Talent vs. Luck: The Role of Chance in Success and Failure

Recently, I came across an interesting work by Italian scientists about the greatly underestimated role of luck and chance in our lives. Unfortunately, I did not find the full version in Russian (maybe I was looking badly?), But I really wanted to share what I read with my non-English speaking friends. Therefore, rolling up his sleeves, he set about his artisanal translation. The authors, Alessandro, Alessio and Andrea, kindly allowed to publish it in the public domain, so if you are interested, welcome to cat.

The authors

- A. Pluchino - Department of Physics and Astronomy, University of Catania and Catania Branch of the National Institute of Nuclear Physics, Italy; alessandro.pluchino@ct.infn.it

- A. E. Biondo - Department of Economics and Business, University of Catania, Italy; ae.biondo@unict.it

- A. Rapisard - Department of Physics and Astronomy, Catania University and Catania Branch of the National Institute of Nuclear Physics, Italy; Center for the Study of Complex Systems, Vienna; andrea.rapisarda@ct.infn.it

annotation

To a large extent, the dominant meritocratic ( meritocracy is the principle of management, according to which the most capable people should occupy leading positions, regardless of their social origin and financial wealthThe model of highly competitive Western cultures originates from the belief that success largely, if not completely, depends on personal qualities such as talent, intelligence, skills, resourcefulness, hard work, perseverance, hard work, or risk taking. Sometimes we are ready to admit that a certain share of luck can also play a role in achieving significant material success. But, in truth, the importance of external forces in individual success stories is often underestimated. It is well known that intelligence (or, in general, talent and personal qualities) in a population has a Gaussian distribution, while the distribution of values - often seen as a measure of success - usually follows a power law (Pareto law), when most are poor and there is a negligible number of billionaires. This discrepancy between normally distributed inputs that have a normal level (averaged talent or intelligence) and a constant distribution at the output suggests that somewhere behind the scenes there is an invisible component. In this paper, on the basis of an extremely simple and toy agent modeling, we make the assumption that such a component is an ordinary accident. In particular, we show that, while life success really does require a certain amount of talent, the most gifted people almost never reach the highest peaks of wealth, being overtaken by mediocre, but much more successful personalities. As far as we know To this contradictory common sense result - although implicitly assumed between the lines there is a lot of literature in which - a quantitative assessment was given here for the first time. This allows you to take a fresh look at the effectiveness of evaluating merits based on an already achieved level of success and emphasizes the risks of spreading excessive honors or resources to people who, in the long run, might just be more successful than others. Using this model, we also consider and compare several behavioral hypotheses to show the most effective strategies for public research funding, with the goal of improving meritocracy, diversity, and innovation. This allows you to take a fresh look at the effectiveness of evaluating merits based on an already achieved level of success and emphasizes the risks of spreading excessive honors or resources to people who, in the long run, might just be more successful than others. Using this model, we also consider and compare several behavioral hypotheses to show the most effective strategies for public research funding, with the goal of improving meritocracy, diversity, and innovation. This allows you to take a fresh look at the effectiveness of evaluating merits based on an already achieved level of success and emphasizes the risks of spreading excessive honors or resources to people who, in the long run, might just be more successful than others. Using this model, we also consider and compare several behavioral hypotheses to show the most effective strategies for public research funding, with the goal of improving meritocracy, diversity, and innovation.

1. Introduction

The ubiquity of power dependence in many physical, biological, or socio-economic complex systems can be considered as something like a distinctive mathematical feature of the close relationship of their dynamic characteristics with a scale-unchanged topological structure [1, 2, 3, 4]. In the socio-economic context, according to the work of Pareto [5, 6, 7, 8, 9], it is well known that the distribution of wealth is in the form of a power dependence, whose characteristic strongly elongated shape reflects the depth of the existing abyss between the rich and poor of our society.

A recent report [10] shows that today this gap is much larger than we feared: eight people own the same wealth as 3.6 billion people, who make up the poorest part of humanity. Over the past 20 years, several theoretical models have been developed that calculate the distribution of values in the context of probability theory and physical statistics, often taking the form of multi-agent modeling with simple internal dynamics [11, 12, 13, 14, 15, 16, 17].

Moving further in this direction, if we consider personal wealth as a measure of success, it can be argued that the deeply asymmetric and unequal distribution among people is a consequence of their natural differences in talent, skills, competence, intelligence, abilities or the measure of their perseverance, hard work, or purposefulness. Such an assumption, in an implicit form, is the basis of the so-called meritocratic paradigm: it affects not only how our society provides employment opportunities, honor and fame, but also the strategies adopted by governments to allocate resources and finance to those who are considered the most honored personalities.

However, the previous conclusion seems to be very different from the confirmed data that the above-mentioned properties and qualities of people are normally distributed throughout the population, i.e., correspond to a symmetric Gaussian distribution relative to this average. For example, the intelligence, as measured by IQ tests, corresponds to the following pattern: the average IQ is 100, but no one has an IQ of 1000 or 10000. The same applies to work counted in working hours: someone works more than average, another fewer, but there is no one who works a billion times more hours than the rest.

But in our time there is more and more evidence regarding the fundamental role of chance, luck, or, in general, random factors, in determining success or failure in our personal and professional affairs. In particular, it was shown that all scientists have the same chance to publish breakthrough work during their careers [18]; that those with the first letter of the family name closer to the beginning of the alphabet are much more likely to receive the position of head of department [19]; that the distributions of bibliometric indicators collected by scientists may turn out to be random and meaningless due to the growing phenomenon associated with the “publish or die” inflationary mechanism [20]; that someone’s position in an alphabetically sorted list may be important in determining access to public services limited by the number of places [21]; that the initial letter of a middle name raises an assessment of intellectual abilities [22]; that people with easily pronounced names are rated more positively than those whose names are complex [23]; that those whose names sound more aristocratic more often than others work as leaders, and not subordinates [24]; that women with male nicknames are more successful in the legal profession [25]; that about half of the differences in income among people around the world is explained solely by their country of residence and the distribution of salaries within the respective country [26]; that the probability of becoming a director is greatly affected by your name and month of birth [27, 28, 29]; that innovative ideas are the result of random reactions in the cells of our brain [30]; and that even the likelihood of developing cancer, quite possibly destroying a great career, for the most part depends on failure [31, 32]. Recent works on the topic of reproductive success throughout life contribute to the confirmation of such statements, showing that if deviations of traits can affect the fate of the population as a whole, then the life of specific individuals is often determined by luck.

In recent years, many authors, including statistician and risk analyst Nassim Taleb [35, 36], investment strategist Michael Mobussin [37] and economist Robert Frank [38], have investigated in a number of popular books the connection between luck and skill in financial transactions, business, sports, art, music, literature, science and many other areas. They concluded that random events play a much greater role in life than many would have imagined. In fact, they do not assume that success does not depend on talent and efforts, since in extremely competitive areas or markets such as “the winner takes everything”, where we live and work at this time, the most productive people are almost always extraordinary talented and hardworking. They only concluded that talent and effort are not enough: You also need to be in the right place at the right time. In short, luck also affects, although its role is almost always underestimated by successful people. This is due to the fact that randomness often works in an unobvious way, so it is easy to compare events that show success as something that was inevitable. Taleb calls such an inclination “a fantastic fallacy” [36], and the sociologist Paul Lazarsfeld proposed the term “biased retrospective”. In his last book, “Everything Is Obvious: When You Know the Answer” [39], sociologist and pioneer of network science Duncan Watts suggests that both fabulous delusion and biased retrospective appeal to a special phenomenon in which people who see unusually successful results, consider them as an undoubted product of hard work and talent. However, success is mainly arises through complex and intertwined steps, each of which depends on the previous ones: if any of them were different, the whole career or life path would almost certainly also be different. This argument is also based on the results of an innovative experimental study conducted several years earlier by Watts himself in collaboration with other authors [40], in which the success of previously unknown songs in the artificial music market was not shown to correlate with the quality of the work itself. And this, of course, greatly complicates any predictions, as shown in another, more recent study [41]. This argument is also based on the results of an innovative experimental study conducted several years earlier by Watts himself in collaboration with other authors [40], in which the success of previously unknown songs in the artificial music market was not shown to correlate with the quality of the work itself. And this, of course, greatly complicates any predictions, as shown in another, more recent study [41]. This argument is also based on the results of an innovative experimental study conducted several years earlier by Watts himself in collaboration with other authors [40], in which the success of previously unknown songs in the artificial music market was not shown to correlate with the quality of the work itself. And this, of course, greatly complicates any predictions, as shown in another, more recent study [41].

In this paper, using an agent-based statistical approach, we will try to practically quantitatively determine the role of luck and talent in successful careers. In Section 2, on the basis of the minimum number of assumptions, namely, the Gaussian nature of the distribution of talent [42] and the multiplicative dynamics of both successes and failures [43], we present a simple model, which we called the “Talent vs. Luck” (TPU) model, in which imitates the development of professional careers of a group of people over the 40-year period of their work. The model shows that in reality, randomness plays a fundamental role in determining the most successful individuals. The true thing is that, as might be expected, talented people are more likely to become rich, famous or significant in their own lives, in relation to less prepared ones. But, and this is a less intuitive explanation, ordinary people with an ordinary level of talent are statistically destined to become successful (i.e., to be at the end of some power distribution of success) much more often than the most talented, provided that they become favorites of fortune throughout their lives . This fact is often encountered, as indicated in references [35, 36, 38], but, as far as we know, it was first modeled and measured in this work.

The success of people with ordinary talent calls into question the “meritocratic" paradigm and all those strategies and mechanisms that gave more rewards, opportunities, honor, fame and resources to people considered the best in their field [44, 45]. The fact is that, in the vast majority of cases, all assessments of someone’s talent were given ex-facto, solely by looking at his / her activity, or the results achieved, in a specific area of our society, such as sports, business, finance, art , science, etc. This type of misleading assessment leads to a substitution of cause and effect, evaluating as the most talented people those who are, simply, the most successful [46, 47]. In accordance with this view, previous works warned of similar types of “near meritocracy” and showed the effectiveness of other strategies based on random samples in many different environments, such as management, politics and finance [48, 49, 50, 51, 52, 53, 54, 55] . In Section 3, we take our approach and outline how the possible distribution schemes of public funds in the context of scientific research are compared. We study the consequences of various distribution strategies, among which there is a “near” meritocratic one, with the aim of exploring new ways to increase, at the same time, the minimum level of success of the most talented people in society and the total efficiency of government spending. We also examine, in general, how opportunities offered by the environment are presented in the form of levels of education and income (i.e., external factors, depending on the country and the social stratum from which people come) are important in increasing the likelihood of success. Final remarks complete the work.

2. Model

Further, we propose an agent model called “Talent against Luck” (TPU), based on a small number of assumptions, and aimed at describing the evolution of careers of a group of people under the influence of randomly occurring successful and unsuccessful events.

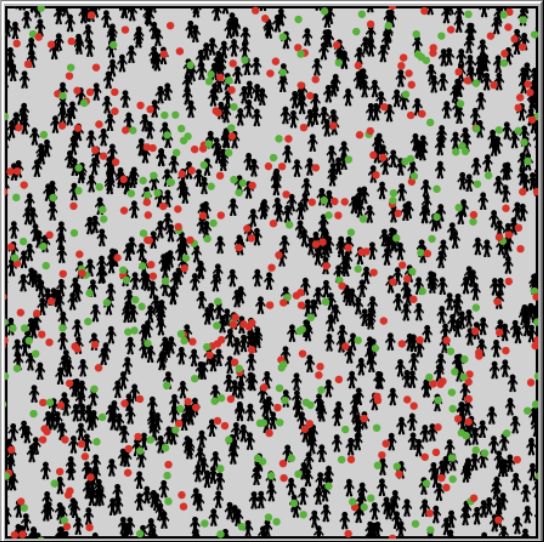

Figure 1: An example of the initial parameters for our simulation. All simulations presented in this work were carried out in the NetLogo agent simulation environment [56]. N = 1000 people (agents) with varying degrees of talent (intelligence, skills, etc.) randomly distributed over fixed positions within a square world of 201 × 201 sections with cyclic boundary conditions. During each simulation, which spans several decades, they are exposed to a certain amount of N Esuccessful (green circles) and unsuccessful (red circles) events moving around the world along random trajectories (random wandering). In this example, N E = 500.

We consider N individuals with T i talent (intelligence, skills, abilities, etc.) having a normal distribution in the interval [0; 1] around a given average m T with a standard deviation σ T randomly placed at fixed positions within the square world (see Figure 1) with cyclic boundary conditions (that is, with a toroidal topology) and surrounded by a certain number N E“Moving” events (marked with dots), some of which are successful, the other is not (neutral events are not taken into account in this model, since they have no significant consequences on the individual’s life). In Figure 1, we showed these events in the form of colored dots: successful in green and with a relative percentage p L , and unsuccessful in red and with a percentage ( 100 - p L ). The total number of event points N E is evenly distributed, but, of course, such a distribution will be ideally uniform only for N E → ∞ . In our simulations, there will usually be N E ≈ N / 2Therefore, at the beginning of each simulation, there is a random significant concentration of successful or unsuccessful event points in various regions of the world, while other regions will be more neutral. Subsequent random movement of points within a square matrix, i.e., the world, does not change this fundamental feature of the model, which indicates a different number of events of success or failure for different people throughout their lives, regardless of their personal talent.

Figure 2: normal distribution of talent among the population (with median m T = 0.6, shown by a dashed vertical line, and standard deviation σ T = 0.1 - values of m T ± σ Tdisplayed as two dotted vertical lines). This distribution is allocated in the interval [0; 1] and does not change during the simulation.

One simulation run examines a working life period P of 40 years (aged twenty to sixty years), with a time step δ t of six months. At the beginning of the simulation, all agents were given the same capital C i = C (0) Ɐ i = 1, ..., Nrepresenting their starting level of success / wealth. This choice has the obvious goal of not giving anyone the initial advantage. While agents' talents are not time-dependent, their capital is changing. During the development of this model, i.e., during the expected period of the agents' life, all event points randomly move around the world and, at the same time, may intersect with the location of some agents. If you go into details, each time each event point covers, in a random direction, the distance of 2 sections. We believe that there is an intersection with the individual if the event point represented inside the circle with a radius of one segment is centered on the agent (event points do not disappear after the intersection). Depending on such an incident, in this time stept (i.e., every six months), with a certain agent A k , the following three options are possible:

- No event point crosses the position of agent A k - this means that during the last six months no such events have occurred, agent A k does not perform any action.

- The position of agent A k is crossed by a successful event - this means that a successful event has occurred in the last six months (note, according to reference [30], the generation of innovative ideas here is also considered a successful event that happened in the agent’s brain); as a result, agent A k doubles his capital / success with a probability proportional to his talent T k . The increase will be C k (t) = 2C k (t - 1) , but only if rand [0; 1] <T k , that is, if the agent is smart enough to benefit from the luck that has come up.

- An unsuccessful event crosses the position of agent A k - this means that an unsuccessful event has occurred in the last six months; as a result, agent A k loses half of its capital / success, i.e. C k (t) = C k (t - 1) / 2 .

The above rules for agents (including the choice of dividing the initial capital in half in case of unsuccessful events and doubling in case of successful ones, in proportion to the talent of the agent) are intentionally simple and can be considered widespread, since they are based on the obvious fact that success in everyday life has the property both grow and decline at a rapid pace. Moreover, these rules give a significant advantage to highly talented people, since they can benefit more from the opportunities presented by luck (including the ability to use a good idea that originated in their brains). On the other hand, for example, a car accident or a sudden illness, are always unsuccessful events in which talent does not matter. In this regard, we can derive a more accurate definition of "talent", defining it as "any personal quality that increases the chance to seize the opportunity." In other words, by the term “talent” we, in a broad sense, mean intelligence, skills, resourcefulness, tenacity, determination, hard work, risk taking and so on. Further we will see that the advantage of having great talent is a necessary but not sufficient condition for achieving very high peaks of success.

2.1. Results of one run

In this subsection we presented the results of a run of one typical simulation. Generally speaking, these results are quite stable, therefore, as we show below, they can be considered to be largely representative of the general framework that leaves our model.

Let's imagine N = 1000 agents with an equal amount of seed capital C (0) = 10 (in abstract units) and with a fixed talent T i ϵ [0; 1], the following normal distribution with a median m T = 0.6 and a standard deviation σ T = 0.1 (see Figure 2). As mentioned earlier, the simulation covers a realistic time span P= 40 years, developing in equal steps, six months each, total of I = 80 iterations. In this simulation, we took N E = 500 event points, with the probability of successful events p L = 50%.

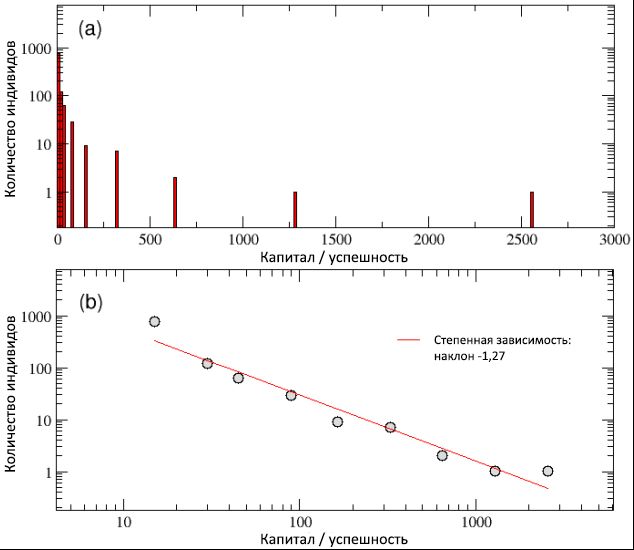

At the end of the simulation, as can be seen from diagram (a) of Figure 3, we found that simple dynamic model rules can produce an unequal distribution of capital / success, with a large number of poor (unsuccessful) agents and a small number of extremely rich (successful) ones. Having constructed the same distribution on a bilogarithmic scale, in scheme (b) of the same figure we see the distribution according to the power function in the Pareto style, the slope of which corresponds to the function y © ≈ C −1.27 .

Thus, despite the normal distribution of talent, the TPU model seemed to be able to capture the first important feature observed when compared with real data: the deepest gap between rich and poor and the invariable nature of its scale. In particular, in our simulation only 4 individuals received more than 500 units of capital, and the 20 most successful people own 44% of all values, while almost half of the population has less than 10 units. In general, the Pareto “80/20” rule is respected, since 80% of the population owns only 20% of the total capital, while the remaining 20% of individuals have 80% of the wealth. Although this inequality undoubtedly seems unfair, it would be somewhat acceptable if most successful people were among the most talented, thus deserving the accumulation of more capital / success compared to the rest. But is this really happening?

Figure 3: The final distribution of wealth / success among the population, on a logarithmic linear (a) and bilogarithmic (b) scale. Despite the normal distribution of talent, the tail of the success distribution, as can be seen from scheme (b), can be described as a power curve with a slope of −1.27. We have also confirmed that the distribution of capital / success follows the Pareto “80/20” law, since 20% of the population owns 80% of the values and vice versa.

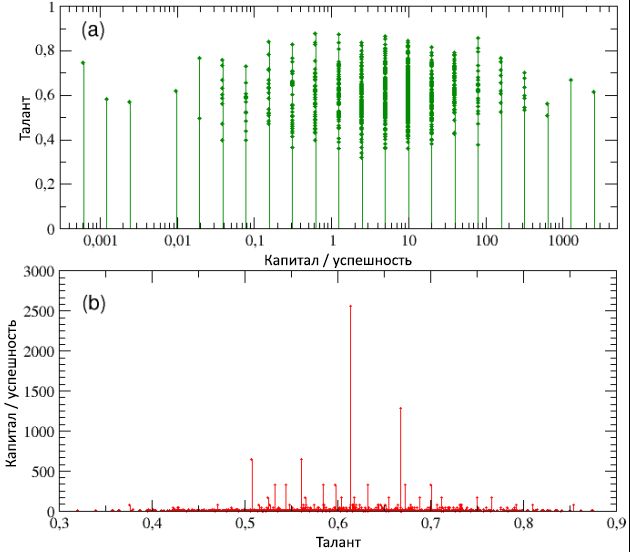

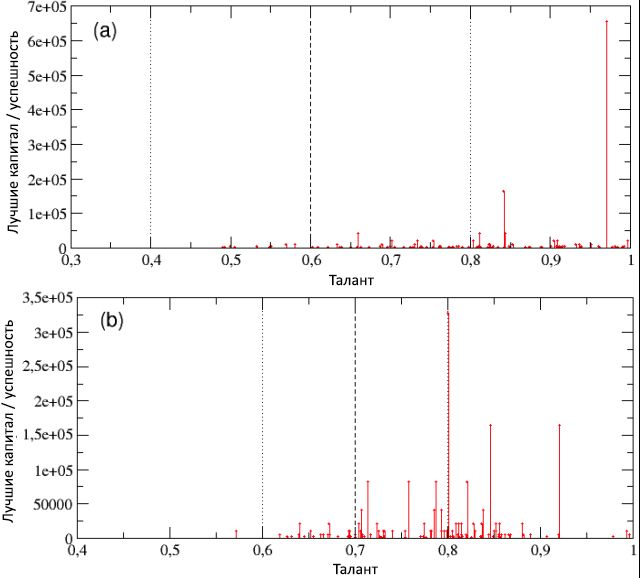

In Fig. 4, schemes (a) and (b), respectively, talent is displayed as a function of the total capital / success, and vice versa (note that in scheme (a) capital / success has only discrete values - this is connected with the decision use the same initial capital for all agents). A look at both schemes shows that, on the one hand, the most successful individuals are not the most talented and, conversely, the most gifted individuals are not the most successful. In particular, the most successful individual, with C max = 2560, has the talent T * = 0.61, which is only slightly higher than the median value m T = 0.6, while the most gifted ( T max= 0.89) has a capital / success rate of less than 1 unit ( C = 0.625).

As we learn in more detail from the next subsection, such a result is not a special case, but rather a rule for systems of this type: maximum success never converges with maximum talent, and vice versa. Moreover, this discrepancy between success and talent is disproportionate and highly non-linear. In fact, the average capital of all people with talent T> T * is C≈ 20; in other words, the capital / success of the most successful people with moderate talents is 128 times higher than the average capital / success of people who are much more gifted than the first ones. We can conclude that if exceptional talent is not hidden behind the reason for the tremendous success of some people, then, perhaps, there is another factor. Our simulation clearly shows that pure luck is such a factor.

Figure 4: in diagram (a), talent is displayed as a function of capital / success (on a logarithmic scale, for better clarity) - it indicates that the most successful individuals are not, at the same time, the most talented. In diagram (b), on the contrary, capital / success is shown as a function of talent - here you can better assess the fact that the most successful agent, with C max= 2560, has a talent that only slightly exceeds the median value m T = 0.6, while the most gifted one has a capital / success lower than C = 1 unit, much less than the initial capital C (0). Read on for more details.

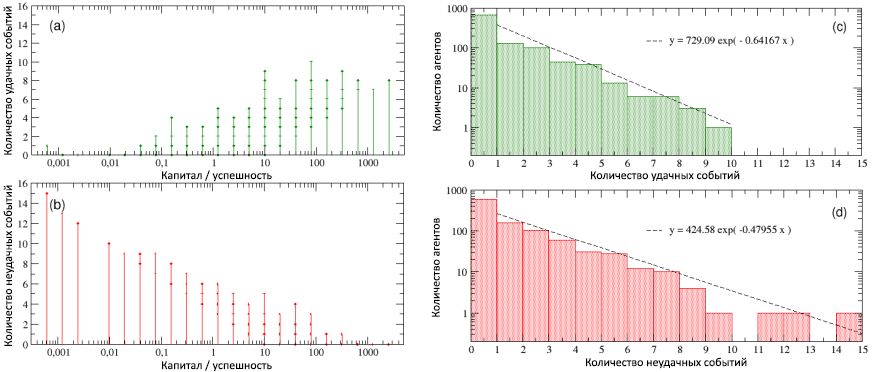

In Figure 5, the number of successful and unsuccessful events that occurred with all people during the period of their working life is shown as a function of their total capital / success. When considering scheme (a), it becomes obvious that the most successful individuals are at the same time the most successful (note that this diagram shows all the successful events that happened to the agents, and not just those from which they were able to benefit, in accordance with with your talent). On the contrary, when looking at scheme (b), we see that the most unsuccessful at the same time are the most unsuccessful. In other words, although there is no correlation between success and talent, based on simulations, there is a strong dependence of success on luck. Analyzing the details of the frequency distributions of the number of successful and unsuccessful events that occurred with individuals, we found

It is also interesting to look at the period of development of success / capital for both the most successful individuals and for the most unsuccessful, comparing with the corresponding sequences of successful and unsuccessful events that occurred during 40 years (80 intervals, 6 months each) of their working life. The results can be seen, respectively, in the left and right parts of Figure 6. In contrast to scheme (a) from image 5, the lower schemes of this figure contain only those successful events from which agents, thanks to their talent, were able to benefit.

Figure 5: total number of successful (a) and unsuccessful (b) events, as functions of capital / agent success. The graph shows a strong correlation between success and success: the most successful individuals are also the most successful, and vice versa. Again, due to the use of the same initial capital for all agents, it turns out that a number of events are grouped into discrete values of capital / success. In diagrams © and (d), the frequency of distributions, respectively, of the number of successful and unsuccessful events is displayed on a log-linear scale. As can be seen, both distributions can be written in the form of exponential dependencies with similar negative powers).

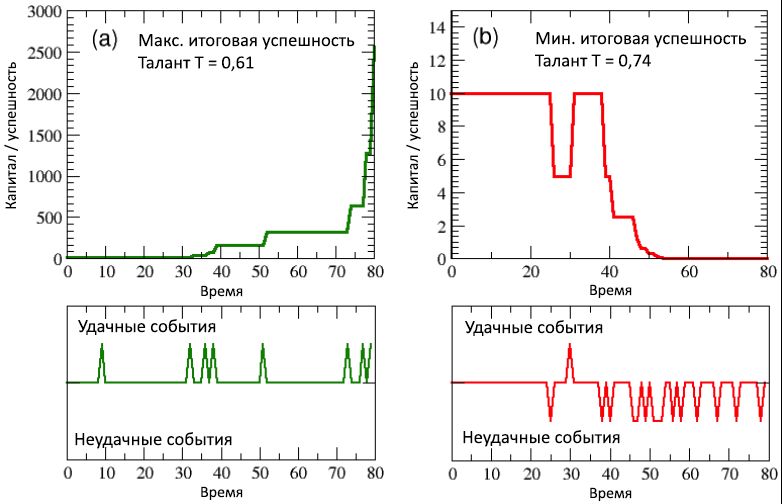

On the (upper and lower) diagrams (a) of Figure 6, concerning a moderately talented but most successful individual, it is clearly seen that after about half of his working life, accompanied by a rare manifestation of successful events (lower diagram), and a low level of capital (upper scheme), a sudden concentration of favorable events that occurred between 30 and 40 time steps (i.e., right before the agent’s 40th birthday) led to a rapid increase in capital, which in the last 10 steps (i.e., in the last 5 years of the agent’s career ) became exponential by going from C = 320 to C max = 2560.

On the other hand, looking at the (upper and lower) diagrams (b) of the same figure for the least successful individual, it becomes obvious that a particularly unsuccessful second half of his working life, accompanied by a dozen adverse events, constantly reduced capital / success, leading to the final value C = 0,00061. It is interesting to note that the talent of this unfortunate agent was T= 0.74, which is higher than most of the most successful. Obviously, creating the difference was influenced by luck. And if it is true that the most successful agent deserved to benefit from all the opportunities provided to him (despite his mediocre talent), it is also true that if your life is full of misfortunes and does not provide opportunities, like this second agent, then even the greatest talent becomes powerless against violent failure.

Figure 6: (a) the period of development of success / capital of the most successful individual and (b) the most unfortunate, compared according to the corresponding sequences of successful and unsuccessful events that occurred during their working life (out of 80 half-years, i.e., 40 years). The time of occurrence of such events is noted in the lower diagrams, in the form of ascending and descending peaks.

All the results of a single run (the demo version of the NetLogo code of the TPU model used for this simulation can be found in the Open ABM repository ) presented in this subsection are very stable and, as we will see from the next subsection, they are saved, with slight differences, with many repetitions of simulations starting with the same talent distribution, but with different random positions of individuals.

2.2. Multiple Run Results

In this subsection, we presented the general simulation results from, on average, more than 100 runs, each started with different, randomly selected, initial conditions. The values of the control parameters were the same as in the previous subsection: N = 1000 individuals, m T = 0.6 and σ T = 0.1 for the normal distribution of talent, I = 80 iterations (each represents δ t = 6 months of working life ), C (0) = 10 units of initial capital, N E = 500 event points and the percentage of successful events p L = 50%.

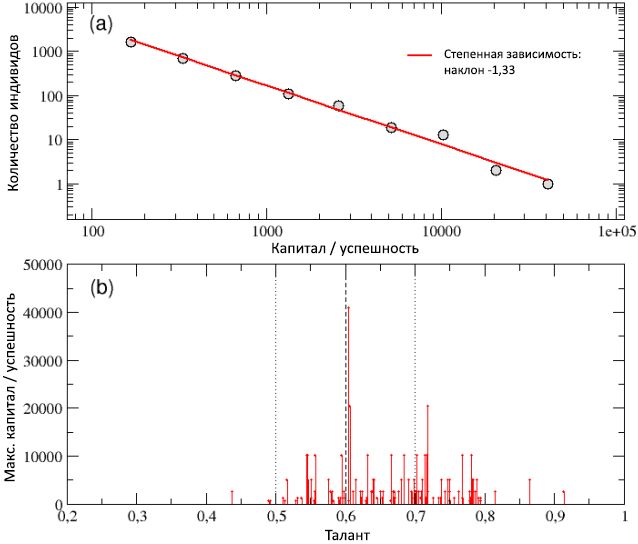

In diagram (a) of Figure 7, the total distribution of total capital / success among all agents collected as a result of 100 runs is shown on a logarithmic scale and is well described by a power curve with an angular coefficient of −1.33. The property of constant capital observed in a single run regardless of scale and the resulting high inequality among individuals, as well as the Pareto rule “80/20”, were thus preserved in the case of multiple runs. In fact, the gap between rich (successful) and poor (unsuccessful) agents has even widened, since the capital of the richest people now exceeds 40,000 units.

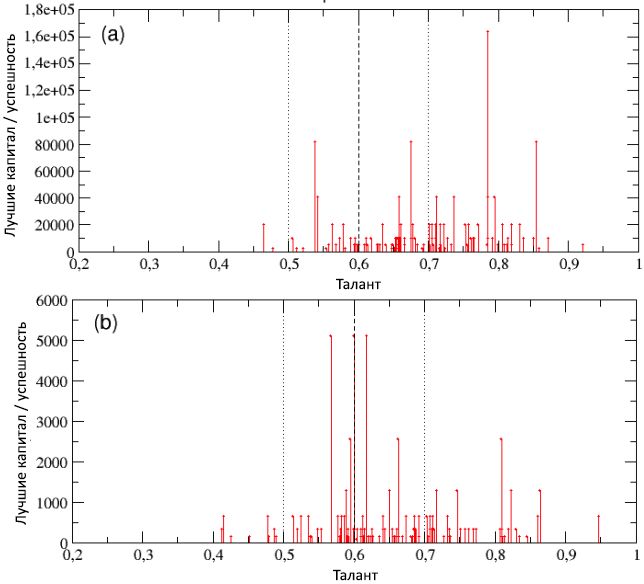

This result can be best estimated by looking at the scheme (b) of Figure 7, where the total capital C max is given as a function of talentonly the most successful individuals, i.e. showing the best result in each of the 100 runs. The agent with the talent T best = 0.6048, which almost coincides with the median of the distribution of talent ( m T = 0.6), which reached the peak capital C best = 40960, received the most points. On the other hand, the most gifted of the most successful individuals, with talent T max = 0.91, gained capital C max = 2560, which is only 6% of C best .

Figure 7: Scheme (a) - distribution of total capital / success calculated over 100 runs for populations with different randomly determined initial conditions. The distribution can be described by a power curve with a slope of −1.33. Scheme (b) - the total capital C max of the most successful individuals in each of the 100 runs, shown as a function of their talent. People with moderately high talent, on average, are more successful than those who have low or moderate low talent, and most often the most successful individual is a moderately gifted agent, and only occasionally the most talented one. The value of m T , as well as the values of m T ± σ Tare shown, respectively, in the form of vertical dashed and dotted lines.

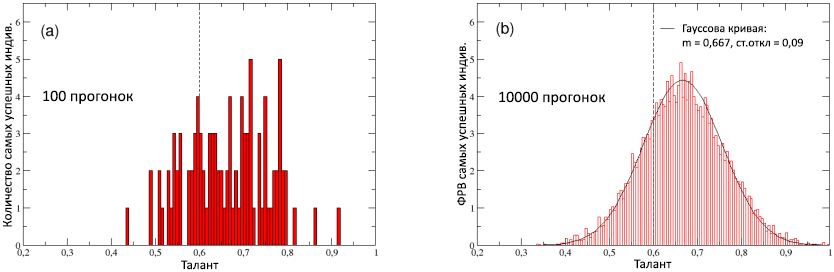

In order to examine this point of view in more detail, in Figure 8 (a) we plotted the talent distribution of the best performers, calculated for 100 runs. The distribution, obviously, is shifted to the right along the axis of the talent, with an average value of T av = 0.66> m T - this confirms, on the one hand, that to achieve significant success, a moderately high talent is often necessary; however, on the other hand, it also shows that this condition is almost never enough, since agents with the highest talent (i.e., with T > m T = 2σ T , or T> 0.8) are among the best performers in only 3% of cases, and their capital / success never exceeds 13% of C best .

Figure 8: (a) Talent distribution of the most successful personalities (best performers) in each of the 100 runs. (b) The probability distribution function (RFF) of the talent of the most successful individuals, calculated in 10,000 runs: is well described by the normal distribution with a median of 0.667 and a standard deviation of 0.09 (solid curve). For comparison, the median m T = 0.6 of the initial normal distribution of talent in the population is shown, shown in both schemes by a dashed vertical line.

In diagram (b) of Figure 8, the same distribution (reduced to the total area to obtain the FRF) is calculated for 10,000 runs, in order to understand its true shape: it looks like it fits into the Gaussian curve G (T) with an average T av = 0.667 and a standard deviation of 0.09 (solid line). This, of course, confirms that the distribution of talent of the best performers is shifted to the right relative to the axis of talent, compared with the initial distribution. To be more precise, this means that the conditional probability P ( C max | T ) = G (T) dT to find among the best performers a personality with talent in the interval [ T ; T + dT] grows with talent T , peaks near approximately moderate to medium talent T av = 0.66, and then drops sharply with large talent values. In other words, the probability of finding a moderately talented individual at the peak of success is higher than finding a highly gifted person there. Note that in an ideal world where talent is the main reason for its success, it is expected that P ( the C max | T ) is an increasing function of T . Thus, we can conclude that the observed Gaussian form P ( C max | T) is evidence of the greater importance of luck than talent in achieving extremely high levels of success.

Figure 9: change in time of success / capital of the most successful person (but, at the same time, moderately gifted), out of 100 simulation runs, compared with the corresponding unusual sequence of successful events that happened in her life.

It is also interesting to compare the average of 100 sweeps capital / success of the C mt ≈ 63 most talented people with the appropriate medium the C AT ≈ 33 those whose talent is close to the median of m T . In both cases, we found rather low indicators (albeit more than the initial capital C (0) = 10), but the fact that Cmt > C at , indicates that, although the probability of finding a moderately talented individual at the pinnacle of success is higher than that of a highly gifted individual, the most talented individuals of each run are, on average, more successful than moderately gifted people. On the other hand, looking at the average over 100 runs, the share of individuals with talent T > 0.7 (i.e., higher than with a standard deviation from the median) and the final success / capital C end > 10, calculated taking into account all agents with talent T> 0.7 (of which, on average for each run, ≈ 160), we found that this share is 32%, which means that the combined performance of the most talented people in our population is, on average, relatively small, since only a third of they reach the total capital in excess of the original.

In any case, the fact that the best performer among the 100 simulation runs is an agent with the talent T best = 0.6, which perfectly matches the median, and with the final success C best = 40960, which is 650 times more than C mt , is irrefutable . and more than 4,000 times higher than C end success<10 for 2/3 of the most talented people. This happened, in the end, simply because he was luckier than the rest. Unconditional lucky, as can be seen from Figure 9, which shows the growth of his capital / success over his working life, along with an impressive series of successful (and only successful) events, of which, despite the lack of exceptional talent, he was able to profit during his careers.

Summing up, at this point it was found that, despite its simplicity, the TPU model seems to be able to take into account many features that characterize, as was mentioned in the introduction, the high inequality in the distribution of wealth and success in our society, which clearly contrasts with the Gaussian distribution of talent among people. The model also quantitatively shows that great talent is not enough for a guaranteed successful career and that, on the contrary, less gifted people very often reach the pinnacle of success - this is another “conditional fact" often observed in real life [35, 36, 38].

A key aspect that intuitively explains how it can happen that moderately gifted individuals achieve (so often) much greater honor and success, compared to more talented ones, is that there is a hidden and often underestimated role of luck, as it is clearly seen from our simulations. But to understand the true meaning of the results of our research, it is important to distinguish between macro and micro point of view.

In fact, at the micro level, following the dynamic rules of the TPU model, a gifted individual is a priori more likely to achieve a high level of success than a moderately talented one, since he has a higher ability to seize the opportunity. Thus, from the point of view of an individual, we should conclude that, not being able (by definition) to influence the appearance of successful events, the best strategy to increase the likelihood of success (at any level of talent) is to expand personal activity, generate ideas, communicate with other people, the search for diversity and mutual enrichment. In other words, becoming a broad-minded person who is ready to contact others gives the highest probability of a successful event (which will be realized to the best of the personality’s talent).

On the other hand, at the macro level, from the point of view of the whole society, the likelihood of meeting moderately gifted individuals at the summits of success is much higher than finding extremely talented people there, because the former are much larger and, thanks to luck, they have, in general, statistical the advantage of achieving tremendous success, despite their own a priori lower personal likelihood.

In the next section, we will consider this macro-level point of view, exploring the opportunities offered by our model in order to study in more detail more effective strategies and policies to improve the average level of performance of the most talented people in the population, implementing more productive ways of distributing rewards and resources. In fact, we expect that any policy that can increase the level of the most talented individuals who are the engine of progress and innovation in our society will have a cumulative beneficial effect.

3. Effective luck balancing strategies

The results presented in the previous section are clearly consistent with the empirical evidence documented in the introduction, which calls into question the meritocratic assumption, which states that natural differences in talent, skills, abilities, intelligence, hard work, or perseverance are the only reasons for success. As we have shown, luck also has an impact and can play a crucial role. The essence of the discussion is that, due to the difficult measurability (in many cases, it is difficult to determine in exact terms) of personal qualities, meritocratic strategies are often used to distribute honoring, financing or awards, often based on private results, measured in terms of personal wealth or success. As a result

Let's imagine, for example, a government-funded research and development council with a fixed amount of money at its disposal. What will be much more effective for increasing the average research effectiveness: to give large grants to only a few undoubtedly excellent scientists or small grants to many obviously more ordinary scientists? A recent study [44], based on an analysis of four indices of the scientific significance of related publications, found that significance has only a weak positive relationship with funding. In particular, the significance of the dollar was lower for large grant holders, and the significance of scientists who received increases in funding did not increase to an appropriate degree. The authors of the study concluded that the scientific significance (as reflected in the publication) only weakly borders on financing, and it was suggested that financing strategies aimed at diversifying ideas rather than “excellence” are likely to be more productive. A later contribution [60] showed that, both in the number of documents produced and in their scientific importance, concentrated research funding usually leads to decreasing marginal returns, and also that the most funded researchers do not stand out in terms of effectiveness and scientific significance. In general, such conclusions should not be surprising in the light of another recent discovery [18], which states that significance, as measured by influential publications, is randomly distributed throughout the scientist’s series of publications. In other words, luck matters and if it affects more than we want to admit, it is not surprising that meritocratic strategies are less effective than expected, especially if we are trying to appreciate the merit of the posteriori. In previous studies [48, 49, 50, 51, 52, 53, 54, 55] there was already a warning against this kind of “near meritocracy,” showing the effectiveness of alternative strategies based on random elections in the areas of management, politics and finance. According to this point of view, the TPU model shows how the minimum level of success can be increased for most talented people in the world where luck matters and accidental discovery often leads to important achievements. if we try to appreciate the merit of a posteriori. In previous studies [48, 49, 50, 51, 52, 53, 54, 55] there was already a warning against this kind of “near meritocracy,” showing the effectiveness of alternative strategies based on random elections in the areas of management, politics and finance. According to this point of view, the TPU model shows how the minimum level of success can be increased for most talented people in the world where luck matters and accidental discovery often leads to important achievements. if we try to appreciate the merit of a posteriori. In previous studies [48, 49, 50, 51, 52, 53, 54, 55] there was already a warning against this kind of “near meritocracy,” showing the effectiveness of alternative strategies based on random elections in the areas of management, politics and finance. According to this point of view, the TPU model shows how the minimum level of success can be increased for most talented people in the world where luck matters and accidental discovery often leads to important achievements.

3.1. Accidental discovery, innovation and effective financing strategies

The term “random discovery” is widely used in literary references to historical facts, showing that researchers quite often make unexpected and useful discoveries by pure chance, when they are looking for something else [61, 62]. There is a long list of stories of discoveries made exclusively by coincidence: from penicillin by Alexander Fleming to radioactivity by Marie Curie, from cosmic microwave background radiation by radio astronomers Arno Penzias and Robert Woodrow Wilson to graphene Andrei Geim and Konstantin Novoselov. Here is a more recent example: a network of channels filled with liquid in the human body, a previously unknown organ that apparently promotes the spread of cancer cells, was discovered by chance during simple endoscopy [63]. Therefore, many believe

Is it possible to quantify the significance of random discovery? What are the most effective ways to simulate random discovery? It can take many different forms and is difficult to limit and quantify. That is why, until now, academic studies have considered an accidental scientific discovery, for the most part, as a philosophical concept. But times are changing. The European Research Council recently allocated a $ 1.7 million grant to biochemist Ohid Yakubu to calculate the significance of an accidental discovery in science [65]. Yakub found that random discovery can be classified into four basic types [66] and that there may be important factors that influence its appearance. His conclusions, apparently, coincide with the ideas developed in earlier studies [67, 68, 69, 70, 71, 72], which argue that generally accepted, clearly meritocratic, strategies that pursue superiority and supplant diversity seem destined to be losing and ineffective. The reason is that they a priori reject research that initially looked less promising, but which, thanks, in particular, to a random discovery, could a posteriori be incredibly innovative.

From this point of view, we want to apply the TPU model, which naturally expresses luck (and, consequently, random discovery) as a quantitative parameter of the strategy, in order to study the effectiveness of various financing scenarios in this subsection. In particular, in situations where, as mentioned above, a moderately-talented-but-lucky person is often more successful than more-gifted-but-unlucky individuals, it is important to evaluate the effectiveness of financing strategies for the ability to maintain a minimum level of success, including for the most talented people who are expected to bring in the most innovative and progressive ideas.

Starting with the same initial parameters that were used in subsection 2.2, i.e. N = 1000, m T = 0.6,σ T = 0.1, I = 80, δ t = 6, C (0) = 10, NE = 500, p L = 50% and 100 simulation runs, let's imagine that the available total funding capital F T is periodically distributed among an individual according to various criteria. For example, finances may be issued:

- Equally shared (egalitarian criteria) to encourage research diversity;

- Only a certain percentage of the most successful (“best”) individuals (elitist criterion), which was previously called the “near” meritocracy, for the distribution of finances among people based on past performance.

- "Premium" distribution among a certain proportion of the most successful individuals, and the remainder, in small equal parts, over the rest (mixed criterion);

- Only a certain percentage of individuals randomly selected (selective random criterion).

We realistically assume that the total capital F T will be allocated every 5 years, during the 40-year period of each simulation run, so that F T = 8 units of capital will be distributed from time to time . With the help of periodic injections of these finances, we intend to maintain a minimum level of resources of the most talented agents. Thus, a good indicator of the effectiveness of the chosen financing strategy can be the percentage P T , average for 100 simulation runs, for individuals with talent T > m T + σ T , whose total success / capital exceeds the initial level, i.e., C end> C (0).

This percentage has already been calculated during the simulation runs presented in section 2.2. It shows that in the absence of funding, the best performance was achieved by the most successful agents with close to average talent, while the capital / success of the most talented people always remains extremely low. In particular, only a part of P T0 ≈ 32% of the total number of agents with talent T > 0.7 was able to achieve, based on the simulation results, capital / success exceeding the initial value. Therefore, to compare the effectiveness of different financing strategies, the growth of the average percentage P T relative to P T0 should be calculatedthose talented people who have increased their initial capital during their careers. Let's define this growth as P * T = P T - P T0 . This value is a fairly stable indicator: we checked it by repeating from 100 simulations, the spread of P * T values remained below 2%. Finally, if we calculate the ratio of P * T to the total capital distributed over all agents over 40 years, we can get an efficiency index E , which measures the growth in the number of sufficiently successful talented people per unit of invested capital, defined as E = P * T/ The F T .

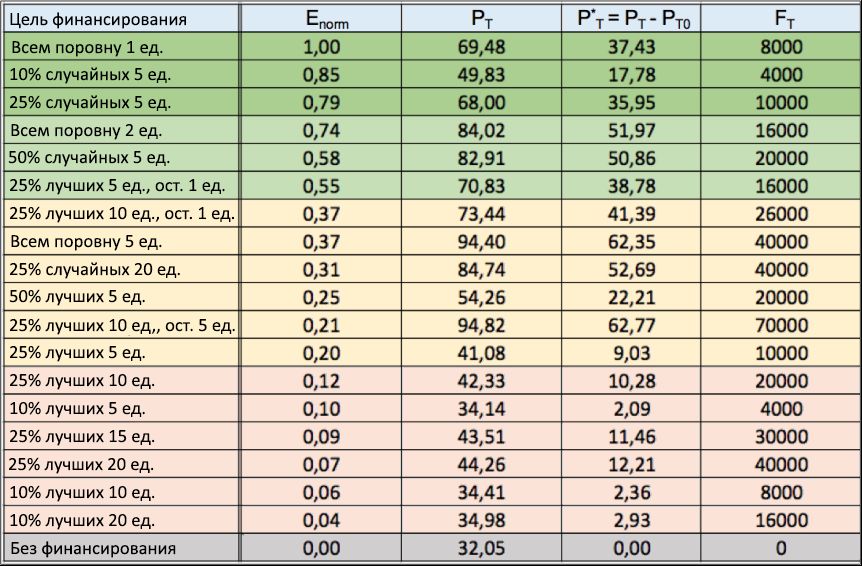

Figure 10: table of financing strategies. Several strategies for distributing finances for various purposes (1 column) are presented, with the results of the normalized efficiency index E norm (2 columns), in descending order. Also, in the third and fourth columns, respectively, the values of the share P T of successful talented people and the net increase in their number P * T are shown , relative to the “no financing” scenario, on average for 100 simulation runs. Finally, the last column shows the total capital F T invested in each run.

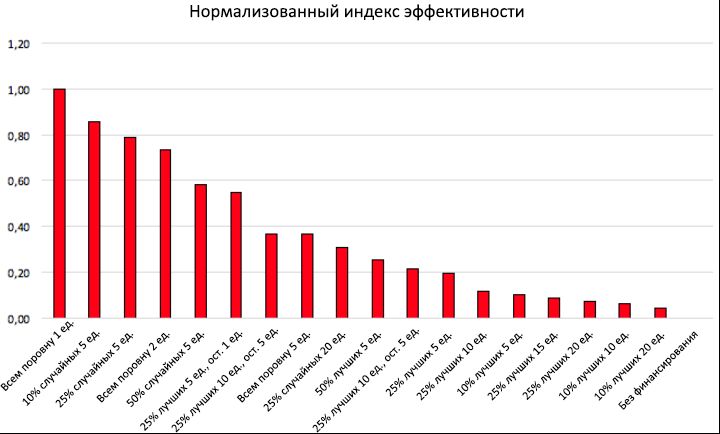

In the table in Figure 10, we showed the performance index (2nd column) obtained for several financing distribution strategies, each with its own financial purpose (1 column), as well as the corresponding values of P T (3rd column) and P * T (4th column). In the same column, in the last column, the total invested capital F T for each run is given . The efficiency index E was normalized relative to its maximum value E max , and all records (rows) are ordered by the criterion of decreasing values of E norm = E / E max. For a scenario with a lack of funding, by definition, E norm = 0. The same results of E norm are shown as a function of the adopted financing strategies in the form of a histogram in Figure 11. Due to the statistical stability P T showing deviations of less than 2%, the results of the efficiency index E norm are stable.

When considering the above table and the corresponding histogram from Figure 11, it becomes obvious that if the goal is to reward the most talented individuals (thereby increasing their final level of success), it is much better to periodically allocate (even a small) amount of capital to all individuals at once, rather than giving out more capital to only a small part of them, selected according to the level of success achieved by the time of distribution.

Figure 11: Normalized Performance Index of some financing strategies. Values of the normalized efficiency index E norm are given as a function of various financing strategies. The figure shows that, to increase the success of more talented people with C end> C (0), it is much more efficient to distribute small amounts of finance among many individuals than to finance with other, more selective ways.

On the one hand, the histogram shows that the “egalitarian” criterion, which allocates 1 unit of capital to each individual every 5 years, is the most efficient way to distribute finances, with E norm = 1 (i.e., E = E max ): for relatively small investments F T in the amount of 8000 units, it turns out to double the percentage of successful talented people, compared with the scenario "without financing", leading it from P T0 = 32.05% to P T= 69.48%, with a net increase of P * T = 37.43. When considering increasing the total invested capital (for example, by setting an equalization quota of 2 or 5 units), this strategy also provides a further increase in the final percentage of successful talented people (from 69.48% to 94.40%), but normalized efficiency at this gradually decreases, from E norm = 1 to E norm = 0.74, and then to E norm = 0.37, respectively.

On the other hand, “elite” strategies that distribute every 5 years for a large amount of finances (5, 10, 15 or 20 units) only among the best 50%, 25% or even 10% of successful individuals are located at the very bottom of the table, withE norm <0.25 in all these scenarios, the net growth P * T of the total number of successful talented people, compared with the “without financing” scenario, remains extremely low (in almost all cases less than 20%), often despite a much larger investment capital, when compared with a similar egalitarian strategy. These results reinforce the assumption that such an approach is obviously not far meritocratic.

It is worth noting that the adoption of the "mixed" criterion, i.e. the distribution of the “meritocratic” financial part among a certain percentage of the most successful individuals, for example, 25%, with the distribution of the remaining finances in equal shares to other people, gives better results of the performance index compared to the “not far meritocratic” approach. However, in terms of productivity, this strategy is not able to catch up with the “egalitarian” criterion. As this is clearly seen, for example, from a comparison of the sixth and fourth rows of the financing table: despite the same total investment of 16,000 units, the P T value obtained with the mixed criteria remains much lower than with the leveling approach (70.83% against 84, 02%), which is also confirmed by the corresponding values of the efficiency index Enorm (0.55 vs 0.74).

If we take into account psychological factors (not modeled in this study), then the mixed strategy can be reconsidered in comparison with the egalitarian one. In fact, the bonus reward assigned to the most successful individuals can stimulate greater adherence among all agents, while the equally distributed remaining part will play a double role: on an individual level, it will stimulate diversity and provide new opportunities for unsuccessful talented people to realize their potential, and at the general level will support random discoveries, thereby contributing to the development of research and the community as a whole.

Looking again at the table of financing strategies, it is worth paying attention to the incredibly high efficiency of random strategies, which occupy two of the three best positions in the overall result. It follows that, for example, a periodic reward of 5 units of only 10% of randomly selected individuals, with a total investment of only 4,000 units, gives a net increase of P * T = 17.78%, which is higher than almost all obtained using equalization strategies. Moreover, increasing to 25% the share of randomly funded people and doubling the total investment (raising them to 10,000 units) gives a net growth of P * T= 35.95, comparable to that obtained by the best equalizing strategy, which won first place in the overall standings. It is striking that this last P * T result is about four times the value ( P * T= 9.03%) obtained with the elitist approach (see row 12 of the table), which distributed exactly the same capital (10,000 units) among the same number of individuals (25% of the total). The latter confirms even more that in complex social and economic environments where chance plays a significant role, the effectiveness of other strategies based on random elections can easily bypass standard strategies based on the “near meritocratic” approach. This phenomenon, contrary to common sense, has already been observed in the areas of management, politics and finance [48, 49, 50, 51, 52, 53, 54, 55], and thus finds another confirmation in the context of the study of financing.

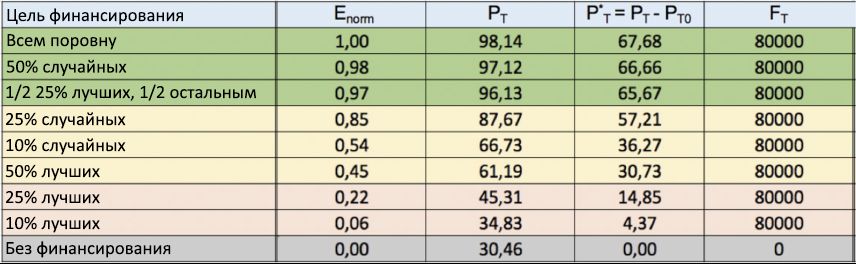

In order to further confirm the data obtained, Fig. 12 shows the results of another series of simulations. Unlike previous simulations, here the total amount of capital invested in each of 100 runs is now fixed at F T = 80,000, so that F T / 8 = 10,000 units are distributed among agents every 5 years , according to the same financing strategies discussed earlier . Looking at the table, we see that the results of the egalitarian strategy were again the most effective in terms of rewarding the most talented people, with a share of P Tclose to 100%. This is followed by a random strategy (with 50% of individuals randomly selected for financing), and then mixed, in which half of the capital is distributed among 25% of the most successful individuals, and the other part, in equal shares, among other people. On the contrary, all elite strategies were again located at the end of the rating, thereby further confirming the inefficiency of the “not far meritocratic” approach in rewarding true talent.

Figure 12: Table of fixed finance financing strategies. The obtained normalized efficiency indices E norm for several strategies for financing distribution (1st column) are again shown in descending order, from top to bottom. In contrast to Figure 10, here the total capital invested in each run is fixed atF T = 80000. The equalization strategy again took first place.

The results of simulations of the TPU model presented in this subsection drew attention to the significance of external factors (as, indeed, effective financing policies) in increasing the chances of success for most talented individuals who too often find themselves punished by the coincidence of unsuccessful events. In the next subsection, we examine the extent to which new opportunities should come from changes in the environment, for example, such as the level of education or other incentives derived from the social environment in which people live or where people come from.

3.2. Significance of the environment

To begin with, let us assess the role of the average level of education among the population. Within the framework of the TPU model, it can be obtained by changing the parameters of the normal talent distribution. In general, if we assume that the talent and skills of individuals, when stimulated, can be more effective in realizing new opportunities, then increasing either the median m T or the standard deviation of talent σ T can be interpreted as a consequence of policies aimed, respectively, either at raising the average level of education, or to strengthen the training of the most gifted people.

In the two diagrams of Figure 13, we presented the total capital / success accumulated by the best performers of each of the 100 runs in the form of a function of their talent. The given parameters correspond to those used in subsection 2.2 ( N = 1000, I = 80, δ t = 6, C (0) = 10, N E = 500 and p L = 50%), but with different moments of talent distribution . In particular, in scheme (a) we left unchanged m T = 0.6, but increased σ T = 0.2, while in scheme (b) we did the opposite, leaving σ T = 0.1 and raising m T= 0.7. In both cases, you can notice a shift to the right of the peaks of maximum success, but with a difference in details.

Figure 13: the total capital of the most successful individuals in each of the 100 runs, presented as a function of their talent for populations with different talent distribution parameters: (a) m T = 0.6 and σ T = 0.2 (which reflects the strengthening of the training training the most gifted people); (b) m T = 0.7 and σ T = 0.1 (which depicts an increase in the average level of education). The corresponding values of m T and m T ± σ T are also shown., in the form of vertical broken lines and dotted lines, respectively.

In fact, this leads to the fact that an increase in σ T , at a constant value of m T , as shown in diagram (a), increases the chances of the most talented people to achieve very high success - the best performer is now a very gifted agent, with T = 0, 97, which achieved an incredible level of capital / success C best = 655360. This, on the one hand, can be evaluated positively, however, on the other hand, it is an isolated case and also, as a counterbalance, there is a widening gap between unlucky and lucky people. Now looking at the scheme (b) we see that the increase in m Twithout changing σ, T gives the best performer with C best = 327680 and talent T = 0.8, followed by two more, with C = 163840 and, accordingly, T = 0.85 and T = 0.92. This suggests that in this case the chances of the most talented people to achieve extremely high success increased, but at the same time, the gap between unsuccessful and lucky people was lower than before.

Finally, in both examples considered, the average value of capital / success of the most talented of 100 runs of people increased in relation to the value of C mt ≈ 63 obtained in Subsection 2.2. In particular, we got Cmt ≈ 319 in scheme (a) and C mt ≈ 122 in scheme (b), but these results are very specific for a particular series of simulation runs. A more reliable parameter for numerical expression of the effectiveness of the social policies studied here is that it is again the indicator P T presented in the previous subsection, i.e. average share of individuals with talent T > m T + σ T and total success / capital C end > 10, relative to the total number of people with talent T > m T + σ T (note that here, in both cases, mT + σ T = 0.8). So, we got P T = 38% in scheme (a) and P T = 37.5% for scheme (b), with a slight net increase in relation to the reference value P T0 = 32% (obtained for talent distribution at m T = 0.6 and σ T = 0.1).

Summing up, our results show that strengthening the training of the most gifted people or raising the average level of education leads, as might be expected, to some positive effects in the social system, since both of these policies lead to an increase in the likelihood of talented individuals to realize opportunities, provided by their luck. On the other hand, improvements in the average share of highly talented people who managed to achieve a good level of success do not seem to be particularly significant for both of the scenarios analyzed. Thus, the outcome of the respective educational policies seems to be largely limited to the occurrence of isolated cases of exceptional success.

Of course, once this level of education was established, it became obvious that the abundance of opportunities offered by that social environment, i.e. the country where someone was accidentally born or decided to live is another key component that can influence the global performance of the system.

In Figure 14 we presented results similar to those that were visible in the previous image, but for another series of simulations, with 100 runs each, with the same set parameters as in subsection 2.2 ( N = 1000, m T = 0, 6, σ T = 0.1, I = 80, C (0) = 10, N E = 500) but with different percentages p Lsuccessful events (recall that in subsection 2.2 the percentage p L = 50% was taken ). In scheme (a), we take p L = 80% to simulate a highly stimulating environment full of opportunities, typical of rich industrialized countries like the USA [26]. On the other hand, in scheme (b), the value p L = 20% reproduces the scenario of a much less encouraging environment, with an extremely small number of possibilities, such as, for example, in the countries of the Third World.

Figure 14: the total capital of the most successful individuals in each of the 100 runs is shown as a function of their talent for populations living in environments with different percentages p L of successful events: (a) p L= 80%; (b) p L = 20%. Also, vertical dashed and dotted lines indicate, respectively, the values of m T = 0.6 and m T ± σ T , with σ T = 0.1.

As seen in both schemes, the final success / capital most fortunate individuals shown as a function of their talent, are highly dependent on p L .

At p L = 80%, as in scheme (a), several agents with medium-high talent were able to achieve higher levels of success compared to the scenario p L = 50%, with the peak C best= 163840. On the other hand, the average value of capital / success of the most talented individuals, C mt ≈ 149, is quite high and, more importantly, the same applies to the indicator P T = 62.18% (which is approximately twice the reference values of P T0 = 32%), this means that, as expected, the most talented people benefit from a larger percentage of successful events.

Completely different results were obtained at p L = 20%. Of course, as can be seen from scheme (b), the overall level of success is now very low, compared to what was found in the simulations from subsection 2.2, with a peak value of C bestamounting to only 5120 units - this is a trace of lowering social inequalities, which is the expected consequence of equalizing opportunities in achieving success. In accordance with these results, the indicator P T also reaches its minimum value, with an average percentage of talented individuals who managed to increase their initial level of success, equal to only 8.75%.

As a result, in this section it was shown that the encouraging environment and the abundance of opportunities associated with the appropriate strategy for the distribution of finances and resources are important factors in realizing the potential of the most talented people, giving them more chances to achieve success compared to moderately gifted, but more lucky. From the macro point of view, any policy that can influence these indicators and support talented individuals will result in collective progress and innovation.

4. Final remarks

In this paper, starting with a number of extremely simple and rational assumptions, we presented an agent model that was able to quantitatively measure the role of talent and luck in the success of people's careers. The simulations showed that although the talent has a Gaussian distribution among agents, the final distribution of success / capital, after 40 years of working life, follows a power function according to the principle of the 80/20 Pareto law, which corresponds to the nature of the distribution of wealth observed in the real world. An important result of the simulations is that the most successful agents are almost always not the most talented, but those who are close to the average value of the Gaussian distribution of talent - a widely known fact that is often found in the literature. The model shows the often underestimated importance of successful events in determining the final level of individual success. Since rewards and resources are usually distributed to those who have already achieved a high level of success, mistakenly used as a measure of competence / talent, this leads to negative incentives, which causes a lack of opportunities for the highest talents. Our results emphasize the risks of a paradigm that we call “near meritocracy,” which is unable to respect and reward the most competent people, since it underestimates the role of chance among the main determining success factors. In this regard, several different scenarios were studied in order to identify the most effective strategies that could balance the unpredictable role of luck and give more opportunities and resources to the most talented ones - the intention, which should be the main goal of a truly meritocratic approach. It was also shown that these strategies are most beneficial for the community as a whole, as they lead to the growth of various ideas and perspectives in research, thereby also stimulating innovation.

Acknowledgments

We want to thank Robert Frank, Pavel Sobkowitz and Konstantino Tsallis for fruitful discussions and comments.

Bibliography

- Bak, P., Tang, C. and Wiesenfeld, K., Self-organized criticality. Phys. Rev. A , 38: 364 {374 (1988).

- Barab´asi, A.-L., Albert, R., Emergence of Scaling in Random Networks, Science , Vol. 286, Issue 5439, pp. 509 {512 (1999).

- Newman, MEJ, Power laws, Pareto distributions and Zipf's law, Contemporary Physics , 46 (5): 323 {351 (2005).

- Tsallis, C., Introduction to Nonextensive Statistical Mechanics. Approaching a Complex World , Springer (2009).

- Pareto, V., Cours d'Economique Politique , vol. 2 (1897).

- Steindl, J., Random Processes and the Growth of Firms — A Study of the Pareto Law, Charles Griffin and Company, London (1965).

- Atkinson, A. B., Harrison, A. J., Distribution of Total Wealth in Britain, Cambridge University Press, Cambridge (1978).

- Persky, J., Retrospectives: Pareto’s law, Journal of Economic Perspectives 6, 181{192 (1992).

- Klass, O. S., Biham, O., Levy, M., Malcai, O., Solomon, S., The Forbes 400 and the Pareto wealth distribution, Economics Letters 90, 290{295 (2006).

- Hardoon, D., An economy for the 99%, Oxfam GB, Oxfam House, John Smith Drive, Cowley, Oxford, OX4 2JY, UK (January 2017).

- Bouchaud, J.-P., M´ezard, M., Wealth condensation in a simple model of economy, Physica A 282, 536{54 (2000).

- Dragulescu, A. and Yakovenko, V. M., Statistical mechanics of money, Eur. Phys. J. B 17, 723{729 (2000).

- Chakraborti, A. and Chakrabarti, B. K., Statistical mechanics of money: how saving propensity affects its distribution, Eur. Phys. J. B 17, 167{170 (2000).

- Patriarca, M., Chakraborti, A., Germano, G., Influence of saving propensity on the power law tail of wealth distribution, Physica A 369(2), 723{736 (2006).

- Scalas, E., Random exchange models and the distribution of wealth. European Physical Journal — Special Topics, 225. pp. 3293-3298. ISSN 1951{6355 (2016).

- During, B., Georgiou, N. and Scalas, E., A stylised model for wealth distribution. In Akura, Yuji and Kirman, Alan (eds.) Economic Foundations of Social Complexity Science. Springer Singapore, Singapore, pp. 95{117. ISBN 9789811057045 (2017).

- During, Bertram, Georgiou, Nicos and Scalas, Enrico (2017) A stylised model for wealth distribution. In: Akura, Yuji and Kirman, Alan (eds.) Economic Foundations of Social Complexity Science. Springer Singapore, Singapore, pp. 95-117. ISBN 9789811057045

- Sinatra, R., Wang, D., Deville, P., Song, C. and Barab´asi, A.-L., Quantifying the evolution of individual scientific impact, Science 354, 6312 (2016).

- Einav, L. and Yariv, L., What’s in a Surname? The Effects of Surname Initials on Academic Success, Journal of Economic Perspective, Vol. 20, n. 1, p.175{188 (2006).

- Ruocco, G., Daraio, C., Folli, V. and Leonetti, M., Bibliometric indicators: the origin of their log-normal distribution and why they are not a reliable proxy for an individual scholar’s talent, Palgrave Communications 3:17064 doi: 10.1057/palcomms.2017.64 (2017).

- Jurajda, S., Munich, D., Admission to Selective Schools, Alphabetically, Economics of Education Review, Vol. 29, n. 6, p.1100{1109 (2010).

- Van Tilburg, W. A. P., Igou, E. R., The impact of middle names: Middle name initials enhance evaluations of intellectual performance, European Journal of Social Psychology, Vol. 44, Issue 4, p.400{411 (2014).

- Laham, S. M., Koval, P., Alter, A. L., The name-pronunciation effect: Why people like Mr. Smith more than Mr. Colquhoun, Journal of Experimental Social Psychology 48, p.752{756 (2012).

- Silberzahn, R., Uhlmann, E. L., It Pays to be Herr Kaiser: Germans with Noble-Sounding Last Names More Often Work as Managers, Psychological Science 24(12): 2437{44 (2013).

- Coffey, B. and McLaughlin, P., From Lawyer to Judge: Advancement, Sex, and NameCalling. SSRN Electronic Journal, DOI10.2139/ssrn.1348280 (2009).

- Milanovic, B., Global Inequality of Opportunity: How Much of Our Income Is Determined by Where We Live?, Review of Economics and Statistics, 97.2 (2015): 452{60.

- Du, Q., Gao, H., Levi, M. D., The relative-age effect and career success: Evidence from corporate CEOs, Economics Letters 117(3):660{662 (2012).

- Deaner, R. O., Lowen, A., Cobley, S., Born at the Wrong Time: Selection Bias in the NHL Draft. PLoS ONE 8(2): e57753 (2013).

- Brooks, D., The Social Animal. The Hidden Sources of Love, Character, and Achievement, Random House, 424 pp. (2011).

- Iacopini, I., Milojevic, S. and Latora, V., Network Dynamics of Innovation Processes, Physical Review Letters 120, 048301 (2018).

- Tomasetti, C., Li, L., Vogelstein, B., Stem cell divisions, somatic mutations, cancer etiology, and cancer prevention, Science 355, 1330{1334 (2017).

- Newgreen, D. F. et al., Differential Clonal Expansion in an Invading Cell Population: Clonal Advantage or Dumb Luck?, Cells Tissues Organs 203:105{113 (2017).

- Snyder, R. E. and Ellner, S. P., We Happy Few: Using Structured Population Models to Identify the Decisive Events in the Lives of Exceptional Individuals, The American Naturalist 188, no. 2 (2016): E28{E45.

- Snyder, R. E. and Ellner, S. P., Pluck or Luck: Does Trait Variation or Chance Drive Variation in Lifetime Reproductive Success?, The American Naturalist 191, no. 4 (2018): E90{E107.

- Талеб Н.Н., Одураченные случайностью. О скрытой роли шанса в бизнесе и в жизни, Манн, Иванов и Фербер (2018).

- Талеб Н.Н., Черный лебедь. Под знаком непредсказуемости, КоЛибри (2018).

- Mauboussin, M. J., The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing, Harvard Business Review Press (2012).

- Фрэнк Р.Х., Успех и удача. Фактор везения и миф меритократии, Высшая Школа Экономики (2019).

- Watts, D. J., Everything Is Obvious: Once You Know the Answer, Crown Business (2011).

- Salganik, M. J., Dodds P. S., Watts D. J., Experimental Study of Inequality and Unpredictability in an Artificial Cultural Market, Science Vol.311 (2006)

- Travis, M., Hofman, J. M., Sharma, A., Anderson,. A., Watts, D. J., Exploring limits to prediction in complex social systems, Proceedings of the 25th ACM International World Wide Web Conference (2016) arXiv:1602.01013 [cs.SI]

- Stewart, J., The Distribution of Talent, Marilyn Zurmuehlin Working Papers in Art Education 2: 21-22 (1983).

- Sinha, S. and Pan, R. K., How a «Hit» is Born: The Emergence of Popularity from the Dynamics of Collective Choice, In Econophysics and Sociophysics: Trends and Perspectives (eds B. K. Chakrabarti, A. Chakraborti and A. Chatterjee), Wiley-VCH Verlag GmbH & Co. KGaA, Weinheim, Germany. doi: 10.1002/9783527610006.ch15 (2006).

- Fortin, J.-M., Curr, D. J., Big Science vs. Little Science: How Scientific Impact Scales with Funding, PLoS ONE 8(6): e65263 (2013).

- Jacob, B. A., Lefgren, L., The impact of research grant funding on scientific productivity, Journal of Public Economics 95 (2011) 1168{1177.

- O’Boyle, JR. E. and Aguinis, H., The Best and the Rest: revisiting the norm of normality of individual performance, Personnel Psychology, 65: 79-119. doi:10.1111/j.1744-6570.2011.01239.x (2012).

- Denrell, J. and Liu, C., Top performers are not the most impressive when extreme performance indicates unreliability, Proceedings of the National Academy of Sciences, 109(24):9331{9336 (2012).

- Pluchino, A., Rapisarda, A., and Garofalo, C., The Peter principle revisited: A computational study, Physica A 389(3):467{472 (2010).

- Pluchino, A., Garofalo, C., Rapisarda, A., Spagano, S. and Caserta, M., Accidental politicians: How randomly selected legislators can improve parliament efficiency, Physica A 390(21):3944{3954 (2011).

- Pluchino, A., Rapisarda, A. and Garofalo, C., Efficient promotion strategies in hierarchical organizations, Physica A 390(20):3496{3511 (2011).

- Biondo, A. E., Pluchino, A., Rapisarda, A., Helbing, D., Reducing financial avalanches by random investments, Phys. Rev. E 88(6):062814 (2013).

- Biondo, A. E., Pluchino, A., Rapisarda, A., Helbing, D., Are random trading strategies more successful than technical ones, PLoS One 8(7):e68344 (2013)

- Biondo, A. E., Pluchino, A., Rapisarda, A., The beneficial role of random strategies in social and financial systems, J. Stat. Phys. 151(3-4):607{622 (2013).

- Biondo, A. E., Pluchino, A., Rapisarda, A., Micro and macro benefits of random investments in financial markets, Cont. Phys. 55(4):318{334 (2014).

- Biondo, A. E., Pluchino, A., Rapisarda, A., Modeling financial markets by self-organized criticality, Phys. Rev. E 92(4):042814 (2015).

- Wilensky, U., NetLogo. ccl.northwestern.edu/netlogo. Center for Connected Learning and Computer-Based Modeling, Northwestern University, Evanston, IL (1999).

- Merton, R. K., The Matthew effect in science, Science 159, 56-63 (1968).

- Мертон Р. К., Эффект Матфея в науке, II: Накопление преимуществ и символизм интеллектуальной собственности, https://www.hse.ru/data/033/314/1234/3_6_1Merto.pdf.

- Bol, T., de Vaan, M. and van de Rijt, A., The Matthew effect in science funding, Proceedings of the National Academy of Sciences, DOI: 10.1073/pnas.1719557115 (2018).

- Mongeon, P., Brodeur, C., Beaudry, C. et al., Concentration of research funding leads to decreasing marginal returns, Research Evaluation 25, 396{404 (2016).

- Merton, R. K., Barber, E., The Travels and Adventures of Serendipity, Princeton University Press, Princeton (2004).

- Murayama, K. et al., Management of science, serendipity, and research performance, Research Policy 44 (4), 862{873 (2015).

- Benias, P. C. et al., Structure and Distribution of an Unrecognized Interstitium in Human Tissues, Scientific Reports, vol. 8, 4947 (2018).

- Flexner, A, The Usefulness of Useless Knowledge, Princeton University Press, Princeton (2017).

- Lucky science. Scientists often herald the role of serendipity in research. A project in Britain aims to test the popular idea with evidence., Nature Editorial, Vol.554, 1 February 2018.

- Yaqub, O., Serendipity: Towards a taxonomy and a theory, Research Policy 47, 169{179 (2018).

- Page, S. E., The Diversity Bonus. How Great Teams Pay Off in the Knowledge Economy, Princeton University Press (2017).

- Cimini, G., Gabrielli, A., Sylos Labini, F., The Scientific Competitiveness of Nations, PLoS ONE 9(12): e113470. doi.org/10.1371/journal.pone.0113470 (2014).

- Curry, S., Let’s move beyond the rhetoric: it’s time to change how we judge research, Nature 554, 147 (2018).

- Nicholson, JM and Ioannidis, JPA, Research grants: Conform and be funded, Nature 492, 34 {36 (2012).

- Bollen, J., Crandall, D., Junk, D. et al., An efficient system to fund science: from proposal review to peer-to-peer distributions, Scientometrics 110, 521 {528 (2017).

- Garner, HR, McIver, LJ and Waitzkin, MB, Research funding: Same work, twice the money ?, Nature 493,599 {601 (2013).

Source: Talent vs Luck: the role of randomness in success and failure