GDP, money supply and dynamic equilibrium

In the article “Balanced Currency and Multilateral Clearing”, I described the model of international settlements based on clearing and CDE - a balanced currency.

Here I will try to numerically simulate the economy of a single state participating in such a system.

I'll start with a description of the numerical model.

Let 20 independent entities participate in the country's economy.

Each produces a certain abstract product - in the amount of 100 SDE per unit of time.

Given the initial amount of money for each subject.

We will carry out three tests - with initial amounts of 50, 100 and 150 units of the national currency, respectively.

We set the initial exchange rate of the SDE to the national currency equal to 1.

In each unit of time, each entity can sell from 0 to 15 percent (a random number) of the product abroad and earn money on it.

The rest of the product is consumed.

Also, the subject can spend from 0 to 15 percent (a random number) of his money on the purchase of imported goods.

The initial balance of the country in the clearing system is zero.

Consider three cases:

1. The course of the SDE is fixed.

2. There is a time-independent feedback between the country's clearing balance sheet and the ETS exchange rate.

3. Time-dependent feedback.

The results of numerical simulation under the cut.

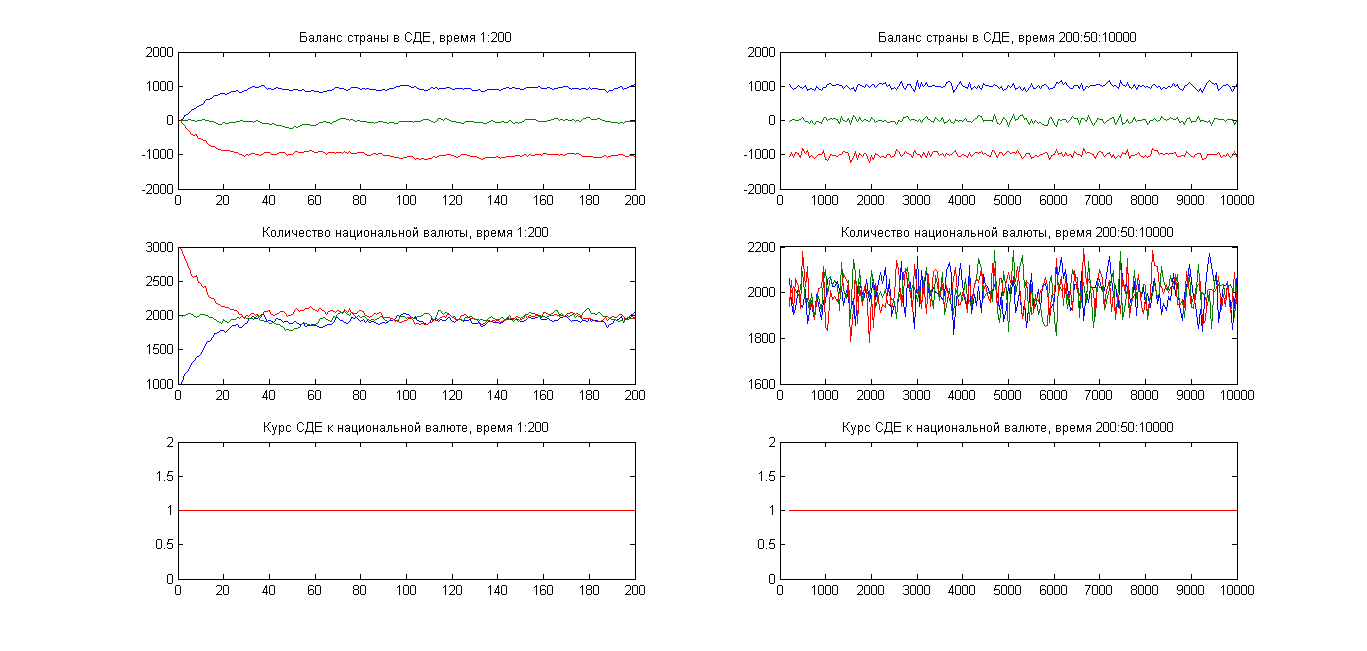

Fixed rate SDE.

The results in the graphs below.

On the graphs on the left - the time is from 1 to 200, on the graphs on the right - from 200 to 10000.

It can be seen that if the initial money supply is too large, it gradually falls to an equilibrium value, and, accordingly, increases if it is initially too small.

The country's clearing balance goes, respectively, to minus or plus, and stabilizes at a certain value.

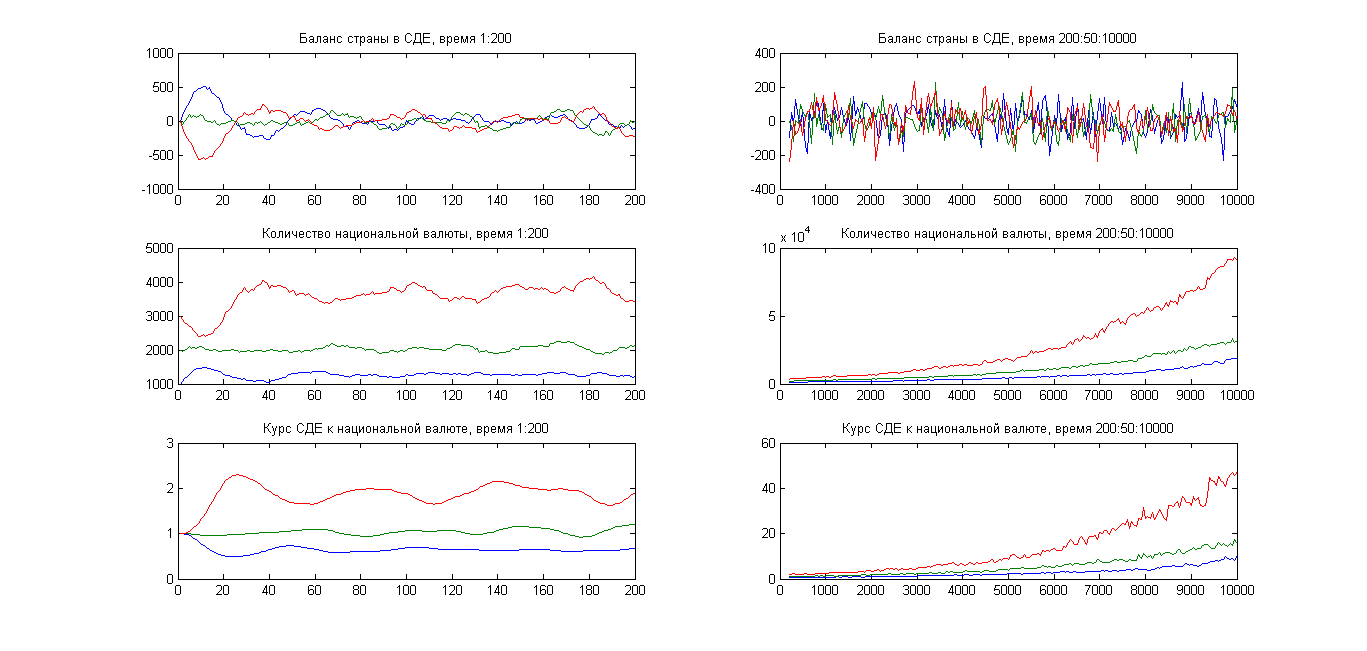

Feedback, not dependent on time.

The following feedback is used:

The results are as follows:

As you can see, the country's clearing balance gradually goes to fluctuations around zero.

But at the same time, there is a constant increase in the money supply and an increase in the SDE rate, in other words, inflation.

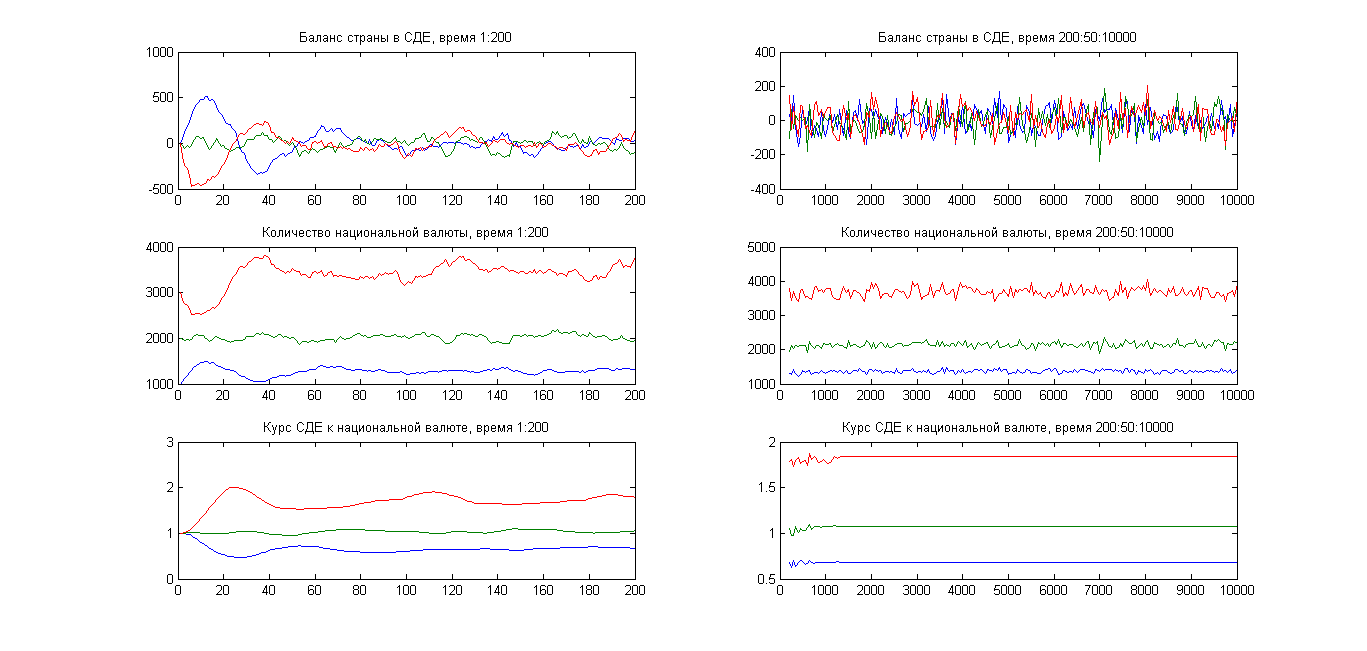

Time-dependent feedback (control).

Feedback is as follows:

That is, over time, it gradually weakens.

Result:

As you can see, the money supply and the SDE rate stabilize over time.

At the same time, the country's clearing balance fluctuates around zero.

That is, a dynamic equilibrium arises in the system.

Scripts here: github.com/tabatsky/jatx/tree/master/BMU

Here I will try to numerically simulate the economy of a single state participating in such a system.

I'll start with a description of the numerical model.

Let 20 independent entities participate in the country's economy.

Each produces a certain abstract product - in the amount of 100 SDE per unit of time.

Given the initial amount of money for each subject.

We will carry out three tests - with initial amounts of 50, 100 and 150 units of the national currency, respectively.

We set the initial exchange rate of the SDE to the national currency equal to 1.

In each unit of time, each entity can sell from 0 to 15 percent (a random number) of the product abroad and earn money on it.

The rest of the product is consumed.

Also, the subject can spend from 0 to 15 percent (a random number) of his money on the purchase of imported goods.

The initial balance of the country in the clearing system is zero.

Consider three cases:

1. The course of the SDE is fixed.

2. There is a time-independent feedback between the country's clearing balance sheet and the ETS exchange rate.

3. Time-dependent feedback.

The results of numerical simulation under the cut.

Fixed rate SDE.

The results in the graphs below.

On the graphs on the left - the time is from 1 to 200, on the graphs on the right - from 200 to 10000.

It can be seen that if the initial money supply is too large, it gradually falls to an equilibrium value, and, accordingly, increases if it is initially too small.

The country's clearing balance goes, respectively, to minus or plus, and stabilizes at a certain value.

Feedback, not dependent on time.

The following feedback is used:

BMU_course(t) = BMU_course(t-1)*BMU_feedback(BMU_balance(t-1),t);

%%%%%%%%

function [feedback] = BMU_feedback(BMU_balance, t)

q1 = 0.0001;

feedback = exp(-q1*BMU_balance);

end

The results are as follows:

As you can see, the country's clearing balance gradually goes to fluctuations around zero.

But at the same time, there is a constant increase in the money supply and an increase in the SDE rate, in other words, inflation.

Time-dependent feedback (control).

Feedback is as follows:

function [feedback] = BMU_feedback(BMU_balance, t)

q1 = 0.0001;

q2 = 0.003;

feedback = exp(-q1*BMU_balance)^exp(-q2*t);

end

That is, over time, it gradually weakens.

Result:

As you can see, the money supply and the SDE rate stabilize over time.

At the same time, the country's clearing balance fluctuates around zero.

That is, a dynamic equilibrium arises in the system.

Scripts here: github.com/tabatsky/jatx/tree/master/BMU