a constant. For cash gross variable, the following formulas are used:

g - growth rate

TV - residual (post-forecast) value

Thus, to determine the value of a company, you calculate the DPV or NPV coefficients for the next X (or infinite number) years. In general, you need to get g more than r. Otherwise, your company does not grow at a sufficient pace to keep up with the discount rate. Of course, in a growth model, growth should ultimately slow down. Otherwise, the value of the company will eventually reach infinity - and this is unlikely.

The value of firms in the Old Economy era is defined differently. For a company in recession, core value is determined by the short term. Investors who adhere to the cost strategy pay attention to cash gains. If the company can maintain the current level of cash profit for 5-6 years, then this is a good investment. Then, investors simply hope that this box-office profit - they determine the value of the company - will not decrease faster than they expected.

With technology companies and other fast-growing firms, this is not the case. Firstly, most of them lose money. When the growth rate g, as we indicated in our calculations, is higher than the discount rate r, then the main value of the technology business falls on the distant future. Indeed, in a typical case, ⅔ values are produced between ten and fifteen years of the company's existence. This is contrary to common sense. Most people - even those who work in startups today - think in models of the Old Economy, where it is necessary to create value right off the bat. The focus should be on companies with explosive growth in the coming months, quarters or, less commonly, years. This is too short a portion of the timeline. Models of the Old Economy are valid only for the Old Economy. This does not work for technology companies and other fast-growing businesses. Nevertheless, the culture of startups today defiantly ignores, if not opposed, thinking at intervals of 10-15 years.

PayPal can be a great illustration. Within 27 months, its growth was 100%. Everyone knew that the growth rate would decrease, but still the growth was higher than the discount rate. The plan was that the maximum cost would be achieved in the 2011 area. Despite the fact that the discount rate planned in the long-term planning mode turned out to be lower in fact, and the growth rate is still at a quite healthy mark of 15%, it’s clear today that PayPal’s maximum price should be expected no earlier than 2020.

LinkedIn is another good example of the importance of the long term. The startup’s market capitalization is currently around $ 10 billion, and the stock is bidding with a very high P / E of around 850. But analysis of discounting cash gains gives the following estimate: from 2012 to 2019, the cost of the service will reach around $ 2 billion. dollars, while the remaining 8 billion reflect an estimate of 2020 and beyond. LinkedIn assessment, in other words, only makes sense in the long run, i.e. if the ability to produce value in the next decade is being evaluated.

III. Durability

People often talk about the “first mover advantage”. But focusing on this problem has consequences: you can take the first step and disappear. The danger is that you may just not be so absorbed in all of this to succeed, even if you end up generating values. Leaving the last word to yourself is even more important than being a pioneer. You must be set up for a long-term presence. In this aspect, business is something like chess. Grandmaster Jose Raul Capablanca put it this way: in order to succeed "you must learn the endgame, and then everything else."

IV. Benefits

Basic economic ideas about supply and demand can be used in discussions about gaining profit. A common understanding is that market equilibrium is reached at the point where the supply and demand curves intersect. When analyzing a business from this point of view, you get two possible options: perfect competition or a monopoly.

In conditions of perfect competition, none of the firms in the industry has economic profit. If profit appears, then firms enter the market and profit leaves. If firms begin to suffer losses, they leave the market. This way you are not making money. And not only you, no one earns them. In conditions of perfect competition, the scale of your activity is negligible in comparison with the scale of the market as a whole. You can slightly affect demand. But, in general, you are in the position of a passive market participant.

But if you are a monopolist, then the whole market is yours. By definition, you are the only producer of any value. Most economic textbooks spend a lot of time discussing perfect competition. They tend to consider examples of monopolies as internal elements or as minor exceptions to perfect competition. The world, as these books say, is in equilibrium by default.

But perhaps the monopoly is not some strange exception. Perhaps the conditions of perfect competition by default exist only in economic textbooks. Let us question whether monopoly is really an alternative to the generally accepted paradigm. Consider the great technology companies. Most of them have one decisive advantage - such as economies of scale or the unique low cost of production - which is at least an important step towards the establishment of monopolies. A pharmaceutical company, for example, can use the patent protection of a particular drug, which allows it to trade at a higher price than the cost of manufacturing this drug. Truly valuable enterprises are business monopolists. They promote the production of values that are sustainable over time,

V. Competitive ideology

A. PayPal and competition

PayPal revolved in the payment business. There is significant economies of scale in this business. You could not compete with large credit card companies directly; it was necessary to somehow undermine their foundations. PayPal did this in two ways: through technical innovations and through innovative products.

The main technical problem that PayPal had to solve was fraud. When it became possible to make payments via the Internet, much more fraud was revealed than anyone expected. It was also unexpectedly difficult to fight him. There were many different enemies in The War Against Fraud. For example, there was the Carders World organization, which built an anti-utopia of the collapse of the foundation of Western Capitalism with anonymous transactions. There was a particularly annoying hacker named Igor, who was evading the FBI outside their jurisdiction (Igor was later killed by the Russian mafia). Ultimately, PayPal was able to create really good software to deal with fraud problems. the name of this software product is “Igor”.

Another key innovation was the reduction in the cost of processing funding sources. For example, the costs of obtaining information on the status of bank accounts by users are compiled from various factors. But as a result of modeling how much money was left in the account, PayPal can make advance payments, more or less bypass the Automatic Clearing system, and make payments instantly from the user's point of view.

These are just two examples from PayPal. Your business will look different. The conclusion is that it is absolutely important to have some decisive advantage over existing services that seem to be the best. Because even a small number of competing services quickly paves the way for very fast competitive dynamics.

B. Competition and monopoly

Whether competition is good or bad is an interesting (and underestimated) question. Most people assume competition is good. A standard economic narrative focused on perfect competition defines competition as a source of progress. If competition is good, then its complete opposite — monopoly — should be bad. Indeed, Adam Smith accepted this point in his work The Wealth of Nations:

People engaged in the same business are rarely found, even in fun and entertainment, but their conversations always end with a conspiracy against society or the search for some mechanisms to increase prices.

Understanding this point of view is important if only because it is so widespread. But to give an exact definition of why monopoly is bad, hard enough. This, as a rule, is simply taken for granted. But, probably, it is worth touching on this issue in more detail.

B. Verification of monopoly

The Sherman Antitrust Act states:

Possession of monopoly power is not illegal, if it is not accompanied by elements of anti-competitive behavior.Therefore, in order to understand whether a monopoly is legal or not, we must figure out what “anti-competitive behavior” is.

The Department of Justice uses three tests to evaluate monopolies and monopoly prices. The first is the Lerner index, which gives an idea of the extent to which a particular company has market influence. The index value is calculated as:

(price - maximum cost) / price.

The index is measured in the range of values from zero (perfect competition) to one (monopoly). Intuitively, the company's market influence means a lot. But in practice, the Lerner index is difficult to evaluate, since for this you need to know the market price and the planned maximum cost. Of course, technology companies themselves know the indicators and can independently evaluate their own Lerner index.

The second is the Herfindahl-Hirschman index. It uses the size of firms and industries in order to assess how much competition exists in the market. In fact, this is the sum of the squares of the sales shares of each company in the industry. The lower the index value, the more competition in the market. A value below 0.15 indicates a market with a high degree of competition; a value from 0.15 to 0.25 indicates that the market is very saturated. A value of more than 0.25 indicates a high saturation and, possibly, monopolization of the industry.

And finally, there is also the saturation coefficient of m-firms. You take 4 or 8 of the largest firms in the industry and the sum of their market shares. If together they make up more than 70% of the market, then we can talk about high market saturation.

G. What is good and what is bad in monopoly

First, the cons: monopolies, as a rule, reduce production volumes and set higher prices than firms in competitive markets. The same statement may not be entirely true for some natural monopolies. In some areas, there is a monopoly of scale, which is slightly different. But, in general, monopolists set prices rather than respond to demand. Also, the phenomenon of price discrimination is characteristic of monopolies, since monopolists can capture a larger market by setting different prices for groups of goods. Another object of criticism is the fact that monopolies stifle innovation, because can make a profit both by introducing any innovative technologies, and by doing without them. The monopoly business will grow without the development of any new technologies.

But the opposite argument can also be made, also regarding innovation. In fact, a monopoly can spur innovation. If a company creates each new product much better than the previous one, then what's wrong with the fact that the price of this product is higher than the maximum cost of production. The resulting delta is a reward to the creators of new things. A monopolist company can also afford improved long-term planning and calculate project financing more deeply, since employees have a greater sense of stability than in conditions of perfect competition, where profit is zero.

D. Biases of perfect competition

It is interesting to speculate why most people have a strong prejudice in favor of perfect competition. It is difficult to argue that economists idolize this system. Even the very concept of “perfect competition” seems to be associated with normative meanings. We do not call it “fierce competition” or “merciless competition”. And this is probably not by chance. Perfect competition is claimed to be perfect.

For starters, perfect competition can be attractive because it is easy to model. This probably explains a lot, because the whole economy rests on modeling the real world in order to simplify interaction with it. Perfect competition can also seem like a very meaningful model because it is cost-effective in a static world. Moreover, it is a very hot commodity from a political point of view, which also does not hurt.

But perfect competition, it is quite expensive. And she seems to be mentally healthy. All benefits are social, not individual. But people who are really involved in this business hold a different point of view - in fact, very many of them want to make real profits. The most serious criticism of perfect competition is that it is meaningless in a dynamic world. If there is no balance - everything constantly moves around - you somehow capture some of the values that you produce. And with perfect competition this is not implied. Perfect competition, therefore, eliminates the question of values - doing business is hard and you can never get anything as a result of this struggle. Controversy: the more competition, the less chance you have of capturing any value.

If you think this way, you can conclude that the concept of "competition" is overrated. Competition can be what we are taught and what we do unquestioningly. Maybe you competed with each other at school. Then comes the tougher competition in college and graduate school. And then rat race in the real world begins. An accurate, but hardly a unique example of intense professional competition is the competition model of young lawyers from the best law universities in large law firms. You graduate from law school, say, at Stanford, and then go to work for a large firm that pays you really good money. You work incredibly hard, trying to become a partner, until you achieve this, although you may not succeed. The alignment is not in your favor, and perhaps you will leave before how do you get a chance to mess up big. A startup’s life can be complicated, but a little less meaningless in terms of competitiveness. Of course, some people like to participate in the competition, no less than in law firms. But such a minority. Ask someone from the majority, and they will say that they never want to compete again. Of course, winning by a wide margin is much better than being in conditions of merciless competition, if you are able to bear it. that they never want to compete again. Of course, winning by a wide margin is much better than being in conditions of merciless competition, if you are able to bear it. that they never want to compete again. Of course, winning by a wide margin is much better than being in conditions of merciless competition, if you are able to bear it.

Globalization provides a very fertile ground for the development of competition. It’s like in the track and field sprint, when one runner wins, and the rest lag behind for the hundredth seconds, stepping on the heels of the winner. From the viewer's point of view, it’s great and exciting. But for a real process, this is an unnatural metaphor.

If for the phenomenon of globalization it would be necessary to come up with a heading, then it would be "The world is flat." We hear this from time to time, and, indeed, globalization begins with this idea. Technology, on the contrary, comes from the idea that the world is Mount Everest. If the world is really flat, then this turns into insane competition. Connections with a negative meaning, for example, “race for survival,” are suitable for determination. You have to accept a pay cut because people in China are willing to work for less. But what if the world is not just crazy competition? What if most of all the objects in the world are unique? In high school, we usually have high hopes and ambitions. And too often, the college knocks these hopes out of us. People say that they are only small fish in the great ocean. Failure to acknowledge this is a sign of immaturity. Acceptance of the truth - that our world is great, and you are just a grain of sand in it - is considered very wise.

However, this cannot be considered psychologically healthy. And this, of course, does not motivate at all. Maybe what you really want to do is make the world smaller. Maybe you do not want to work in large markets. It may be much better to find a small market, succeed in it and take possession of it. And at the same time, the only business idea that you hear so often is: the larger the market, the better. This is absolutely, completely wrong. The restaurant business is, for example, a huge market. And this is not a good way to make money.

The problem is that the ocean is a lot of water, and it’s hard to know exactly what's inside. Perhaps there are monsters and predators that you do not want to meet. You want to stay away from dangerous areas. But you cannot do this if the ocean is too big to control it. Of course you can be the best in your class, even if this class is very large. In the end, someone must be the best. But, nevertheless, the larger the class, the more difficult it becomes to be the first number. Therefore, clearly defined, understandable markets are more difficult to master. Therefore, we return to the importance of the question that we formulated in the second paragraph: which companies, the value of which is obvious, have not yet been founded?

E. Venture Investors, Networks, and Final Thoughts

Where are the venture capital flows? As a rule, this is not a very large business area. Rather, investors rely on a very limited number of people who are already their representatives. That is, they have access to a unique network of entrepreneurs, this network is the main value, it is supported by relationships. Venture capital is not massive, but personal and often specific. This is directly related to big business. The PayPal network, as it is called, is built on friendships that have been formed over a decade. This is a kind of franchise. But this is not a unique phenomenon, such dynamics characterizes, perhaps, all large technology companies, those that represent monopolies in the markets. All of them are not engaged in mass business. The core of their relationship. They create value. They are durable.

From the translator:

I ask for translation errors and spelling in PM. I also remind you that this text is a translation, its content is copyright, and the author's opinion may not coincide with mine.

I repeat once again that I translated 9e9names . Editor of Astropilot . All thanks to them.