Enlarge your pension-3. Examples. Everything is relative

The first comment on the previous topic on fire fighting with kerosene was the issue of the contribution of empiricism to the formation of the accumulative portfolio. This is a very good, correct and timely question, immediately the sensibility of the habro-community is felt. Of course, “empirically” with your hind mind you can get any good numbers you want. Markowitz’s portfolio theory itself is not used precisely because all the characteristics of assets tend to change over time, including after the formation of an asset portfolio. Asset classes are easier.

In the West there is such a term as “simpleton's portfolio”, “bedcloth portfolio”. Let me be a simpleton (this assumption is not far from the truth) and I do not have an economic education. I choose where to invest. What markets can come to my mind? There are not so many of them:

- Shares (stocks);

- Debt markets (bonds) and money markets;

- Commodity markets (or at least gold);

- Real estate ( REIT funds ).

Because I’m a simpleton, I don’t quite understand the meaning of the words “if everything falls”. This term implies that certain assets will decline in price. Expressed in what? In money (which, men say, are not provided with anything at all ), well, let it be in gold. Therefore, money and instruments with fixed interest payments will increase my purchasing power in this situation when “everything has fallen”. Therefore, you need more gold!such assets should be in my portfolio. I can spend or invest the funds received from the growth of this share of the portfolio with the annual rebalancing of everything else that “fell”, hoping for excessive pessimism (and the authority of the Schiller noble who ate this dog) and the post-crisis recovery.

In general, one can go even further in generalizations and say that capital is forced to flow between the listed markets depending on economic conditions. We do not know exactly when and where the capital will go (and the interest of investors), we do not know when the economy will switch to which regime, but we know that there is basically nowhere to get capital from these markets. In the comments of the first topic, they rightly noted that capital, with hopelessness, is forced to paradoxically flow into money and American debts, and this is actually almost the case. Fuh, mastered formulating, never once using the term “deflation” ...

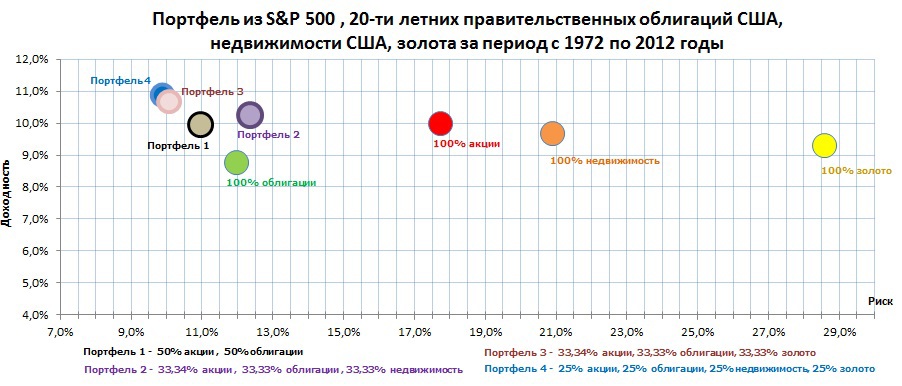

So I, as a simpleton, can try to solve the problem simply. For starters, I will fix in my portfolio equal shares of equity funds, bonds, real estate and gold. I’ll get such characteristics for the period since 1972 (before, there simply weren’t enough indices, but there were Bretton Woods agreements):

We look at the figure and remember that up means “more profitable”, to the right - “riskier”, to the left - “more reliable”. Our miracle portfolio (number 4) turned out to be in the upper left corner, defeating all other options in all respects. Gold and real estate fans can easily compare their favorite risk and return assets. I will provide real estate data for different countries in the future, and not just in the USA.

Finally, consider the Russian market. Financial advisors like to give the Russian market an example of a portfolio of stocks, bonds and gold in equal shares of one-third.

“Shares” - shares of the Dobrynya Nikitich open-end equity fund of UK “Dvoika-Obituary”;

“Bonds” - shares of the Ilya Muromets open-end fund of bonds of the same Asset Management Company “How many Uvolok”;

"Gold" - the discount price of gold of the Central Bank of Russia (in rubles per 1 g).

Continuing the naming tradition above, the portfolio should be called "St. Basil".because only the blessed one will keep pension savings in assets with a rating near Be-Be-Be-Be

Financial advisors prefer to start demonstrating such a portfolio from December 31, 1997, so that all the growth from the very bottom and crazy interest on bonds are included in the statistics - a statistical artifact that we are unlikely to encounter in such a cumulative form. Because we don’t have a task to vparit something to the reader, we will take the data more modestly, without an attractive artifact.

Since 2000 dynamics:

The weather results of the portfolio with annual rebalancing were as follows:

As you can see, in 2008 this portfolio lost as much as 25%. The mutual fund lost 70% that year, the bond mutual lost 30%, gold rose 25%. The following year, the equilibrium portfolio showed + 76% and won back losses (in the comments of the first topic they asked to indicate the set of assets for recovery from the fall of 2008). Over the past two years, the portfolio has been losing inflation somewhat, but there is nothing perfect, any asset is sometimes falling in price or losing inflation, the long-term result, which turned out to be at the stock market level, is important to us.

Further, on average, the equilibrium portfolio grew by 24%, and the unit investment trusts grew by 22% per year. Those. reducing the fluctuations, we also raised the yield.

To be continued .

In the West there is such a term as “simpleton's portfolio”, “bedcloth portfolio”. Let me be a simpleton (this assumption is not far from the truth) and I do not have an economic education. I choose where to invest. What markets can come to my mind? There are not so many of them:

- Shares (stocks);

- Debt markets (bonds) and money markets;

- Commodity markets (or at least gold);

- Real estate ( REIT funds ).

Because I’m a simpleton, I don’t quite understand the meaning of the words “if everything falls”. This term implies that certain assets will decline in price. Expressed in what? In money (

In general, one can go even further in generalizations and say that capital is forced to flow between the listed markets depending on economic conditions. We do not know exactly when and where the capital will go (and the interest of investors), we do not know when the economy will switch to which regime, but we know that there is basically nowhere to get capital from these markets. In the comments of the first topic, they rightly noted that capital, with hopelessness, is forced to paradoxically flow into money and American debts, and this is actually almost the case. Fuh, mastered formulating, never once using the term “deflation” ...

So I, as a simpleton, can try to solve the problem simply. For starters, I will fix in my portfolio equal shares of equity funds, bonds, real estate and gold. I’ll get such characteristics for the period since 1972 (before, there simply weren’t enough indices, but there were Bretton Woods agreements):

We look at the figure and remember that up means “more profitable”, to the right - “riskier”, to the left - “more reliable”. Our miracle portfolio (number 4) turned out to be in the upper left corner, defeating all other options in all respects. Gold and real estate fans can easily compare their favorite risk and return assets. I will provide real estate data for different countries in the future, and not just in the USA.

Finally, consider the Russian market. Financial advisors like to give the Russian market an example of a portfolio of stocks, bonds and gold in equal shares of one-third.

“Shares” - shares of the Dobrynya Nikitich open-end equity fund of UK “Dvoika-Obituary”;

“Bonds” - shares of the Ilya Muromets open-end fund of bonds of the same Asset Management Company “How many Uvolok”;

"Gold" - the discount price of gold of the Central Bank of Russia (in rubles per 1 g).

Continuing the naming tradition above, the portfolio should be called "St. Basil".

Financial advisors prefer to start demonstrating such a portfolio from December 31, 1997, so that all the growth from the very bottom and crazy interest on bonds are included in the statistics - a statistical artifact that we are unlikely to encounter in such a cumulative form. Because we don’t have a task to vparit something to the reader, we will take the data more modestly, without an attractive artifact.

Since 2000 dynamics:

| Assets | Nominal average annual yield, 2000-2012 | Average annual inflation-adjusted return 2000-2012 |

| Ruble | 0% | -12.1% |

| U.S. dollar | + 1.5% | -10.7% |

| Euro | + 3.6% | -8.5% |

| Inflation | + 12.1% | |

| Gold | + 17.4% | + 5.2% |

| Housing in Moscow | + 19.8% | + 7.7% |

| MICEX Index | + 20.3% | + 8.2% |

| Mutual fund bonds Ilya Muromets | + 22.1% | + 10.0% |

| Mutual fund shares Dobrynya Nikitich | + 22.3% | + 10.2% |

| Briefcase "St. Basil" | + 24.4% | + 12.2% |

The weather results of the portfolio with annual rebalancing were as follows:

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| + 45.3% | + 52.9% | + 38% | + 20% | + 15.2% | + 41% | + 23% | + 13.2% | -25% | + 76% | +24.7 | -0.2% | + 6.6% |

As you can see, in 2008 this portfolio lost as much as 25%. The mutual fund lost 70% that year, the bond mutual lost 30%, gold rose 25%. The following year, the equilibrium portfolio showed + 76% and won back losses (in the comments of the first topic they asked to indicate the set of assets for recovery from the fall of 2008). Over the past two years, the portfolio has been losing inflation somewhat, but there is nothing perfect, any asset is sometimes falling in price or losing inflation, the long-term result, which turned out to be at the stock market level, is important to us.

Further, on average, the equilibrium portfolio grew by 24%, and the unit investment trusts grew by 22% per year. Those. reducing the fluctuations, we also raised the yield.

To be continued .