More than 7,000 FINTECH startups worldwide will go through the process of consolidating the financial services industry.

- Transfer

Fintech enthusiasts can argue endlessly about how high the results were achieved by representatives of the financial technology industry in the financial services industry and in general, and in their allegations there will even be some truth.

Indeed, more than 7 thousand FINTECH startups from around the world prove in practice their ability to go beyond the usual level of service for consumers. Moreover, the size of venture capital investments in the sphere of fintech around the world in 2016 grew by 11% to $ 17.4 billion . If we talk about 2017, today we already have Fintech alternatives that look more attractive than any similar banking service.

However, there is one process that will inevitably put an end to this victorious march. The consolidation of resources (financial, human, technological and ideas) in the financial services industry will restore the balance of power in the market and bring it to its original state, in which most of the market will be controlled by a very limited number of companies.

In this regard, it should be noted that the areas of payments and crediting are likely to be among the first segments, which by their example will demonstrate the futility of a wide variety of players. More than 1 thousand payment startups around the world are trying to offer the same basic service under different signs. At the same time, payments, loans and financing are segments that can boast the most stable financing and the greatest variety of offers. Inside the payment segment, mobile wallets and payments are the most popular activity. According to the MEDICI database , about 34% of payment FINTECH companies already work in it.

Meanwhile, conducted by Gallup in 2015The study indicates that only 13% of American adults have digital wallets on their smartphones. Most of these 13% (76%) in general or practically did not use them to make any purchases in the last month (at the time of the survey). The fragmented consumer experience and separately existing islands of mobile solutions constitute an obstacle to the development of the entire segment.

Anyway, this situation has a bright side. The legacy of the current Fintech-cacophony will be transformed business models, new corporate cultures, significant automation and individual solutions that can lead to lower business costs (for example, investment applications), rethinking the role of the user interface in the financial services industry, expanding business opportunities due to cross-border payments, cheaper remittances, advances in user profiling (for example, alternative credit ratings), behaviorists for advanced security solutions, invisible payments. All these solutions can revive e-commerce, provide a high level of consumer loyalty and give impetus to the growth of business sales.

The gloomy expectations about the future of a large number of teams seeking to make innovative changes in the segment of financial services technologies have several reasons. In many respects, consolidation scenarios are caused by the current state of the most popular fintech markets and the wise strategic decisions made by major players.

In this way, they will regain control of cutting-edge developments and niche markets.

It is noteworthy that approximately 75% of startups that have received venture capital funding fail . Of course, the numbers may differ for different markets, but on the whole the same tendency can be traced: a huge number of venture enterprises fail for one reason or another: lack of experienced investors, incorrect positioning in the market, problems with regulators, unclear marketing plan, mistakes of leaders , mistakes in financial management and so on. All these flaws lead to the fact that companies that have shown themselves from the best side are fighting with each other to win their market share.

However, even these 25% of the most effective players are far from being turned into “unicorns”. Large financial institutions have developed a wise strategy aimed at mitigating the apparent threat from niche markets. Its essence is very simple and corresponds to the old rule “keep friends close, and enemies even closer.” To bring startups closer, major players establish various tests, incubators, accelerators, innovative laboratories, investment funds and partnerships. As soon as the debate about the place of fintech in the financial services industry subsided and the development vector was set, thriving and mutually beneficial partnerships between fintech startups and institutions (in insurance and banking) came to the site of observation and collection of information.

Visa, one of two processing companies controlling the international payments market, recently acquired a stake in Klarna, a Swedish unicorn startup operating in the field of e-commerce. After concluding an investment agreement, the companies announced the start of a strategic partnership aimed at jointly launching new products. Klarna is not the first strategic acquisition of Visa. Earlier, the payment giant also invested in two other fast-growing financial startups - Square and Stripe. In 2016, both Visa and MasterCard only in the United States processed transactions totaling $ 4.3 trillion — twice the same figure a decade ago.

According to some reports, at least halfFinancial services companies operating around the world are planning to purchase fintech startups in the next 5 years. In addition, 8 out of 10 institutions are considering the possibility of entering into strategic partnerships with companies engaged in direct lending. With this in mind, we can say that digital money transfer platforms and other firms will change the face of the e-commerce industry.

Even traditional fintech companies choose this path. Paypal recently purchasedSwift Financial to strengthen its position in the segment of lending to small businesses, in which competition has significantly increased over the past 2 years. PayPal launched its first product for working capital supply in 2013. Since then, new strong players like Square and Kabbage have appeared on the market, offering their own lines of credit for small businesses.

It is expected that technology leaders will also become more aggressive with regard to strategic acquisitions, as this will help them get into new niches and strengthen their positions in existing areas of activity. For example, Daniel Doderlein , director general of a Norwegian financial tech start-up Auka, gave an example with IBM, which, according to his data, will go shopping next year. In an interview with CNBCHe said that large companies will begin to acquire separate “fragments” and “niche verticals” - vendors offering their services in specific markets - since larger players will need technologies that allow them to fully use the directive of the new European payment directive PSD2 . According to Doderlein, technology giants, who have long and consistently cooperated with banks, will begin to show interest in the influx of new FINTECH firms.

In one of the most attractive fintech markets in the world - China (to be more precise, it’s rather Hong Kong rather than mainland China, and yet) there are only two monopolists in the field of mobile payments - Alipay and Tenpay - who own 91% of domestic of the market.

More important, influential companies around the world often try to expand their influence by expanding to other markets and new lines of business, as this step strengthens their position and gives them a competitive advantage in niche markets compared to smaller companies. For example, Ant Financial, a digital payments subsidiary of Chinese Alibaba, was willing to pay $ 1.2 billion for a deal with MoneyGram. As explainedThe Financial Times, MoneyGram, is the company's first major acquisition in the United States, whereas over the past few years, Ant Financial has already made a number of investments in mobile payment companies in India, Thailand and South Korea. And the Alipay service, originally established for servicing e-business Alibaba, today dominates the huge Chinese mobile payment market.

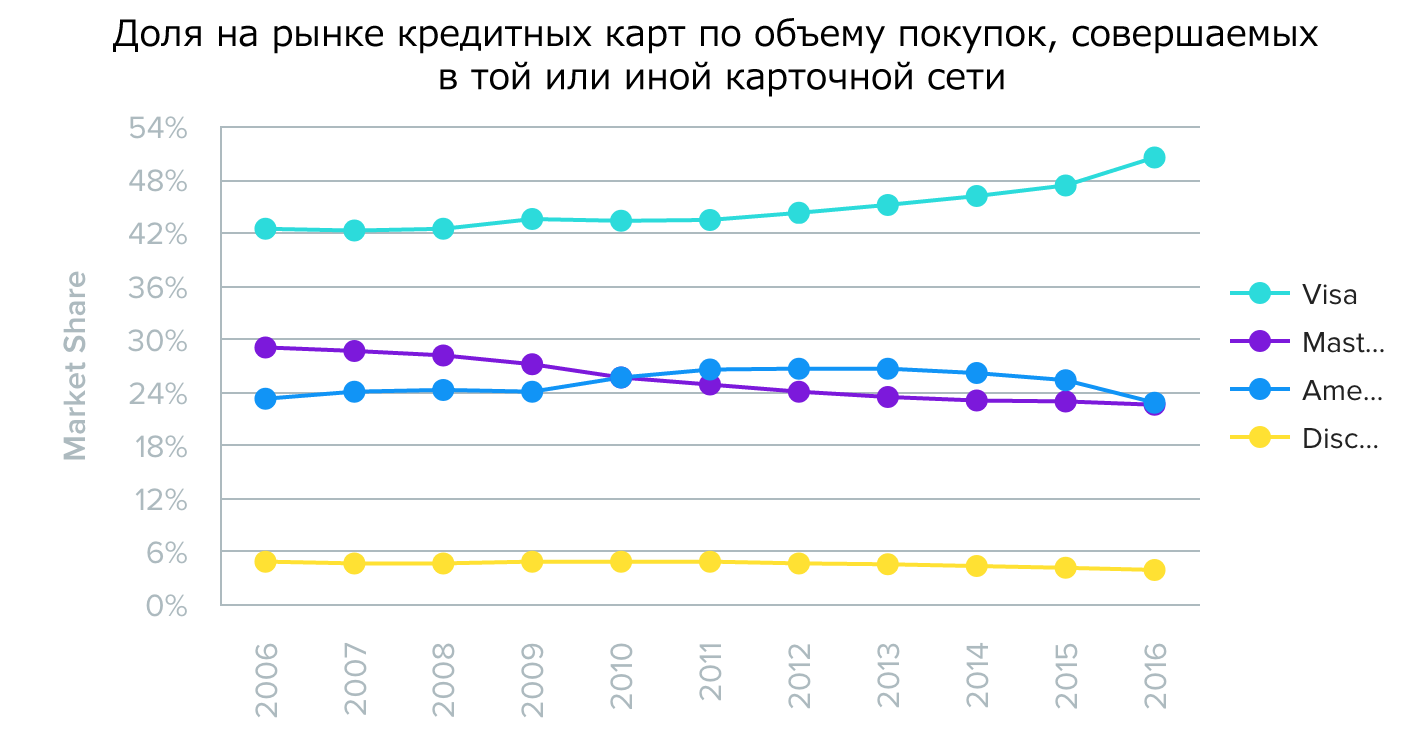

In the US, the 4 largest card networks - Visa, MasterCard, American Express and Discover - in fact dictate terms and conditions for using credit and debit cards to consumers, WalletHub believes, citing statistics to confirm . Visa and MasterCard possessa significant advantage in terms of the prevalence of accepting their cards worldwide. As for Amex and Discover, then according to the same WalletHub, they offer their service to simplify payment, issuing cards for users directly, without intermediaries.

Source: WalletHub

Source: WalletHub

Source: WalletHub

Indian payment service Paytm, which Alipay owns through One97, increased its market share to 67.9% in six months, while the share of its competitor Freecharge was 11.4%. As explained by the publication Financial ExpressThis figure represents the volume of transactions recorded by payment wallets operators in 10 major cities of the country. Another 5% of the market got AirtelMoney and Mobikwik.

Recently, the World Economic Forum released a document titled “Going beyond Fintech: A Pragmatic Evaluation of Innovative Capacity in Financial Services”, the authors of which, in particular, assume that the market will consolidate in the future, the most successful companies will increase their market share Ultimately, consumers will establish relationships with fewer suppliers. Against the background of consolidation, product distribution will be the most likely entry point for large technology companies due to their deep technological knowledge.

The organization lists the possible consequences that financial institutions will face in the event of consolidation:

Market consolidation means that fintech companies that do not have a large customer base and the ability to scale quickly will have to look for niches if they want to succeed in becoming distributors. Existing distributors can, on the contrary, help fintech companies compete with more experienced market participants, relying on the uniqueness and narrow specialization of the products offered.

Indeed, more than 7 thousand FINTECH startups from around the world prove in practice their ability to go beyond the usual level of service for consumers. Moreover, the size of venture capital investments in the sphere of fintech around the world in 2016 grew by 11% to $ 17.4 billion . If we talk about 2017, today we already have Fintech alternatives that look more attractive than any similar banking service.

However, there is one process that will inevitably put an end to this victorious march. The consolidation of resources (financial, human, technological and ideas) in the financial services industry will restore the balance of power in the market and bring it to its original state, in which most of the market will be controlled by a very limited number of companies.

In this regard, it should be noted that the areas of payments and crediting are likely to be among the first segments, which by their example will demonstrate the futility of a wide variety of players. More than 1 thousand payment startups around the world are trying to offer the same basic service under different signs. At the same time, payments, loans and financing are segments that can boast the most stable financing and the greatest variety of offers. Inside the payment segment, mobile wallets and payments are the most popular activity. According to the MEDICI database , about 34% of payment FINTECH companies already work in it.

Meanwhile, conducted by Gallup in 2015The study indicates that only 13% of American adults have digital wallets on their smartphones. Most of these 13% (76%) in general or practically did not use them to make any purchases in the last month (at the time of the survey). The fragmented consumer experience and separately existing islands of mobile solutions constitute an obstacle to the development of the entire segment.

Anyway, this situation has a bright side. The legacy of the current Fintech-cacophony will be transformed business models, new corporate cultures, significant automation and individual solutions that can lead to lower business costs (for example, investment applications), rethinking the role of the user interface in the financial services industry, expanding business opportunities due to cross-border payments, cheaper remittances, advances in user profiling (for example, alternative credit ratings), behaviorists for advanced security solutions, invisible payments. All these solutions can revive e-commerce, provide a high level of consumer loyalty and give impetus to the growth of business sales.

The gloomy expectations about the future of a large number of teams seeking to make innovative changes in the segment of financial services technologies have several reasons. In many respects, consolidation scenarios are caused by the current state of the most popular fintech markets and the wise strategic decisions made by major players.

Financial institutions will swallow fintech companies to completely rethink their services and approach

In this way, they will regain control of cutting-edge developments and niche markets.

It is noteworthy that approximately 75% of startups that have received venture capital funding fail . Of course, the numbers may differ for different markets, but on the whole the same tendency can be traced: a huge number of venture enterprises fail for one reason or another: lack of experienced investors, incorrect positioning in the market, problems with regulators, unclear marketing plan, mistakes of leaders , mistakes in financial management and so on. All these flaws lead to the fact that companies that have shown themselves from the best side are fighting with each other to win their market share.

However, even these 25% of the most effective players are far from being turned into “unicorns”. Large financial institutions have developed a wise strategy aimed at mitigating the apparent threat from niche markets. Its essence is very simple and corresponds to the old rule “keep friends close, and enemies even closer.” To bring startups closer, major players establish various tests, incubators, accelerators, innovative laboratories, investment funds and partnerships. As soon as the debate about the place of fintech in the financial services industry subsided and the development vector was set, thriving and mutually beneficial partnerships between fintech startups and institutions (in insurance and banking) came to the site of observation and collection of information.

Visa, one of two processing companies controlling the international payments market, recently acquired a stake in Klarna, a Swedish unicorn startup operating in the field of e-commerce. After concluding an investment agreement, the companies announced the start of a strategic partnership aimed at jointly launching new products. Klarna is not the first strategic acquisition of Visa. Earlier, the payment giant also invested in two other fast-growing financial startups - Square and Stripe. In 2016, both Visa and MasterCard only in the United States processed transactions totaling $ 4.3 trillion — twice the same figure a decade ago.

According to some reports, at least halfFinancial services companies operating around the world are planning to purchase fintech startups in the next 5 years. In addition, 8 out of 10 institutions are considering the possibility of entering into strategic partnerships with companies engaged in direct lending. With this in mind, we can say that digital money transfer platforms and other firms will change the face of the e-commerce industry.

Even traditional fintech companies choose this path. Paypal recently purchasedSwift Financial to strengthen its position in the segment of lending to small businesses, in which competition has significantly increased over the past 2 years. PayPal launched its first product for working capital supply in 2013. Since then, new strong players like Square and Kabbage have appeared on the market, offering their own lines of credit for small businesses.

It is expected that technology leaders will also become more aggressive with regard to strategic acquisitions, as this will help them get into new niches and strengthen their positions in existing areas of activity. For example, Daniel Doderlein , director general of a Norwegian financial tech start-up Auka, gave an example with IBM, which, according to his data, will go shopping next year. In an interview with CNBCHe said that large companies will begin to acquire separate “fragments” and “niche verticals” - vendors offering their services in specific markets - since larger players will need technologies that allow them to fully use the directive of the new European payment directive PSD2 . According to Doderlein, technology giants, who have long and consistently cooperated with banks, will begin to show interest in the influx of new FINTECH firms.

The number of strong players in some of the most advanced fintech hubs is very limited.

In one of the most attractive fintech markets in the world - China (to be more precise, it’s rather Hong Kong rather than mainland China, and yet) there are only two monopolists in the field of mobile payments - Alipay and Tenpay - who own 91% of domestic of the market.

More important, influential companies around the world often try to expand their influence by expanding to other markets and new lines of business, as this step strengthens their position and gives them a competitive advantage in niche markets compared to smaller companies. For example, Ant Financial, a digital payments subsidiary of Chinese Alibaba, was willing to pay $ 1.2 billion for a deal with MoneyGram. As explainedThe Financial Times, MoneyGram, is the company's first major acquisition in the United States, whereas over the past few years, Ant Financial has already made a number of investments in mobile payment companies in India, Thailand and South Korea. And the Alipay service, originally established for servicing e-business Alibaba, today dominates the huge Chinese mobile payment market.

In the US, the 4 largest card networks - Visa, MasterCard, American Express and Discover - in fact dictate terms and conditions for using credit and debit cards to consumers, WalletHub believes, citing statistics to confirm . Visa and MasterCard possessa significant advantage in terms of the prevalence of accepting their cards worldwide. As for Amex and Discover, then according to the same WalletHub, they offer their service to simplify payment, issuing cards for users directly, without intermediaries.

Source: WalletHub

Source: WalletHub

Source: WalletHub

Indian payment service Paytm, which Alipay owns through One97, increased its market share to 67.9% in six months, while the share of its competitor Freecharge was 11.4%. As explained by the publication Financial ExpressThis figure represents the volume of transactions recorded by payment wallets operators in 10 major cities of the country. Another 5% of the market got AirtelMoney and Mobikwik.

In the future, consumers will interact with fewer suppliers.

Recently, the World Economic Forum released a document titled “Going beyond Fintech: A Pragmatic Evaluation of Innovative Capacity in Financial Services”, the authors of which, in particular, assume that the market will consolidate in the future, the most successful companies will increase their market share Ultimately, consumers will establish relationships with fewer suppliers. Against the background of consolidation, product distribution will be the most likely entry point for large technology companies due to their deep technological knowledge.

The organization lists the possible consequences that financial institutions will face in the event of consolidation:

- All companies will try to become distributors of both their products and products of other companies. Their success will depend on existing markets and whether they can become a “well-known company”.

- A distributor of products may have to fight for consistency and maintaining the same level of quality against the background of the growing fragmentation of the world of network-connected devices.

- Held market participants will gain an advantage in the race for becoming eligible as distributors due to their large customer base. However, those who fail to become distributors of products will have to face a decrease in the profitability of products, which will be due to the transformation of products into a typical streaming product.

Market consolidation means that fintech companies that do not have a large customer base and the ability to scale quickly will have to look for niches if they want to succeed in becoming distributors. Existing distributors can, on the contrary, help fintech companies compete with more experienced market participants, relying on the uniqueness and narrow specialization of the products offered.