How to get the most out of your investment portfolio?

The fool said: “Do not put all your eggs in one basket!” - in other words: spray your interests and money! And the sage said: “Put all your eggs in one basket, but ... take care of the basket!” This phrase belongs to Mark Twain, but you probably heard its “wise” part from Warren Buffett. Yes, the legendary investor is not a supporter of asset allocation and invests exclusively in American stocks.

Is such an approach justified and is portfolio diversification as they say it useful? Let's check. To do this, we take the ETF funds most popular for investment and see how effective they are when combined into a portfolio. And at the same time, we will find out whether the number of funds in the portfolio affects its performance.

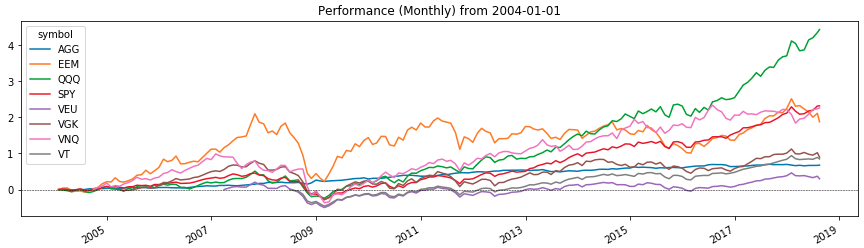

The chart above shows the profitability of the ETF funds with which we will work, from January 2004 to August 2018. It is during this period that we will test portfolios. And below is a description of what they consist of. (Pay attention to the date the funds appeared (ETF launch column) - we will need it in the future.)

Now we will form portfolios of the aggressive model from the funds listed above (we want to squeeze the most out of portfolio investment). This model assumes the predominance of shares in the portfolio, in our case it will consist of 80% of the shares and 20% of US bonds (as the most risk-free asset). By structure, portfolios will differ in the number of assets and the depth of diversification. There will be six in total:

In parentheses are the shares of assets in accordance with their order in the name. So, the portfolio of SPY, AGG (80/20) consists of 80% of S&P 500 shares and 20% of US investment rating bonds. Now that our portfolios are ready, let's test them with Python. We will test, as already mentioned, for the period from January 2004 to August 2018. However, you probably noticed that not all of the ETFs we examined were on the market in 2004. Therefore, in the tests we will do so. Those funds that were not yet traded at the start of testing will be added to the portfolio as they appear on the market.

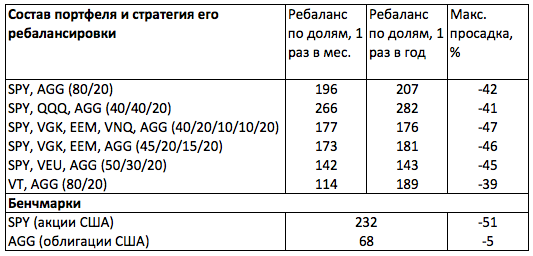

The table below shows the test results. The Benchmarks section shows the yield and maximum drawdown for the period for stocks (SPY) and bonds (AGG). By their values, we can easily understand what to expect from stocks and bonds as an aggressive and defensive asset class. (However, we always (!) Must remember that past results do not guarantee future ones).

As you can see, over the period of broad market shares (SPY) gave a cumulative return of 232% with a maximum drawdown of 51%. That is, if we had been holding a portfolio of S&P 500 shares only since 2004, we would have increased our investments by 3.3 times, but at some point half of the invested funds could not be counted (these are the risks of the stock market). But if we added 20% of the bonds to it, we would soften the blow a bit and reduce the drawdown by 20% (42% vs 51%), but paying 15.5% of the yield (196% vs 232%) for this.

At the same time, if we, along with bonds, added shares of the fund on the Nasdaq 100 to the portfolio, we would have received the same 41% drawdown, but with a higher yield (266% or 282%, depending on the frequency of rebalancing). And this means that with this portfolio we would have overtaken the wide market (SPY) and sank less during the crisis. But if we diversified our portfolio into different countries, we would have significantly worsened its return (173% or 181% - depending on the frequency of rebalancing and lower) and ensured an average drawdown of 46%. Adding to the portfolio of the US Real Estate Fund (VNQ) would slightly improve its profitability, but increase the drawdown.

Test results lead us to the following conclusions.

It turns out that Buffett is right in putting all his eggs in one basket. And if we want to get the most out of our portfolio, we must bet on the American market. Is it worth worrying that an 80% portfolio of US stocks is not diversified? I don't think it's worth it. At least because the S&P 500 includes securities of companies operating around the world. That is, this index is diversified by default. And whether we need additional diversification by country is a big question. I suggest you think about this issue (and write what you think in the comments below). And we are moving from the most profitable portfolio model to the most effective way of managing it.

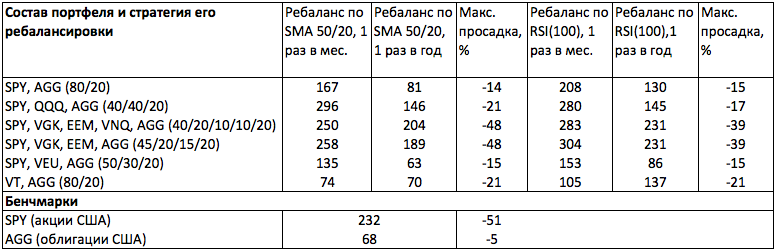

When analyzing the effectiveness of the portfolio structure, we relied on the results of classical management. That is, those that we would receive by rebalancing the portfolio once a year in shares. Let's now look at the results of an alternative rebalancing of indicators. The essence of this rebalancing is to check the daily charts of portfolio assets for one of the following conditions (depending on the chosen strategy): 1) The RSI (100) is above 50. 2) The moving average SMA (50) is above the SMA (200).

In the first case, we buy and hold an asset in the portfolio only when its RSI (100) value is above 50. In the second case, when the SMA (50) is on the SMA (200). If these conditions are not met, the asset is not taken into the portfolio. If the asset is already in the portfolio, then it is sold, and the money received is distributed among other assets.

What gives us this approach? As can be seen from the table, a decrease in portfolio drawdown and profitability growth. At the same time, we would get the maximum effect from the monthly rebalancing of the portfolio (annual balancing is not suitable here) according to RSI (100). So, for the simplest portfolio of SPY, AGG (80/20), we would have a yield of 9% lower than SPY (208% versus 232%), and the drawdown is 3.4 (!) Less (51% versus 15%). Moreover, due to rebalancing according to RSI (100), we would be able to get an increase in EEM in the portfolio diversified by countries (SPY, VGK, EEM, AGG) in 2007-2009, and thereby overtake SPY by 30% (304% against 232%).

The results of the tests lead us to the idea that portfolio management is more important than its model. They also make you think about applying elements of technical analysis in portfolio investment in order to maximize profits and reduce risk. Whether to combine passive investment with active management is up to you. But it is obvious that just such a synthesis allows you to get more from standard portfolios.

Is such an approach justified and is portfolio diversification as they say it useful? Let's check. To do this, we take the ETF funds most popular for investment and see how effective they are when combined into a portfolio. And at the same time, we will find out whether the number of funds in the portfolio affects its performance.

The chart above shows the profitability of the ETF funds with which we will work, from January 2004 to August 2018. It is during this period that we will test portfolios. And below is a description of what they consist of. (Pay attention to the date the funds appeared (ETF launch column) - we will need it in the future.)

We make portfolios

Now we will form portfolios of the aggressive model from the funds listed above (we want to squeeze the most out of portfolio investment). This model assumes the predominance of shares in the portfolio, in our case it will consist of 80% of the shares and 20% of US bonds (as the most risk-free asset). By structure, portfolios will differ in the number of assets and the depth of diversification. There will be six in total:

- SPY, AGG (80/20).

- SPY, QQQ, AGG (40/40/20).

- SPY, VGK, EEM, VNQ, AGG (40/20/10/10/10/20).

- SPY, VGK, EEM, AGG (45/20/15/20).

- SPY, VEU, AGG (50/30/20).

- VT, AGG (80/20).

In parentheses are the shares of assets in accordance with their order in the name. So, the portfolio of SPY, AGG (80/20) consists of 80% of S&P 500 shares and 20% of US investment rating bonds. Now that our portfolios are ready, let's test them with Python. We will test, as already mentioned, for the period from January 2004 to August 2018. However, you probably noticed that not all of the ETFs we examined were on the market in 2004. Therefore, in the tests we will do so. Those funds that were not yet traded at the start of testing will be added to the portfolio as they appear on the market.

Testing portfolios

The table below shows the test results. The Benchmarks section shows the yield and maximum drawdown for the period for stocks (SPY) and bonds (AGG). By their values, we can easily understand what to expect from stocks and bonds as an aggressive and defensive asset class. (However, we always (!) Must remember that past results do not guarantee future ones).

As you can see, over the period of broad market shares (SPY) gave a cumulative return of 232% with a maximum drawdown of 51%. That is, if we had been holding a portfolio of S&P 500 shares only since 2004, we would have increased our investments by 3.3 times, but at some point half of the invested funds could not be counted (these are the risks of the stock market). But if we added 20% of the bonds to it, we would soften the blow a bit and reduce the drawdown by 20% (42% vs 51%), but paying 15.5% of the yield (196% vs 232%) for this.

At the same time, if we, along with bonds, added shares of the fund on the Nasdaq 100 to the portfolio, we would have received the same 41% drawdown, but with a higher yield (266% or 282%, depending on the frequency of rebalancing). And this means that with this portfolio we would have overtaken the wide market (SPY) and sank less during the crisis. But if we diversified our portfolio into different countries, we would have significantly worsened its return (173% or 181% - depending on the frequency of rebalancing and lower) and ensured an average drawdown of 46%. Adding to the portfolio of the US Real Estate Fund (VNQ) would slightly improve its profitability, but increase the drawdown.

Was Buffett right?

Test results lead us to the following conclusions.

- Portfolio diversification by country would not increase the profitability of our portfolio.

- Adding an additional asset class (US Real Estate Fund, VNQ) to our portfolio would also not give us advantages.

- The greatest return and least drawdown would be brought to us by a portfolio focused on US stocks, especially innovative companies (QQQ).

It turns out that Buffett is right in putting all his eggs in one basket. And if we want to get the most out of our portfolio, we must bet on the American market. Is it worth worrying that an 80% portfolio of US stocks is not diversified? I don't think it's worth it. At least because the S&P 500 includes securities of companies operating around the world. That is, this index is diversified by default. And whether we need additional diversification by country is a big question. I suggest you think about this issue (and write what you think in the comments below). And we are moving from the most profitable portfolio model to the most effective way of managing it.

Choosing a portfolio management model

When analyzing the effectiveness of the portfolio structure, we relied on the results of classical management. That is, those that we would receive by rebalancing the portfolio once a year in shares. Let's now look at the results of an alternative rebalancing of indicators. The essence of this rebalancing is to check the daily charts of portfolio assets for one of the following conditions (depending on the chosen strategy): 1) The RSI (100) is above 50. 2) The moving average SMA (50) is above the SMA (200).

In the first case, we buy and hold an asset in the portfolio only when its RSI (100) value is above 50. In the second case, when the SMA (50) is on the SMA (200). If these conditions are not met, the asset is not taken into the portfolio. If the asset is already in the portfolio, then it is sold, and the money received is distributed among other assets.

What gives us this approach? As can be seen from the table, a decrease in portfolio drawdown and profitability growth. At the same time, we would get the maximum effect from the monthly rebalancing of the portfolio (annual balancing is not suitable here) according to RSI (100). So, for the simplest portfolio of SPY, AGG (80/20), we would have a yield of 9% lower than SPY (208% versus 232%), and the drawdown is 3.4 (!) Less (51% versus 15%). Moreover, due to rebalancing according to RSI (100), we would be able to get an increase in EEM in the portfolio diversified by countries (SPY, VGK, EEM, AGG) in 2007-2009, and thereby overtake SPY by 30% (304% against 232%).

Is portfolio management more important than its model?

The results of the tests lead us to the idea that portfolio management is more important than its model. They also make you think about applying elements of technical analysis in portfolio investment in order to maximize profits and reduce risk. Whether to combine passive investment with active management is up to you. But it is obvious that just such a synthesis allows you to get more from standard portfolios.