Bank in your pocket: 9 trends in mobile payments and banking

In this article, we have collected key insights from the annual report of Global Mobile Money of the international organization Mobile Ecosystem Forum. After reading to the end, you will find out what retailers are doing to popularize contactless payments in advanced economies, what revolutionary solutions are being introduced by payment service providers in the markets of developing countries, and of course, key trends in the field of M-commerce, including: the future mobile payments in offline stores, messenger applications as a new sales channel, specifics of multi-screen sales, and much more.

In this article, we have collected key insights from the annual report of Global Mobile Money of the international organization Mobile Ecosystem Forum. After reading to the end, you will find out what retailers are doing to popularize contactless payments in advanced economies, what revolutionary solutions are being introduced by payment service providers in the markets of developing countries, and of course, key trends in the field of M-commerce, including: the future mobile payments in offline stores, messenger applications as a new sales channel, specifics of multi-screen sales, and much more.The report contains a survey of 15,000 mobile device users from 15 countries. The main topic of the report was the steady growth in the popularity of mobile banking and mobile commerce. 69% of mobile device users use online banking, 66% make certain types of transactions. It is worth noting that the popularity of "mobile money" varies markedly from country to country.

According to MEF, in the broad sense, “mobile payments” can mean activities such as payment using a mobile device in the store, online payments on sites, money transfers from account to account (P2P), purchase of digital content, payment for services online at the point of provision, payments using mobile wallets.

The study also shows that contactless payments in offline stores still occupy a minimal share in the volume of mobile commerce. With the launch of Samsung Pay, Android Pay and Apple Pay, which recently announced its plans for large-scale expansion, there is no doubt that the situation will change soon.

New Technologies and NFC Growth

Developed markets today are characterized by high penetration of mobile devices and developed infrastructure. This allows us to develop and complicate the formats for using “mobile money”, both between individuals and between consumers and financial institutions. An example of such latest technologies are NFC sensors in smartphones, which allow paying in offline stores using a mobile device as a contactless bank card.

Convenience and Speed - Key Driversfor most developed markets, although there is no universal payment solution that would suit any user for solving any problems. For example, payment tools that allow you to pay for digital content that does not have physical media (the so-called carrier billing) are the most suitable solution for those who do not have bank cards, as well as a convenient way to make purchases in mobile applications.

Speaking about NFC technology, one cannot fail to note how retailers use mobile payments together with other important elements of e-commerce - loyalty, special offers and rewardsso as not to lose their position in the market. For example, the Starbucks mobile app processes more than eight million transactions per week and has about 16 million registered users. With each purchase made using the application, points are credited to the client's account, which can be exchanged for drinks and other bonuses. This increases loyalty of regular customers and attracts new brand supporters.

Mobile Champions - Africa and Asia

In markets where mobile payments lead, the picture is dramatically different. In dozens of countries in Africa and Asia, services such as Mpesa and Fundamo (providers of payment services and microfinance for mobile operator subscribers) unleashed a mobile revolution. Although the majority of the population of these countries have not yet started using banking services, they actively use phones with advanced functionality to access mobile money services and pay for physical goods, bills, money transfers or access to digital goods and services.

The use of mobile payment services as the main way of making transactions in these countries allowed them to “overtake” even developed economies. The growing popularity of smartphones in these countries has created additional opportunities for the development of mobile payments. For example, 80% of respondents in Indonesia, 85% of respondents in Nigeria, and 93% of respondents in Kenya confirmed that they are active users of mobile banking.

It should be noted that such a dominance of mobile money slows down the development of the banking system and retail in several regions of Asia and Africa.

Having understood the many possibilities of using mobile payments, MEF chose nine key trends and driverswho currently set the tone for the entire M-commerce industry and will greatly influence it in the future.

I. Payments using smartphones in offline stores, so insignificant today, have great prospects in the future.

12% of users have made at least one contactless payment over the past six months:

- 4% using NFC technology;

- 7% through a mobile POS terminal at a point of sale;

- 5% made payments with a mobile loyalty card (Starbucks, etc.).

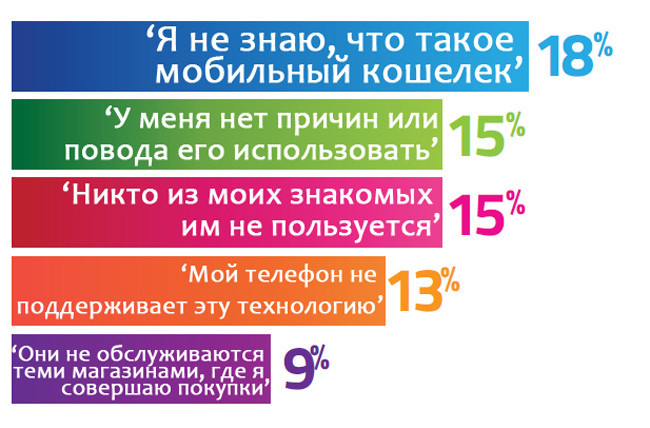

II. Consumers still don’t know why they need mobile electronic wallets.

The study reflects the bewilderment of society and, as a result, indifference to mobile wallets. 18% do not know what it is, 15% do not see the point in it, and just as much that none of their friends use them.

III. Social networks are the future of e-commerce.

The impact of social networks on the use of mobile devices cannot be overestimated. 24% of mobile phone users and 15% of smartphone owners actively use social networks in the process of online shopping.

IV. Distrust of users prevents mobile payments.

34% of consumers put safety first among their concerns. 11% “do not trust the security of mobile payments”, 9% are afraid to provide too much personal information, 8% say that mobile systems are completely unprotected, and 6% do not trust electronic trading enterprises at all.

V. Mobile applications - a new opportunity for shopping.

56% of respondents prefer to make purchases through the application, rather than through a mobile site. Since consumers spend most of their time in messenger applications, some experts suggest that in the future they may become the new online sales channel. Some of these services already have a financial transaction function. Messaging applications such as Line in the Asia-Pacific region allow users to connect a bank card to the messenger and make money transfers to friends, as well as purchases in some stores.

VI. The “second screen” is the path to the heart of the buyer.

94% use two or more “screens” in the process of surfing the Internet, most of which (42%), for example, watch TV. In addition, 32% use the “second screen” to search for additional information about the purchase. More information about the specifics of multi-screen sales is in the analytical material “ Multi-screen world. Cross-platform shopping . ”

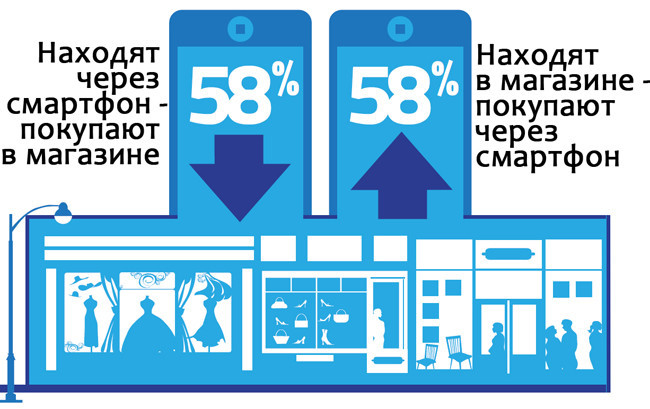

VII. From online to offline - and vice versa.

58% of users at least once found goods online via a smartphone, and then purchased them in an offline store. About the same number of respondents, on the contrary, get acquainted with the range of offline, then to place an order on the Internet. The PayOnline press center wrote about this trend back in 2013 .

Viii. The place of the bank is in your pocket.

69% of mobile users interact with their bank account through their mobile device. The most popular feature is checking the bank balance. At the same time, the popularity of more complex financial transactions is growing: 18% transfer money from one account to another, 16% transfer money to friends, 9% apply for a loan.

IX. In the first place - simplicity and convenience.

Mobile payments attract 32% of users at high speed shopping. Payment providers understand the need of users for speed and convenience - and strive to make the services as friendly as possible.

One of the most interesting solutions is fingerprint identification. For many, this is the best opportunity to make a payment in one action. Apple devices already support this option to pay for iTunes - and this is just the beginning.

In the summer of 2014, the TouchID API became available, which allowed developers to implement this technology in their applications. At the moment, this function is more used to unlock the phone than to make payments. However, with the advent of Apple Pay, the rapid growth in the popularity of authentication through biometric data is perhaps inevitable.

So in the Mobile Ecosystem Forum see the future of M-commerce. The material has been prepared for publication by the authors of the electronic payment system PayOnline .