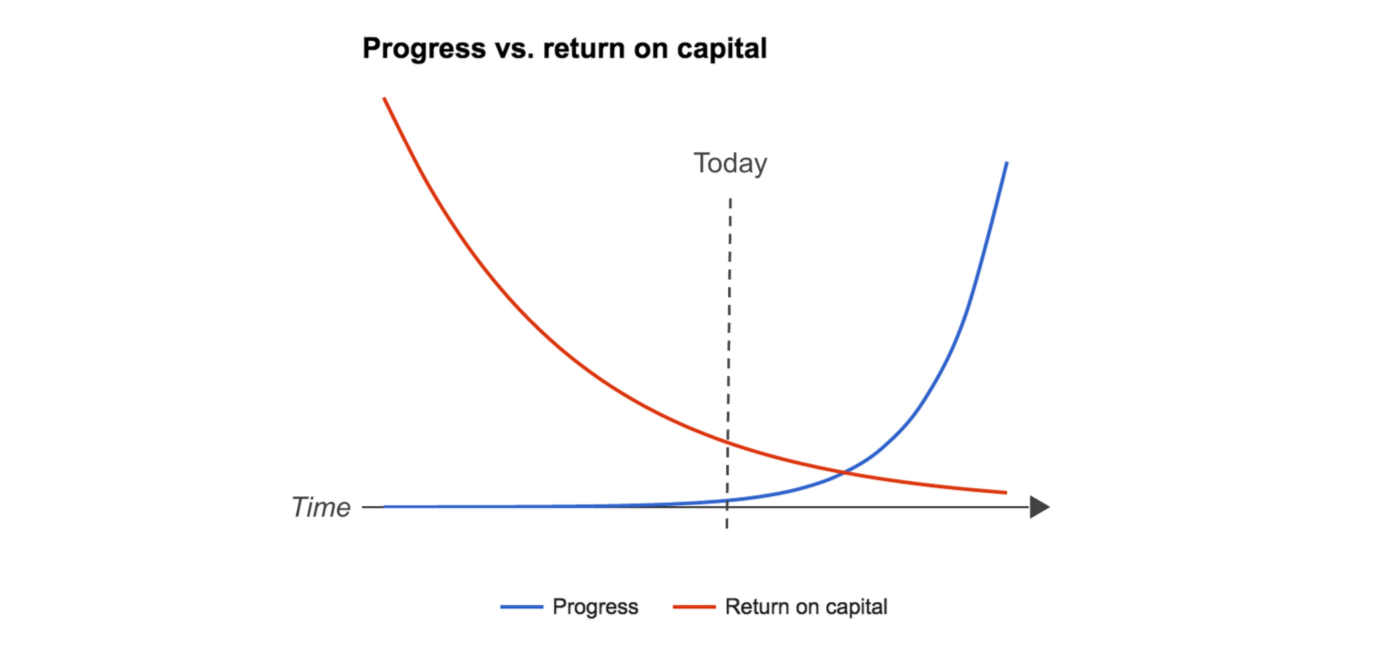

There are no more interest rates

- Transfer

Entrepreneurs and techies love to dream about the future: how self-driving cars will change transportation, how logistics will be destroyed by drones, how bitcoins will supplant sovereign currencies.

But, distracting from technology: what will happen to financial markets? Namely: what will happen to interest rates and return on capital over the next 50 years? What will the destruction of the old order by new technologies lead to?

Today, we can confidently prove that the return of capital (or the cost of capital - depending on which side you are on) tends to zero as technological progress grows.

Return on capital decreases with the growth of technological progress

Why?

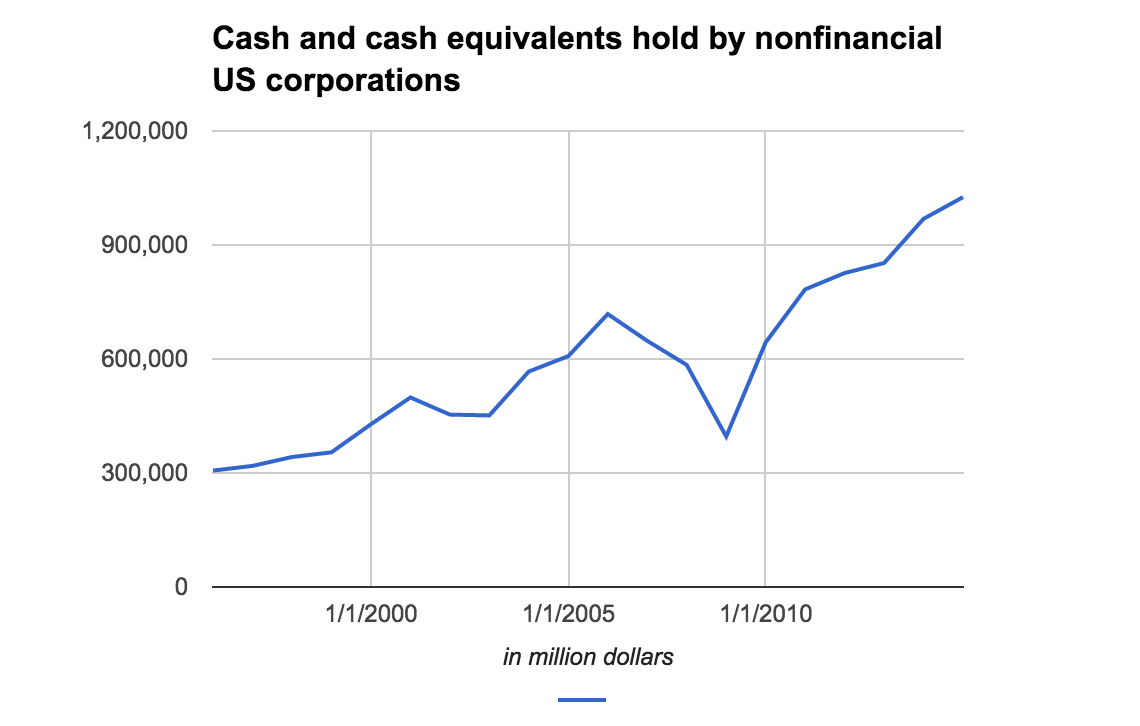

Technology makes innovation cheaper by increasing the availability of capital

During the industrial revolution, it was impossible to start a business without solid capital. Innovation depended on “heavy” tangible assets (for example, mining or foundry) and therefore required a solid investment. Now everything is arranged differently. Innovation and the creation of companies have never been so cheap. As a result, the supply of capital is growing rapidly. Corporations eat huge amounts of cash. At the end of 2014, there was more than one trillion dollars in cash on the balance sheet of US non-financial companies alone.

The reason is simple: lower demand for capital leads to higher availability, which, in turn, leads to a decrease in its profitability.

Balance of non-financial corporations in the United States, million dollars, according to the US Federal Reserve for 1995 - 2014

Technology improves capital market efficiency and capital availability

In addition to the fact that capital is becoming more accessible, the effectiveness of its attraction is also growing due to information technology. The advent of algorithmic trading and information technology such as the Bloomberg ★ terminal in the 90s made open markets more efficient. Companies such as Angellist, Mattermark, and Kickstarter are rapidly equalizing the information efficiency of the private investment market.

Arbitrage transactions ★ come to naught, and the possession of large capital no longer creates new opportunities in itself, which ultimately also leads to a decrease in return on capital.

Return on Assets in the US Economy 1965 - 2010, according to the Deloitte Shift Index

The trend is noticeable today in many industries. A study of 20,000 organizations in the United States between 1965 and 2010 shows that the return on capital today is only a quarter of the level of 1965.

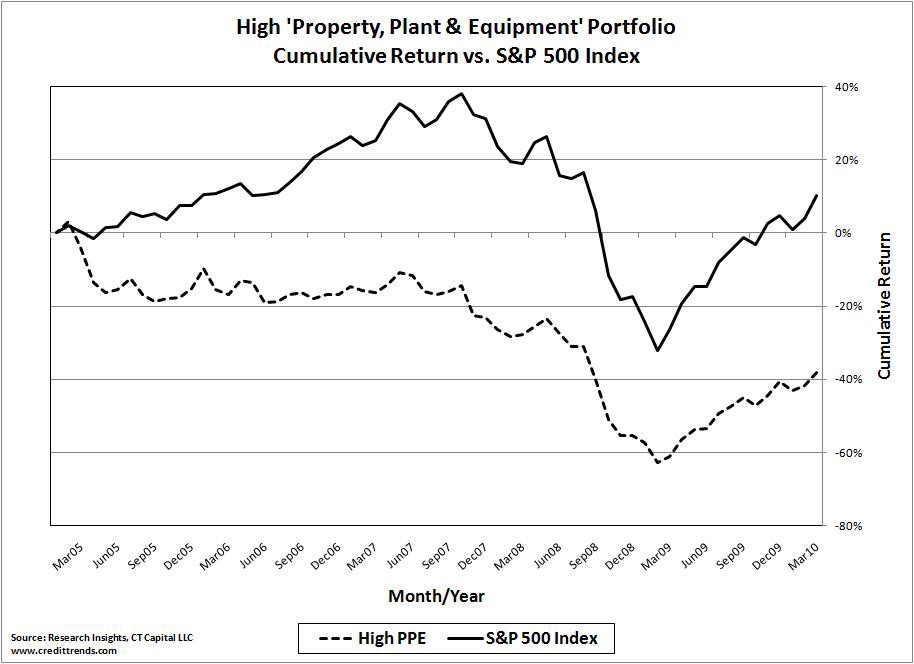

Reduced returns will be even more noticeable for capital-intensive industries

Companies requiring large investments will face an even more noticeable decline in profitability. Capital-intensive goods will be used (including jointly) more efficiently, which will lead to a decrease in demand for them. Sharing cars and bicycles is just the beginning. For the foreseeable future, households will produce and distribute electricity among themselves. Companies can use common power, 3D printers, heavy machines. An increase in the efficiency of collective consumption of capital-intensive goods will free up even more capital.

This trend has already affected the market value of companies with “heavy” assets. Profitability in resource-intensive industries, such as mining and steel industry, in recent decades is much lower than in light industry.

Comparison of heavy industry securities with the rest of the market, according to the S & P500.

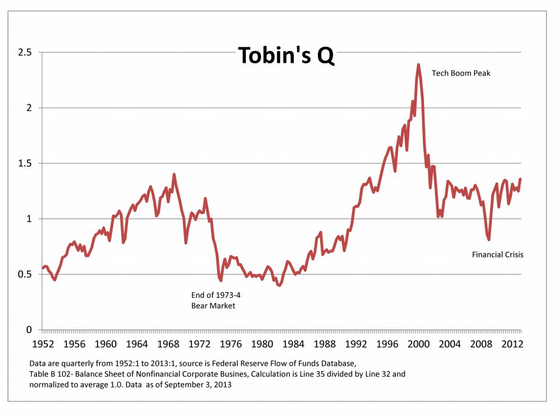

The dilemma of corporations with “heavy” assets also manifests itself in how we evaluate companies. The share of tangible assets no longer affects the value of the company in a situation where the economy is based on intellectual property. A significant deviation of the book value of assets from the valuation of the company itself (Tobin Ratio ★ ) was previously perceived as an anomaly, but now it is becoming the standard. Look at Google, Facebook, etc.

Tobin's Ratio: The ratio of a company's market value to the replacement value of its assets, according to the US Federal Reserve.

Be that as it may, the deviation of market value from the book value is caused not only by the flow of capital from the “heavy” to the “light” industries, but also by a lower profitability per se. The reason for the current high estimates of the value of technology companies (Uber, Pinterest, etc.) and the overall market growth are not so much the over-optimistic expectations of these companies' future earnings, but the realization of how little they will have to return to investors. Thus, the denominator by which we divide future cash flows is reduced, which gives a higher assessment of the value of the company today.

Lower barrier to entry will accelerate lower returns

Not the first year, entry barriers have been reduced in all sectors. In addition to reducing the capital required to start a business, lower returns work as a self-sustaining force, resulting in even lower returns. Investors and corporations are looking for the latest “high-yield” opportunities, acting as the “invisible hand of the market”, entering industries where profitability is still attractive. Opportunities for investment remain with an ever smaller return on capital.

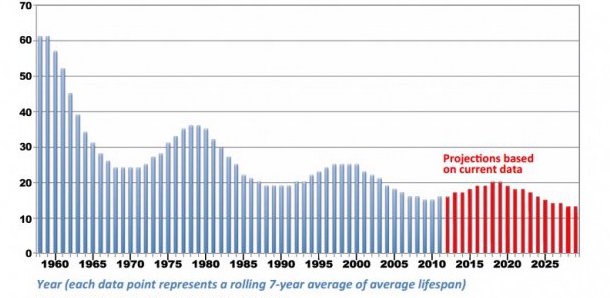

Lower entry barriers are already common in all sectors. Half a century ago, the life expectancy of Fortune 500 companies was 75 years, and today it has dropped to less than 15 years.

7-year moving average of the average life expectancy of a company. Richard Foster, Creative Destruction

What should an entrepreneur proceed from today?

- The increasing supply of capital will simplify its attraction for entrepreneurs. In recent years, record amounts have flowed into private equity and venture capital. (The average venture capital fund has grown in every way since 1980, according to the National Association of Venture Capitalists of the United States.)

- Private equity and risky investment funds will show lower returns compared to historical values.

- Growth in capital and constant changes in conditions will make predicting market bubbles even more difficult. (Even today it is unclear: are we in a bubble or not?)

- Innovative development will only accelerate, which, on the one hand, will allow companies to easily invade the market, but on the other, it will make it difficult for them to maintain their positions.

- With few exceptions, markets will become less saturated with more SMEs.

To summarize, the best way to achieve high returns is to be an entrepreneur.

And never before had there been more suitable conditions for this. ∎

About the Author: Paul Gebhardt is the CEO and founder of @bonusbox . Data fan, amateur chef, econometrics ★ With rich experience in the financial industry.