Why do we need product managers in fintech

Everyone knows that product managers do e-commerce: they optimize the funnel and come up with “how to make the site as convenient for shopping as home slippers for going to the kitchen at night”. But today, almost any self-respecting company, which is somehow present in the digital, begins to introduce a grocery approach to its work: telecom, banks, insurance ... even fast food.

Under the cut, Alexander Okulov from ID Finance talks about the issues that are facing products in Fintech, digital from birth, but he has taken a lot from his parents, traditional banks and finance. In Fintech, as a rule, business is built around a product and everywhere solid agile, but only those who are over 30 and who managed to work in dinosaur companies heard about the “waterfall”.

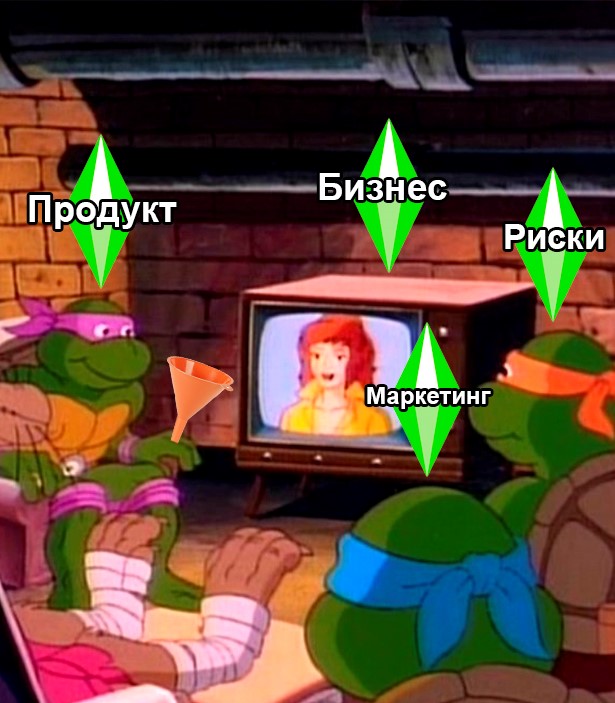

The product in Fintech is just one of these turtles, which, like in e-commerce, carries a funnel. Two more turtles are marketing and risks. Marketing leads traffic to the funnel, and the risks put filters in his neck. If one of the three turtles is limping, a business can tilt and default.

This is a key difference from digital companies, where often there is only product and product marketing. Almost half of the issues that a particular turtle has to solve are at the junction of the responsibility of the other two, and therefore they have to be solved together in a team, they have a lot to discuss and test a lot.

Hence, a very important feature of product issues in Fintech: one needs to understand the slang of colleagues, first of all from the risks, the dependence between adjacent KPIs and how changes of one lead to changes in another.

Let's start with slang, and then look at a few case studies when products need to interact with pragmatic risk mathematicians and dreamy marketers.

AR - approval rate. Ratio of approved loans to submitted applications.

IR - issue rate. The ratio of loans to applications submitted (it happens that the company approved the loan, but it was not issued: the bank rejected the transaction or the borrower changed his mind).

RR - recovery rate. The ratio of cash flow to outgoing.

NPL - non performing loan. The ratio of the number of "not paying" customers to those who pay on time. In other words, a delay.

NPL2, NPL15, NPL30, NPL90 - non performing loan after 2,15,30,90 days. The ratio of NPL taken 2,15,30,90 days after the date of the planned receipt.

FPD, SPD, TDP- first (second, third) payment default. The term relevant for loans with annuity payments is the ratio of the number of “not paying” the first (second, third) payment to those who pay this payment on time.

As you have probably guessed, all these indicators are expressed in percentages and many of them are relevant for the entire banking industry, although they can be called differently. For example, even in our company, financiers have their own strange terminology, which they use. Well, you need to watch these figures in the context of vintages. What? Yes, I also called them “blends” before and could not understand why the financiers perverted the well-known terminology of cohort analysis. In short, in the vintage finance ~ cohort, only a cohort of clients, not loans. To dot the risk, I must say that the most important indicators are RR, NPL and AR.

The food world lives in the paradigm of the unit economy and LTV (life time value, customer life cycle) and few have heard about recovery, but in fact they are very similar. Both that and another about that, how much you earn from a certain group. But here are the differences:

Example

Imagine a credit product lasting for 12 months. Every year you issue these 12-month loans every day. How to understand how much you earned by the results of the year, because many may not return the loan, many may close the loan ahead of schedule, etc.? To do this, you need to wait until the user pays up to 3-4 payments on these loans (“let them mature”) and then, based on the statistics of each vintage, you can predict the recovery of your portfolio. Calculate the proceeds further is easy.

Why does the product need this indicator? Very often, when you test business changes, rather than UI / UX (usability), which is easier to measure in conversion, then the main "measure" of the effect will be recovery, an indicator reflecting the specific increase in your earnings.

NPL- This is the second most important indicator. It applies to vintages and to the entire portfolio. This indicator characterizes user traffic that has penetrated into your funnel and brings you money. And the closer it is to 0% - the better, 0% means that all customers pay loans. So, of course, does not happen in real life. There are always users who do not pay for their subscription to Netflix. But Netflix can simply disable their access to their content. We can not take the money back, so for us it is a loss that greatly affects the economy of both the product and the entire business. And about every other test that products launch and marketing requires an assessment of the change of the NPL.

AR / IR. We all know how banks work, they “turn on” us, drive the data collected about us through their risk assessment models, give us points and define a “good” or “not good enough” client in front of them. Approval level is the result of scoring. The more advanced the scoring model of the company, the more customers it can get on the market, and the greater the return on investment in attracting customers.

I hope you understand that the designated risk indicators are only the tip of the iceberg.

They are very similar to the grocery, it is important how the departments agree on areas of responsibility within the company. As a rule, CR (conversion) and retention are joint product-marketing indicators, while the cost of attracting a client is a purely marketing indicator.

You understand that marketing is always to blame for everything? Or almost always. This is, of course, a joke.

As I have already said, one of the most important product liability areas in ID Finance is a funnel: the process when a user becomes our client visiting our website. Funnels in different services can be technically arranged in different ways, but the goal of products is always the same: minimize costs (funnel costs: APIs, comminications, processing, identification, OCR and other) and maximize the number of users who reach the neck - CR (conversion). Here and solving design issues and UI, UX (usability), API integration (in our funnels a lot of integration with third-party services), the return of abandoned registrations (they also abandoned basket in online shopping), security issues, modeling cases and miscalculation of the economy of improvements - all it's in the fight for precious conversion percentage points.

However, enveloping a user from the site is only the beginning. Users who have become owners of the valuable title of a new client have yet to be wrapped in repeat customers. There works a standard tandem of marketing and product managers - together we figure out how to do it and monitor retention (we have ~ 90%). The whole arsenal of direct marketing and communications, the development of attractive product offers (but with a good economy), bonus programs, discount programs, etc. are used. And, of course, a couple of years after the start of the project, repeated users become the main source of profit, and we actively care about them and think.

The economy is the most interesting and the most difficult part in the development of product functionality in Fintech. Here we follow the average check (average check), and LT / LTV. When testing and developing product features, it is necessary to track the entire heap of indicators. This is the most difficult thing, because we are partly in the “risk” glade, the owners of the indicators (delay and recovery), who really do not like to take risks.

They will try to minimize the proportion of traffic to test branches, invent many reasons why you should be careful. It is necessary to give them their due - they are often right, mathematics after all. And a compromise is what helps to find a middle ground between the riskiness of our MVP and minimization of possible losses in case of a feil. Tests in the field of product economics are quite long, but if the test is successful, it can bring good dividends to the product and business.

Our business is difficult and without products in Fintech in any way. You need to be a technician to communicate in the same language with the dev team and set a development task, you need to understand business perfectly to develop and tune products, and you need to be a manager to make everything move at the right pace.

In the next article I’ll tell you the furious cases about how your cool product feature can boost both RR and NPL at the same time, and how you can improve CR while reducing, for example, AR.

Under the cut, Alexander Okulov from ID Finance talks about the issues that are facing products in Fintech, digital from birth, but he has taken a lot from his parents, traditional banks and finance. In Fintech, as a rule, business is built around a product and everywhere solid agile, but only those who are over 30 and who managed to work in dinosaur companies heard about the “waterfall”.

A couple of words about the three turtles

The product in Fintech is just one of these turtles, which, like in e-commerce, carries a funnel. Two more turtles are marketing and risks. Marketing leads traffic to the funnel, and the risks put filters in his neck. If one of the three turtles is limping, a business can tilt and default.

This is a key difference from digital companies, where often there is only product and product marketing. Almost half of the issues that a particular turtle has to solve are at the junction of the responsibility of the other two, and therefore they have to be solved together in a team, they have a lot to discuss and test a lot.

Hence, a very important feature of product issues in Fintech: one needs to understand the slang of colleagues, first of all from the risks, the dependence between adjacent KPIs and how changes of one lead to changes in another.

Let's start with slang, and then look at a few case studies when products need to interact with pragmatic risk mathematicians and dreamy marketers.

Slang credit riskists

AR - approval rate. Ratio of approved loans to submitted applications.

IR - issue rate. The ratio of loans to applications submitted (it happens that the company approved the loan, but it was not issued: the bank rejected the transaction or the borrower changed his mind).

RR - recovery rate. The ratio of cash flow to outgoing.

NPL - non performing loan. The ratio of the number of "not paying" customers to those who pay on time. In other words, a delay.

NPL2, NPL15, NPL30, NPL90 - non performing loan after 2,15,30,90 days. The ratio of NPL taken 2,15,30,90 days after the date of the planned receipt.

FPD, SPD, TDP- first (second, third) payment default. The term relevant for loans with annuity payments is the ratio of the number of “not paying” the first (second, third) payment to those who pay this payment on time.

As you have probably guessed, all these indicators are expressed in percentages and many of them are relevant for the entire banking industry, although they can be called differently. For example, even in our company, financiers have their own strange terminology, which they use. Well, you need to watch these figures in the context of vintages. What? Yes, I also called them “blends” before and could not understand why the financiers perverted the well-known terminology of cohort analysis. In short, in the vintage finance ~ cohort, only a cohort of clients, not loans. To dot the risk, I must say that the most important indicators are RR, NPL and AR.

A bit about recovery

The food world lives in the paradigm of the unit economy and LTV (life time value, customer life cycle) and few have heard about recovery, but in fact they are very similar. Both that and another about that, how much you earn from a certain group. But here are the differences:

- recovery is the ratio of the incoming cash flow to the outgoing cash flow of a certain vintage, and LTV is the difference of static values (income minus expense)

- recovery shows the yield of one vintage within one credit cycle, and LTV over the entire life cycle.

- one in percent, the other in currency.

Example

Imagine a credit product lasting for 12 months. Every year you issue these 12-month loans every day. How to understand how much you earned by the results of the year, because many may not return the loan, many may close the loan ahead of schedule, etc.? To do this, you need to wait until the user pays up to 3-4 payments on these loans (“let them mature”) and then, based on the statistics of each vintage, you can predict the recovery of your portfolio. Calculate the proceeds further is easy.

Why does the product need this indicator? Very often, when you test business changes, rather than UI / UX (usability), which is easier to measure in conversion, then the main "measure" of the effect will be recovery, an indicator reflecting the specific increase in your earnings.

NPL- This is the second most important indicator. It applies to vintages and to the entire portfolio. This indicator characterizes user traffic that has penetrated into your funnel and brings you money. And the closer it is to 0% - the better, 0% means that all customers pay loans. So, of course, does not happen in real life. There are always users who do not pay for their subscription to Netflix. But Netflix can simply disable their access to their content. We can not take the money back, so for us it is a loss that greatly affects the economy of both the product and the entire business. And about every other test that products launch and marketing requires an assessment of the change of the NPL.

AR / IR. We all know how banks work, they “turn on” us, drive the data collected about us through their risk assessment models, give us points and define a “good” or “not good enough” client in front of them. Approval level is the result of scoring. The more advanced the scoring model of the company, the more customers it can get on the market, and the greater the return on investment in attracting customers.

I hope you understand that the designated risk indicators are only the tip of the iceberg.

Marketing figures

They are very similar to the grocery, it is important how the departments agree on areas of responsibility within the company. As a rule, CR (conversion) and retention are joint product-marketing indicators, while the cost of attracting a client is a purely marketing indicator.

- The traffic for which marketing is responsible strongly affects the conversion. You can drive tons of users, from which the units will reach the end of the funnel. Because, for example, this is completely untargeted traffic.

- Traffic that can be well converted - can pass badly through the scoring barrier. Again, because these are just not the customers you need.

- Traffic that is well converted and even goes through scoring may also not be what you are looking for. Just because his NPL may be above average.

You understand that marketing is always to blame for everything? Or almost always. This is, of course, a joke.

Main goal of the products

As I have already said, one of the most important product liability areas in ID Finance is a funnel: the process when a user becomes our client visiting our website. Funnels in different services can be technically arranged in different ways, but the goal of products is always the same: minimize costs (funnel costs: APIs, comminications, processing, identification, OCR and other) and maximize the number of users who reach the neck - CR (conversion). Here and solving design issues and UI, UX (usability), API integration (in our funnels a lot of integration with third-party services), the return of abandoned registrations (they also abandoned basket in online shopping), security issues, modeling cases and miscalculation of the economy of improvements - all it's in the fight for precious conversion percentage points.

However, enveloping a user from the site is only the beginning. Users who have become owners of the valuable title of a new client have yet to be wrapped in repeat customers. There works a standard tandem of marketing and product managers - together we figure out how to do it and monitor retention (we have ~ 90%). The whole arsenal of direct marketing and communications, the development of attractive product offers (but with a good economy), bonus programs, discount programs, etc. are used. And, of course, a couple of years after the start of the project, repeated users become the main source of profit, and we actively care about them and think.

Project economics

The economy is the most interesting and the most difficult part in the development of product functionality in Fintech. Here we follow the average check (average check), and LT / LTV. When testing and developing product features, it is necessary to track the entire heap of indicators. This is the most difficult thing, because we are partly in the “risk” glade, the owners of the indicators (delay and recovery), who really do not like to take risks.

They will try to minimize the proportion of traffic to test branches, invent many reasons why you should be careful. It is necessary to give them their due - they are often right, mathematics after all. And a compromise is what helps to find a middle ground between the riskiness of our MVP and minimization of possible losses in case of a feil. Tests in the field of product economics are quite long, but if the test is successful, it can bring good dividends to the product and business.

Our business is difficult and without products in Fintech in any way. You need to be a technician to communicate in the same language with the dev team and set a development task, you need to understand business perfectly to develop and tune products, and you need to be a manager to make everything move at the right pace.

In the next article I’ll tell you the furious cases about how your cool product feature can boost both RR and NPL at the same time, and how you can improve CR while reducing, for example, AR.