"Take-off debit" in the 95th or what lessons the mobile payments market can learn from the history

- Transfer

Sometimes in the process of surfing on the expanses of the global network, you can stumble upon materials that you immediately want to share. This material for us at PayOnline , which provides services for the integration of various payment methods on websites and mobile applications, was the material from the PYMNTS publication. The author of this article gave a detailed analysis of the history of the development of the payment card industry in the United States, starting in 1995, listing the main milestones to which attention should be paid to mobile payment solutions wishing to learn from the positive experience of technology existing on the market a little longer. Below you can see the translation of the original material.

Sometimes in the process of surfing on the expanses of the global network, you can stumble upon materials that you immediately want to share. This material for us at PayOnline , which provides services for the integration of various payment methods on websites and mobile applications, was the material from the PYMNTS publication. The author of this article gave a detailed analysis of the history of the development of the payment card industry in the United States, starting in 1995, listing the main milestones to which attention should be paid to mobile payment solutions wishing to learn from the positive experience of technology existing on the market a little longer. Below you can see the translation of the original material.For more than 10 years now, mobile payment market players have been trying to “launch” mobile payments, but this has barely got off the ground. Karen Webster believes that now is the time to stop doing narcissism and seek inspiration in the technologies of the future. Instead, we should turn to the history of the payment industry, because there is already an example of a successful exit from a similar situation. It is about 1995, when there was a successful "launch" of debit payments. So, let us call for the aid of the 95th debit card muse, which will help us understand what we can do to ensure that mobile payments finally “take off”.

If we seriously want to make mobile payments ubiquitous, it may be time for us to stop looking to the future in search of ideas and inspiration and instead look back and take a closer look at the success of another payment innovation that changed the world several decades ago.

Or rather, let's go back to the year 1995.

1995 was the year when Toy Story, Apollo 13 and Batman Forever beat all possible box office records. The album Fantasy Mariah Carey was at the top of the pop charts, and the 26-year-old millennials who are now working in FINTECH start-ups drank juices from solid sachets in kindergarten.

And in 1995, debit cards “took off”.

“It's all great, but what does all this have to do with attempts to“ start ”mobile payments today?”, You ask.

Meet - check cards

In the early 1990s, if the parents of modern advanced millennials wanted cash from an ATM, they used a special piece of plastic called an ATM card that they carried in their wallet. ATM cards were issued by banks, were tied to the check accounts of their owner, and on the back they had a magnetic stripe. The systems of electronic cashless transfer of funds (abbreviated EPS), which made it possible to withdraw money using these cards, had two distinctive features: a) money could only be withdrawn after entering a PIN code. From here comes another name for this payment method - “pin debit”; b) after withdrawing money, funds are immediately debited from the card holder’s checking account.

Pin card accounting systems are usually managed by regional operator companies, such as STAR, PULSE, NYCE and Shazam, for example. And usually, these operators were established jointly by banks and were subordinate to them. Visa and MasterCard also managed their own national ATM networks - Plus and Cirrus, respectively, which appeared separately from each other in 1982 and helped to process card transactions made outside of local or regional networks.

At the turn of the 90s, about 20 years after the first publicly available ATM appeared in the US, their number in the country totaled 80 thousand. By that time, almost all of them were part of a regional or national network, which allowed consumers to use their ATM cards for withdrawing money at almost any ATM in the country.

At the same time, the first merchants began to appear - mostly supermarkets, which equipped their cash registers with keyboards for entering PIN codes, which allowed cardholders to use them to pay for purchases. However, such sellers were the exception rather than the majority of outlets at that time did not have such keyboards.

But all of them possessed electronic cash terminals provided to them by card network operators in the 1980s. These terminals allowed consumers to use any card issued by a bank in any store, regardless of which bank was its issuer. They were connected to a whole group of clearing networks that provided the correct mutual settlement between banks and merchants.

What the card networks failed to achieve was the success of widespread distribution of debit products.

Both Visa and MasterCard tried to launch debit products from the very beginning in the mid-70s. Consumers then wrote tons of checks - about 24 billion - so replacing paper checks with plastic cards seemed like an elementary task.

But the banks were not interested in this. They received a profit from checks and therefore did not want to rock the boat. Consumers, it seemed, were also not interested in using plastic, as they looked at it as a kind of loan, which could only lead to the rapid depletion of money in a checking account.

Therefore, when the 90s came, the US debit market looked like this. There were a large number of consumers who liked to pay for purchases with money from their checking account. As a result, they wrote checks to pay for any purchase. Yes, millennials who never held a checkbook in their hands, now you will know that in the stone age of the 90s, people not only used them, but also did it regularly. For example, writing checks to pay for weekly grocery shopping was as common as cash purchases.

In addition, there were many people carrying ATM cards with them. In fact, it was all the same consumers who wrote checks. There were also regional EPS networks, which united ATMs of almost all banks in the country and thus allowed using any cards at almost any ATM. According to estimates of the mid-90s, consumers had about 220 million cards in their hands.

It should be noted that the “pin debit” was not in great demand among sellers. And this despite the fact that the pin networks could boast a very attractive and friendly offer for them, which included a reduction in the cost of both transactions and fees for returns. In addition, the need to enter a PIN code, along with the availability of funds in the account in real time, reduced the risk that the client would not be able to pay for the purchase, and the seller, in turn, would be able to reject the transaction on the spot. And in order to get all these advantages, he only needed to find money somewhere to install a pin keyboard.

Card networks, however, were widely distributed among sellers thanks to electronic terminals that made it possible to accept payments using magnetic stripe cards issued by most of the participating banks. They also could boast not only a large number of partner banks, but also a large user base with checking accounts. Nevertheless, the banks seriously thought about the possibility of making a profit from debit products due to the competitive advantage of the “pin debit” - almost zero operating commissions. Networks needed a debit product that consumers could use in the numerous outlets connected to their system. They also needed to find a way to attract banks to cooperate, which would allow them to use the full potential of the checking accounts base.

And that's what happened next.

Pin keyboards and advertising with Bob Dole

EPS networks have offered sellers a decline in already low payment commissions - a measure that was supposed to stimulate the installation of pin keyboards. And this measure worked: sellers began to install a pin-keyboard. Now consumers could easily use the ATM cards already in their wallets, on the back of which the EPS network logo was depicted, at each outlet with a pin-keyboard to pay for purchases instead of writing checks.

At the same time, Visa launched an aggressive campaign designed to encourage the 50 largest card issuers to issue a different type of debit card - subscription. Instead of a pin-code for identifying the identity of the buyer, such a card used his signature. The subscription debit card had its advantage: it could be used in terminals already installed in a large number of stores. Operations on it were carried out in offline mode, with the settlement carried out within 2-3 days after the actual moment of their execution. Bank customers received a card with a magnetic strip, which, just like an ATM, allowed paying for purchases in stores and withdrawing money, eliminating the need to write checks.

In order to interest banks, Visa introduced for issuers the same interbank commissions as for credit cards, thus showing how they can turn a novelty into a source of profit. The payment network also sponsored a large advertising campaign with Dayon Sanders, Bob Doleand Duffy Duck, to convince consumers that they could use their “check card” from any vendor who accepted Visa cards. In a relatively short period of time, Visa signed agreements with a whole bunch of different banks. By agreeing to cooperate with the company, the banks deprived themselves of the opportunity to work with the MasterMoney product from MasterCard, which debuted a few years later, which gave Visa a good starting advantage in the subscription debit card market. Unlike the situation with credit cards at that time, banks could issue only one payment provider cards, and they had to choose between MasterCard or Visa.

EPS offer was focused on sellers. By installing a pin keyboard, they received a stream of new customers with ATM cards and significantly reduced both the cost of each transaction and the risk of fraud.

The Visa offer was focused on banks: they received a new profit channel, replacing checks with a single card, which allowed their customers to shop at stores and withdraw money at any ATM. In addition, the Visa offer also made irrelevant use of ATM cards.

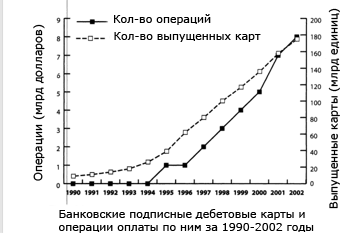

In 1991, the number of debit cards in the United States did not exceed some 7.6 million units. By 1997, this figure had risen to 58 million. The volume of the debit card market during this period increased from 5.9 billion to 58 billion dollars. In 1996, a year after the launch of its campaign, Visa reported about 1.2 billion debit card transactions totaling about $ 50 billion. The number of pin-keyboards increased from several thousand in the early 90s to 500 thousand in 1996. In 1998 - just two years later - this figure rose to 2 million. The

In 1991, the number of debit cards in the United States did not exceed some 7.6 million units. By 1997, this figure had risen to 58 million. The volume of the debit card market during this period increased from 5.9 billion to 58 billion dollars. In 1996, a year after the launch of its campaign, Visa reported about 1.2 billion debit card transactions totaling about $ 50 billion. The number of pin-keyboards increased from several thousand in the early 90s to 500 thousand in 1996. In 1998 - just two years later - this figure rose to 2 million. The debit market “took off”.

And this happened through the use of two very different strategies at once.

In an attempt to talk about the “take-off of debit” first of all, and not about the debit market as such, I deliberately missed a lot of details that make the market history interesting and even a bit contradictory.

However, if you need some light summer reading about the history of the debit market, I suggest you get acquainted with the 8th chapter of the book Paying With Plastic (Evans, Schmallensee, ed. MIT Press, 2005). Yes, I miss many equally interesting and significant details in this material, but I do it, because today we are talking a little about something else.

What is important for today is that as representatives of the payment industry, we obviously know how to “bring” new products to the market or “put” new technologies into the hands of consumers and sellers, simply because we already did before.

The history of electronic terminals and debit cards confirms this.

Therefore, it is time to learn the lessons that history teaches us and call upon our debit museum to help, finally, to launch mobile payments.

This can be done with the help of five simple ideas.

We must not allow technology to impose a development strategy.

The debit was launched due to the most efficient use of existing technologies that were easily available or were already available on the vendor side at the time of their connection. MasterCard and Visa simply took advantage of what was available to the entrepreneurs and what the latter had already paid for earlier, while representatives of the EPS system themselves provided their customers with the technology to accept payments using cards. It is quite natural that no one from the very beginning expected that the sellers would start to put money into the new technology from their pockets.

In the case of NFC and mobile payments, everything is completely different.

Unfortunately, we spent the last 10 years trying to force mobile payments into a certain template of the NFC shop option, which offers customers to change a couple of clicks on the screen for a swipe and therefore they do not have much hype. Pay the bills for this must sellers. In fact, we simply allowed technologies to manage the strategy of launching mobile payments, instead of creating real value at the intersection of the consumer with a mini-computer in hand and the seller who wants to use the possibilities of this computer to sell more goods.

The launch strategy using NFC also ignores several dependencies at once: the need to gain a critical mass of both sellers with NFC terminals and buyers with suitable devices and cards, as well as the importance of providing enough obvious motivation for both groups to make them want to start using the new products . In fact, we have neither the one, nor the other, nor the third, and the launch of mobile payments is left to the mercy of fate: everyone simply hopes that one day something will happen that will get the process off the ground and that by this time we will have the necessary infrastructure.

That is, this approach simply does not take into account one important factor for success: a critical mass.

Lack of critical mass leads to critical state.

Ignoring this factor makes the economic benefit of investing in mobile payments very ephemeral and not obvious. This is probably the very reason why those who want to offer businessmen financial and any other assistance in installing contactless terminals, as was the case in the 80s with credit and in the 90s with pin debit cards, were not found. There are probably too many doubts about the ability of NFC to provide a critical mass in a short amount of time for potential players to believe that all this makes sense.

However, the need for a critical mass does not explain the take-off of the debit market. Pin and subscription debit cards have eliminated the "friction" between sellers and buyers. The process of working with checks was very time-consuming: buyers constantly toiled with their discharge, which slowed down the checkout process, while sellers were very expensive to maintain them, including because of the risks associated with fraud. Debit cards allowed consumers not only to pay with cards that they already carried with them to withdraw money from ATMs, but also to do it in a way they were used to, which was not very different from paying with credit cards. As for the sellers, their novelty has eliminated the process of servicing checks, replacing them with already familiar credit card terminals or new easy-to-use PIN-keyboard.

Both pin and subscription debit card networks made the most effective use of the potential interest of consumers in the new technology. They managed to realize a profitable offer from a sufficient number of sellers, which made it possible to unleash the flywheel of innovation. They also did not embarrass consumers by talking about the fact that their debit cards can work only in a few stores here and there, and only if they carry them in purple leather wallets.

That is, in order for mobile payments to reach a critical mass, we need solutions that can work on all devices, all operating systems, all sales channels, with very different technologies and with very different calculation units. It also means that launch strategies for mobile payments should focus primarily on analyzing consumer demand and provide an offer that is interesting enough for them that could fully meet this demand.

The price must be justified

Pin and subscription debit cards had two different pricing approaches.

Pin debit networks used low commissions to ensure a sufficient level of supply, which was expressed in equipping sellers with pin-keyboards. And it worked. The number of institutions using the pin-keyboard, for three years has increased four times.

Subscription debit networks offered an incentive to banks to create large consumer demand: sellers could already accept payment by this method, that is, the offer was available. By providing banks with an incentive to advertise “check cards” among their customers and without requiring sellers to make any investments in cash-in-sales payment terminals, Visa was able to launch the subscription debit card market, even though commissions for merchants were significantly higher. than with pin debit networks. Banks have sent millions of customers to sellers who can use banking products to pay for their purchases at any store.

The current situation with mobile payments is much more complicated, given the lack of a “standard” way of organizing their reception in traditional stores. The launch of mobile payments requires a deliberate approach. The cost of applying new technology should be consistent with its value and the benefits it provides. Sellers will also want the new product to not require long and costly changes in the payment acceptance process.

Sellers must be part of the game

Starting one or another payment project traditionally requires taking into account the opinions of several interested parties. Payment networks should be able to please the banks that collect commissions for each operation from sellers. They also need to be confident that consumers will be sufficiently interested in a new product, and sellers will accept card products so that customers have the opportunity to use them at any place of purchase. Each of the parties to this process is very important, and maintaining a balance between them is one of the main and difficult tasks of the players in the payment industry.

Whenever the term “vendor-friendly” is used in the payment industry, we are usually talking about reducing the cost of processing card payments. The history of confrontation between networks and salespeople around this subject is as old as the world, and litigation on commissions fed and provided work for more than one generation of lawyers. The results, however, can be considered very successful for entrepreneurs, because in all this time they have managed to save billions of dollars in reducing commissions.

It is possible that the solution to the problem of “launching” mobile payments will give us the opportunity to rethink the meaning of this term. Perhaps the most “sellers-friendly” strategy is simply to maximally simplify the process of accepting all types of mobile payments that customers use or want to use.

The “friendliness” of the pin debit, for example, was to provide consumers, who already owned a certain card, with a new place of its use - stores. As a result, sales went up. However, more important in this example is that pin debit cards have eliminated the main inconvenience - the need to stand in a queue of people, each of whom holds a checkbook. Subscription debit cards “flew up” because sellers did not need to make any investments in the new method of accepting payments: they were ready to serve millions of cardholders from the very beginning. Visa also spent $ 37 million on advertising in 1996 to raise consumer awareness, create excitement and demand. But even if no new customer entered the store with a card in hand as a result of all these actions, the sellers would still have remained “at their own”, because they were not invested in technical improvements. The risks were small, and the rewards were great. In short, we have a good example of “friendliness towards sellers.”

Attention to all innovators in the field of mobile payments: go back to the blackboard and think about a mobile payment scheme that would really be “friendly to sellers”!

Let certainty be the killer chip of mobile payments.

Every innovation needs its own "killer chip". For smartphones, it has become an app store, for debit cards - continuity on the part of sellers. For mobile payments, this is a certainty.

The Apple Pay system, which is a good example of the thoughtful application of NFC technologyIt works with thousands of card issuers in the United States and is available at 2 million outlets across the country. And yet, most observers believe that the launch of Apple Pay has failed. When Apple claims that its product accounts for 3 of the 4 contactless payments made in the country, it actually calls itself the largest player in the "frog-pad", with which you can now compare the entire sphere of mobile payments. The technology continues to exist, but the process of its distribution is declining, and this has been happening for the past 18 months. 19 out of 20 consumers who could use Apple Pay do not. And 4,000 consumers, quarterly polled by the resource pymnts.com, claim that they no longer even try to use the product simply because it is too often unavailable in their favorite places.

The most successful player in the market today, accepting mobile payments in retail outlets, is the coffee giant Starbucks, which, however, guarantees its customers the possibility of mobile payment in each of their establishments. Starbucks uses QR codes and loyalty psychology to stimulate mobile payments , which today provide more than 20% of all its profits. And his “mobile ordering ahead” service now provides 5% of total orders. Starbucks customers always know that they can use the company's mobile application to pay for an order at any of the network establishments, and now they can also make it in advance and avoid standing in line.

For the same reason, it will be very interesting to watch the development of Walmart Pay. The versatility of the Walmart.com application, which is available in all stores of a large American chain, will make it possible to simplify the life of more than 100 million customers who make purchases on a weekly basis.

That is why certainty is important and its use as a “slaughter chip” of mobile payments will allow them to gain momentum.

When consumers are confident that their mobile devices can not only help in making purchases, but also act as real tools for their payment, mobile payments will finally “take off”. As for sellers, the main goal of their business is to sell goods and make a profit, rather than participate in the life of the payment industry and its development, so they start to be interested in this or that method of payment only when they become confident that customers in In fact, they will appear and start using this method for paying for purchases.

And at the moment, of all the most modern payment methods, it is plastic cards that best fit this description.

Continue to follow PayOnline processing blog updates ., and be among the first to read the most important materials from foreign sources, translated specifically for users of Geektimes.