Prospects for Venture Capital 2016

- Transfer

GVA LaunchGurus has translated for you this intriguing article by Mark Saster, partner of Upfront Ventures, about the prospects for venture capital in 2016. The expert spoke about current trends in the behavior of market players and future changes in venture capital investment.

Mark Saster:

At the moment, there is a lot of uncertainty about the status of the private, fast-growing technology and venture capital markets that underlie them. On the one hand, innovation is now on an unprecedented boom thanks to features such as high speed communications, an increase in the number of smartphones, the promotion of trading through social networks and the fact that we can make a purchase on Amazon, Apple, Google or PayPal in one click.

In 2012, I wrote an article entitled “The dawn of venture capital ”, which already described these trends, and in 2014 I published a presentation“ Why venture capital is most attractive ”, where new data on many of our past analytical studies were presented.

Fast forward three years, and what will we see on the horizon of 2016? It will be more likely the sunset of venture capital, in the sense of the sunset of days of rational behavior in this area. There is no one to blame for this recklessness - it is just that the laws of the market operate, and history does not teach us anything. The boom-decline cycle. The coolest companies appeared in the last stagnant period, and we all see how successful they are - Facebook, Twitter, Tesla and others. Prior to this, Google, Salesforce, and LinkedIn appeared among others.

Technology innovations enrich venture capital with new companies and contributions - this is the reward for investment partnerships to rediscover our asset class. Who to blame? These partnerships? Venture capital? Or a flood of new entrepreneurs and woeful entrepreneurs seeking fame and fortune? Neither one nor the other, nor the third. It’s the same as blaming the press for continuous reports about Donald Trump, and then, at the sight of Donald Trump’s rating in the debate, be surprised that the press is paying so much attention to him. The market is the market.

The modern private technology market is definitely in the bubble. According to Wikipedia, a bubble is

“trading in securities at prices substantially different from fair prices”.

Objections that, they say: "This time, startups bring real income," or that "market value is growing, then this is not a bubble," are unconvincing. And the definition of “price significantly different from the fair price” sounds quite convincing. The market gave us what investment guru Michael Moritz defined as “ second-rate unicorns (startups worth more than $ 1 billion).” How elegantly said.

Definition of a “bubble” from Investopedia :

“A jump in prices, more than justified by non-market factors, and usually appearing in a particular sector. It is usually followed by a drop in prices after the start of an active sale of financial instruments. ”

The jump in prices. More than justified. Usually in a specific sector. Let's take a closer look.

Last week I spoke at the annual Cendana conference on venture capital and investment partnerships. Cendana founder Michael Kim was one of the first to notice changes in venture capital that led to the seed stages of investing, and funded many of the best projects in the area. It is always a great honor to meet with such illustrious colleagues. Click here to download my presentation from the summit. Final venture outlook 2016 from Mark Suster

If the “market” stimulates price increases beyond the real value of the asset, then new players appear on the market who are not so rational in assessing actual prices — a number of non-venture funds, including corporate investors, hedge funds, crowdsourcing. Please note that I do not justify what is happening in the industry - in the field of venture capital. I just want to emphasize that price increases are closely related to outsiders. The graph below shows that 78% of rounds of financing for 80 companies worth over a billion dollars were conducted by non-business investors.

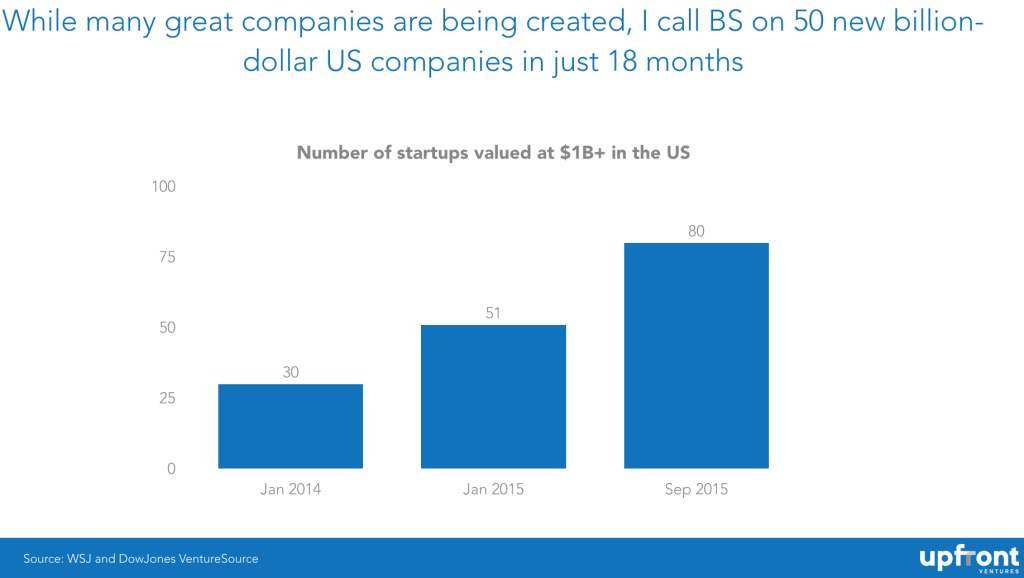

Although there are a lot of great companies, I doubt very much that there were 50 new companies worth a billion in the world in 18 months.

US $ 1 billion or more startups

US $ 1 billion or more startups

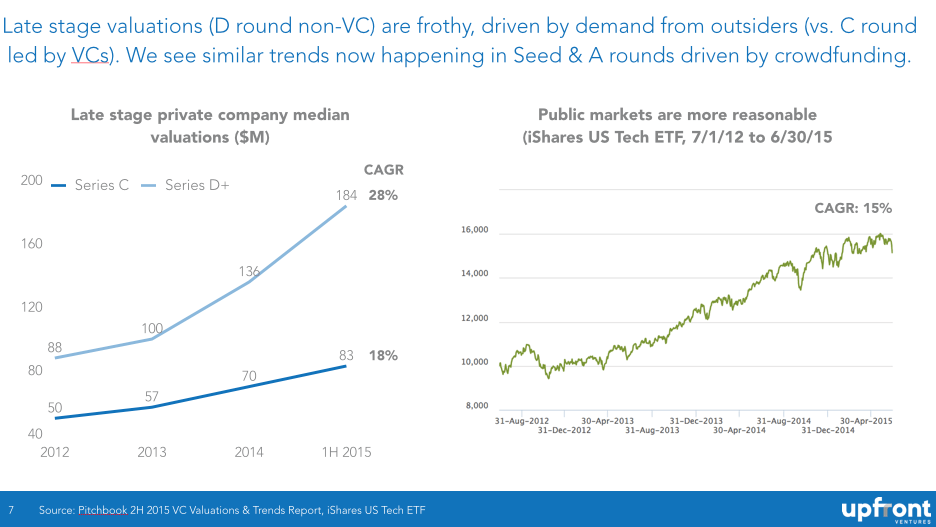

So that you better understand how quickly we created a “second-rate startup market” (as Michael Moritz calls it): over the past year and a half, in the US alone, the number of private companies engaged in new technologies and valued at more than a billion (which some already consider to be high ) grew from 30 to more than 80. Either we got magic beans and elixirs, or we rushed to our calculations. Below is a graph showing the average rating of private companies in the late stages of development compared to traditional rounds of financing for company development conducted by venture funds, as well as compared to open markets.

Late-stage evaluations of companies (round D, non-venture capital) are superficial and are dictated by the needs of outsiders (compared to round C conducted by venture funds). We can observe similar trends during the sowing rounds A and B, carried out using crowdfunding.

Medium priced, late stage private companies (SMT) Open markets are more adequate (US Tech ETF stocks from 1/7/12 to 30/6/15)

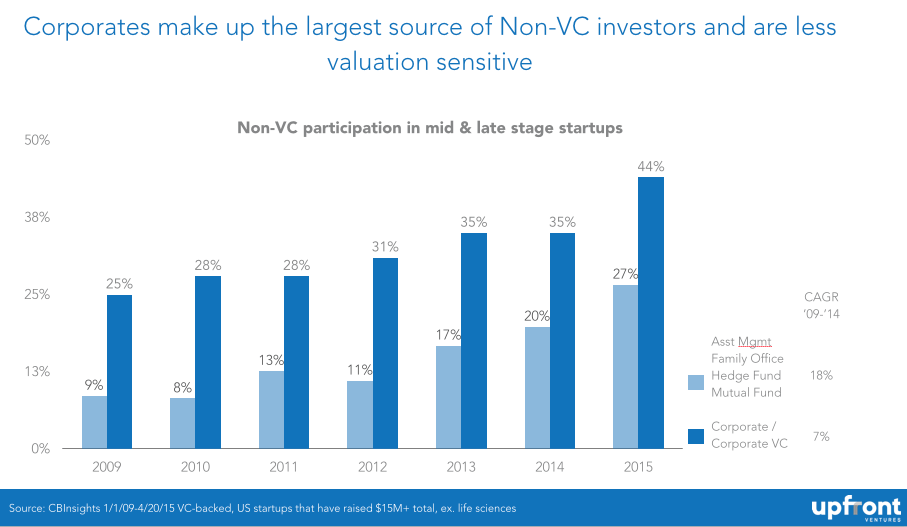

And after it is discovered what factors contributed to the increase in the members of the club of second-rate startups, then you can track the money that leads to a small number of sources. Firstly, corporate investors, including Google, Rakuten, Alibaba, Comcast, and others have increased their investment in enterprises, and they are often guided by not the same profit motives (and thus not the same pricing mechanisms) as traditional investors. This is not a damning statement or an accusation against corporate investors - just admit that there are often strategic reasons for investing in addition to those that are usually determined by the actions of a financial investor.

Corporations make up the majority of non-venture investors and pay less attention to valuations.

Non-venture presence in startups at intermediate and late stages of development

Perhaps the most interesting is the actions of mutual funds and hedge funds to penetrate the private capital market. As I wrote in the post Structural Changes in the Venture Capital Industry , private technology companies postpone the initial public offering, and thus private technology investors earn more until the actual public offering, and public investors feel the need to respond.

And what is the reaction?

Mature funds thumped money into companies that seemed to them the closest competitors of already public companies, and one informed person described this action as a simple “preliminary buying up of placed shares in order to become owners of shares after the companies become public.”

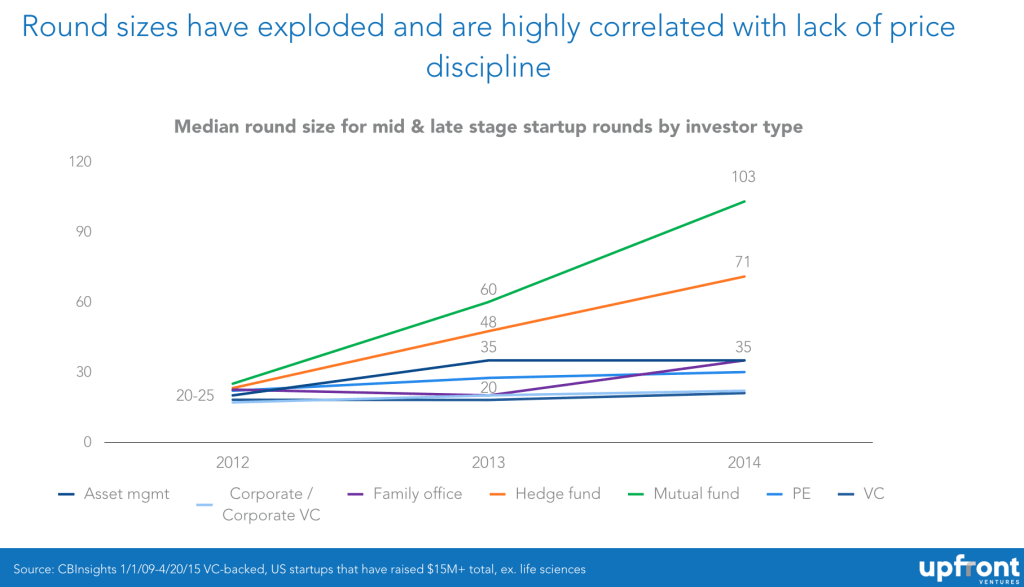

Round sizes reached unprecedented values, which is directly related to the lack of discipline in pricing. The

average size of rounds for startups at the intermediate and late stages of development by type of investor

In just two years, the average size of a round involving mutual funds has more than tripled, and the same phenomenon is observed in hedge funds. Therefore, we can say that a huge amount of money revolves around ecosystems in the late stages of development. This is good for entrepreneurs in fast-paced technology - isn't it? Is not it? Not so simple. It turns out that the company will have its Doomsday. They will either have to place their shares, or they will be bought by large companies, which are likely to be public themselves. Everything should return to square one.

Open market investors are not as stupid as private investors are trying to make them. Of course, they integrate protection mechanisms into their financial transactions, which allows them to avoid losses during the initial public offering if the price is lower than the price paid by them. So is the price they pay today for a company worth more than a billion? Does it really cost more than a billion dollars, or as Michael Moritz puts it, are we creating second-rate unicorns again?

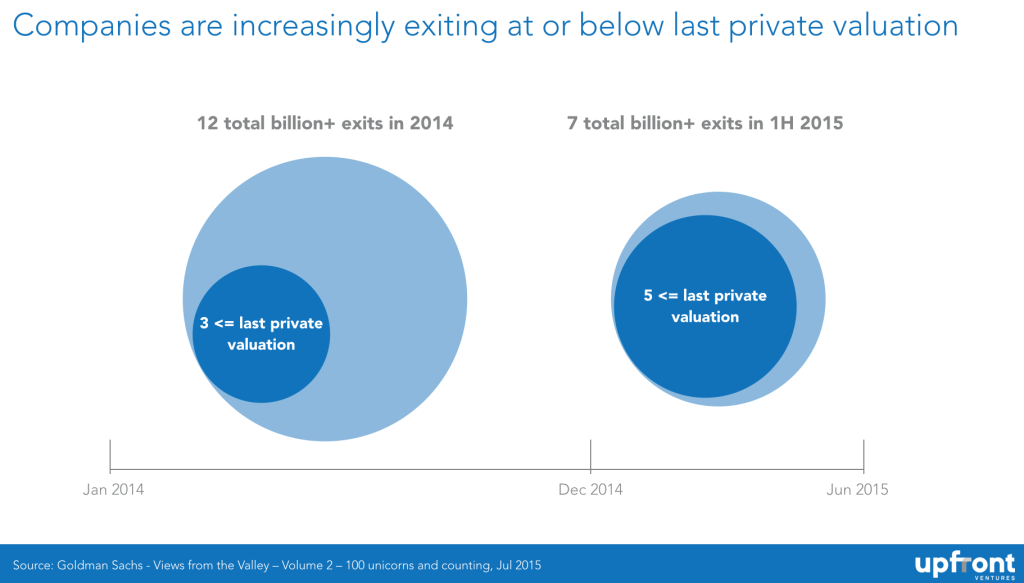

Increasingly, companies sell at a price equal to or lower than their value according to the latest assessment of

12 transactions for the sale of shares with a total value of more than 12 billion in 2012

7 transactions for the sale of shares with a total value of more than 7 billion in the first half of 2015

As usual - the market gives us clues. In 3 out of 12 cases, investors sold their shares at a price lower than their value as estimated in the previous round. 25% discount sales? Sorry sight. But a year later, in 2015, 5 out of 7 sales were carried out at a lower price. I myself will calculate: this is already 71% of transactions.

And it’s difficult to make any forecast for 2016 without recognizing the role that crowdsourcing in the startup market is beginning to play. Over the past 2 years, we have seen an influx of high-tech companies funded through crowdsourcing platforms. Those who read this article, of course, know that AngelList is an undoubted leader and a platform worthy of all respect, but many new platforms have reached the world level. Funding through them only in the last 2 years has reached unprecedented heights, and increased from 400 million to 2.6 billion dollars.

Meanwhile, on the other side of the market - CAGR crowdfunding indicator over the past 2 years reached 153%.

The total amount of funds raised through crowdfunding around the world.

Of course, at first glance this will sound implausible, I myself read a lot of figurative statements on the topic of how dead venture capital is, and that it will soon be replaced by a gang of altruists - former founders who wake up the rain of investment on startups. The reality is more sophisticated.

For starters, conditions that are not offered to entrepreneurs with a convertible loan, much worse than the conditions offered by seed and venture funds, which are evaluated by companies, but only recently, entrepreneurs have started talking about this. Although these are trifles in comparison with the large-scale swindle of inexperienced investors that has begun. I openly warned about this for several years every time when it came to crowdfunding, but now the sell has become so obvious that even the Securities and Exchange Commission (SEC) should take a closer look at the activities of crowdfunding platforms.

I receive many letters from caring strangers describing a particular startup and urging them to invest as soon as possible, “before it's too late,” and at the same time convincing investors that they can enter into a deal only if they replenish the fund of the undersigned. I often saw transactions recommended by the platform, where even the most necessary information is not given, the study of which would temper, I think, the desire to invest.

Why not? The platform often charges fees. The platform does not bear the costs of maintaining the investment position. And what many do not understand is that many syndicates work according to the deal by deal scheme. For an investor, this means that if the transaction that he concluded is closed (and 49 more transactions are covered), then the management of the syndicate can still earn a lot of money on these 50 transactions, since he / she does not incur losses due to other failed transactions . Therefore, investment partnerships do not allow venture funds to work under a deal by deal.

The founders of the companies will pay for this short crowdfunding boom. In conditions when “every transaction is winning” and money flows in a river, they will receive their money through intermediary financing, but when the market will inevitably make its adjustments - who will carry out subsequent financing of these companies stranded? I understand that the final chords have not yet sounded, but they will sound.

What is my forecast for 2016?

1. I think that in 2016 the market for private technology companies will cool down, but I have been predicting this for 2 years, so hell knows. Although I know that markets are overvalued, but one in the field is not a warrior, i.e. one player cannot change market prices. That is why the scandal in the 38 Bin barwas just a distraction. I will continue to invest in the early stages in companies that will fundamentally change some aspects of the industry in an adequate period of time (8-12 + years). Soon, only cats will be born, and if it is not a bubble, money does not come immediately.

2. We will continue to observe excessive financing in the late stages of company development until the veil is overlooked, and then, according to my predictions, reasonable non-venture investors will return to their direct responsibilities and again begin to seek profits in other areas, and we - those who understands something in venture funds, we will continue to do our business.

3. The growth of crowdfunding as an equivalent alternative to venture capital will not decrease. Too much (relative to its value) capital will be directed into this direction until the next recession, when many inexperienced investors go broke, or until the SEC (Securities and Exchange Commission) begins to spread doubtful platforms or investors on these platforms. I suspect that this will happen after 2016, when retail investors get tired of waiting for easy money in the technology market.

4. In the meantime, technological progress will continue to evolve regardless of how many startups are evaluated there. Technology will continue to deeply influence society and industry, and grab ever larger pieces of the economic pie. And I suspect that for a long time, venture capital will play a decisive role in supporting great entrepreneurs.

I would like to thank my colleague Kevin Zheng for his tireless work in monitoring the trends of intermediary financing on behalf of Upfront Ventures. His work is invaluable, and if you follow him on Twitter, you will learn a lot of useful things.

Mark Saster is a partner at Upfront Ventures. He joined the company in 2007, after 8 years already working with Upfront Ventures as a two-front entrepreneur. Prior to joining Upfront, Mark served as vice president of production management at Salesforce.com, after the company was acquired by Koral, where he, in turn, was one of the founders and CEO. Prior to Koral, Mark ran his own firm, BuildOnline, a European software company (SaaS), which was subsequently acquired by the SWORD group. Mark is always looking for enthusiastic entrepreneurs to invest in projects in the early stages of technology development. His areas of interest include digital content and distribution, AdTech, consumer Internet technologies, and SaaS companies; Mark has impressive experience in this sector, given that he founded and sold two companies already. Follow the link to read his articles on his blogBoth Sides of the Table (“On Two Chairs”).

The original article can be read on the link on the AlwaysOn blog .

Mark Saster:

At the moment, there is a lot of uncertainty about the status of the private, fast-growing technology and venture capital markets that underlie them. On the one hand, innovation is now on an unprecedented boom thanks to features such as high speed communications, an increase in the number of smartphones, the promotion of trading through social networks and the fact that we can make a purchase on Amazon, Apple, Google or PayPal in one click.

In 2012, I wrote an article entitled “The dawn of venture capital ”, which already described these trends, and in 2014 I published a presentation“ Why venture capital is most attractive ”, where new data on many of our past analytical studies were presented.

Fast forward three years, and what will we see on the horizon of 2016? It will be more likely the sunset of venture capital, in the sense of the sunset of days of rational behavior in this area. There is no one to blame for this recklessness - it is just that the laws of the market operate, and history does not teach us anything. The boom-decline cycle. The coolest companies appeared in the last stagnant period, and we all see how successful they are - Facebook, Twitter, Tesla and others. Prior to this, Google, Salesforce, and LinkedIn appeared among others.

Technology innovations enrich venture capital with new companies and contributions - this is the reward for investment partnerships to rediscover our asset class. Who to blame? These partnerships? Venture capital? Or a flood of new entrepreneurs and woeful entrepreneurs seeking fame and fortune? Neither one nor the other, nor the third. It’s the same as blaming the press for continuous reports about Donald Trump, and then, at the sight of Donald Trump’s rating in the debate, be surprised that the press is paying so much attention to him. The market is the market.

The modern private technology market is definitely in the bubble. According to Wikipedia, a bubble is

“trading in securities at prices substantially different from fair prices”.

Objections that, they say: "This time, startups bring real income," or that "market value is growing, then this is not a bubble," are unconvincing. And the definition of “price significantly different from the fair price” sounds quite convincing. The market gave us what investment guru Michael Moritz defined as “ second-rate unicorns (startups worth more than $ 1 billion).” How elegantly said.

Definition of a “bubble” from Investopedia :

“A jump in prices, more than justified by non-market factors, and usually appearing in a particular sector. It is usually followed by a drop in prices after the start of an active sale of financial instruments. ”

The jump in prices. More than justified. Usually in a specific sector. Let's take a closer look.

Last week I spoke at the annual Cendana conference on venture capital and investment partnerships. Cendana founder Michael Kim was one of the first to notice changes in venture capital that led to the seed stages of investing, and funded many of the best projects in the area. It is always a great honor to meet with such illustrious colleagues. Click here to download my presentation from the summit. Final venture outlook 2016 from Mark Suster

If the “market” stimulates price increases beyond the real value of the asset, then new players appear on the market who are not so rational in assessing actual prices — a number of non-venture funds, including corporate investors, hedge funds, crowdsourcing. Please note that I do not justify what is happening in the industry - in the field of venture capital. I just want to emphasize that price increases are closely related to outsiders. The graph below shows that 78% of rounds of financing for 80 companies worth over a billion dollars were conducted by non-business investors.

Although there are a lot of great companies, I doubt very much that there were 50 new companies worth a billion in the world in 18 months.

US $ 1 billion or more startupsSo that you better understand how quickly we created a “second-rate startup market” (as Michael Moritz calls it): over the past year and a half, in the US alone, the number of private companies engaged in new technologies and valued at more than a billion (which some already consider to be high ) grew from 30 to more than 80. Either we got magic beans and elixirs, or we rushed to our calculations. Below is a graph showing the average rating of private companies in the late stages of development compared to traditional rounds of financing for company development conducted by venture funds, as well as compared to open markets.

Late-stage evaluations of companies (round D, non-venture capital) are superficial and are dictated by the needs of outsiders (compared to round C conducted by venture funds). We can observe similar trends during the sowing rounds A and B, carried out using crowdfunding.

Medium priced, late stage private companies (SMT) Open markets are more adequate (US Tech ETF stocks from 1/7/12 to 30/6/15)

And after it is discovered what factors contributed to the increase in the members of the club of second-rate startups, then you can track the money that leads to a small number of sources. Firstly, corporate investors, including Google, Rakuten, Alibaba, Comcast, and others have increased their investment in enterprises, and they are often guided by not the same profit motives (and thus not the same pricing mechanisms) as traditional investors. This is not a damning statement or an accusation against corporate investors - just admit that there are often strategic reasons for investing in addition to those that are usually determined by the actions of a financial investor.

Corporations make up the majority of non-venture investors and pay less attention to valuations.

Non-venture presence in startups at intermediate and late stages of development

Perhaps the most interesting is the actions of mutual funds and hedge funds to penetrate the private capital market. As I wrote in the post Structural Changes in the Venture Capital Industry , private technology companies postpone the initial public offering, and thus private technology investors earn more until the actual public offering, and public investors feel the need to respond.

And what is the reaction?

Mature funds thumped money into companies that seemed to them the closest competitors of already public companies, and one informed person described this action as a simple “preliminary buying up of placed shares in order to become owners of shares after the companies become public.”

Round sizes reached unprecedented values, which is directly related to the lack of discipline in pricing. The

average size of rounds for startups at the intermediate and late stages of development by type of investor

In just two years, the average size of a round involving mutual funds has more than tripled, and the same phenomenon is observed in hedge funds. Therefore, we can say that a huge amount of money revolves around ecosystems in the late stages of development. This is good for entrepreneurs in fast-paced technology - isn't it? Is not it? Not so simple. It turns out that the company will have its Doomsday. They will either have to place their shares, or they will be bought by large companies, which are likely to be public themselves. Everything should return to square one.

Open market investors are not as stupid as private investors are trying to make them. Of course, they integrate protection mechanisms into their financial transactions, which allows them to avoid losses during the initial public offering if the price is lower than the price paid by them. So is the price they pay today for a company worth more than a billion? Does it really cost more than a billion dollars, or as Michael Moritz puts it, are we creating second-rate unicorns again?

Increasingly, companies sell at a price equal to or lower than their value according to the latest assessment of

12 transactions for the sale of shares with a total value of more than 12 billion in 2012

7 transactions for the sale of shares with a total value of more than 7 billion in the first half of 2015

As usual - the market gives us clues. In 3 out of 12 cases, investors sold their shares at a price lower than their value as estimated in the previous round. 25% discount sales? Sorry sight. But a year later, in 2015, 5 out of 7 sales were carried out at a lower price. I myself will calculate: this is already 71% of transactions.

And it’s difficult to make any forecast for 2016 without recognizing the role that crowdsourcing in the startup market is beginning to play. Over the past 2 years, we have seen an influx of high-tech companies funded through crowdsourcing platforms. Those who read this article, of course, know that AngelList is an undoubted leader and a platform worthy of all respect, but many new platforms have reached the world level. Funding through them only in the last 2 years has reached unprecedented heights, and increased from 400 million to 2.6 billion dollars.

Meanwhile, on the other side of the market - CAGR crowdfunding indicator over the past 2 years reached 153%.

The total amount of funds raised through crowdfunding around the world.

Of course, at first glance this will sound implausible, I myself read a lot of figurative statements on the topic of how dead venture capital is, and that it will soon be replaced by a gang of altruists - former founders who wake up the rain of investment on startups. The reality is more sophisticated.

For starters, conditions that are not offered to entrepreneurs with a convertible loan, much worse than the conditions offered by seed and venture funds, which are evaluated by companies, but only recently, entrepreneurs have started talking about this. Although these are trifles in comparison with the large-scale swindle of inexperienced investors that has begun. I openly warned about this for several years every time when it came to crowdfunding, but now the sell has become so obvious that even the Securities and Exchange Commission (SEC) should take a closer look at the activities of crowdfunding platforms.

I receive many letters from caring strangers describing a particular startup and urging them to invest as soon as possible, “before it's too late,” and at the same time convincing investors that they can enter into a deal only if they replenish the fund of the undersigned. I often saw transactions recommended by the platform, where even the most necessary information is not given, the study of which would temper, I think, the desire to invest.

Why not? The platform often charges fees. The platform does not bear the costs of maintaining the investment position. And what many do not understand is that many syndicates work according to the deal by deal scheme. For an investor, this means that if the transaction that he concluded is closed (and 49 more transactions are covered), then the management of the syndicate can still earn a lot of money on these 50 transactions, since he / she does not incur losses due to other failed transactions . Therefore, investment partnerships do not allow venture funds to work under a deal by deal.

The founders of the companies will pay for this short crowdfunding boom. In conditions when “every transaction is winning” and money flows in a river, they will receive their money through intermediary financing, but when the market will inevitably make its adjustments - who will carry out subsequent financing of these companies stranded? I understand that the final chords have not yet sounded, but they will sound.

What is my forecast for 2016?

1. I think that in 2016 the market for private technology companies will cool down, but I have been predicting this for 2 years, so hell knows. Although I know that markets are overvalued, but one in the field is not a warrior, i.e. one player cannot change market prices. That is why the scandal in the 38 Bin barwas just a distraction. I will continue to invest in the early stages in companies that will fundamentally change some aspects of the industry in an adequate period of time (8-12 + years). Soon, only cats will be born, and if it is not a bubble, money does not come immediately.

2. We will continue to observe excessive financing in the late stages of company development until the veil is overlooked, and then, according to my predictions, reasonable non-venture investors will return to their direct responsibilities and again begin to seek profits in other areas, and we - those who understands something in venture funds, we will continue to do our business.

3. The growth of crowdfunding as an equivalent alternative to venture capital will not decrease. Too much (relative to its value) capital will be directed into this direction until the next recession, when many inexperienced investors go broke, or until the SEC (Securities and Exchange Commission) begins to spread doubtful platforms or investors on these platforms. I suspect that this will happen after 2016, when retail investors get tired of waiting for easy money in the technology market.

4. In the meantime, technological progress will continue to evolve regardless of how many startups are evaluated there. Technology will continue to deeply influence society and industry, and grab ever larger pieces of the economic pie. And I suspect that for a long time, venture capital will play a decisive role in supporting great entrepreneurs.

I would like to thank my colleague Kevin Zheng for his tireless work in monitoring the trends of intermediary financing on behalf of Upfront Ventures. His work is invaluable, and if you follow him on Twitter, you will learn a lot of useful things.

Mark Saster is a partner at Upfront Ventures. He joined the company in 2007, after 8 years already working with Upfront Ventures as a two-front entrepreneur. Prior to joining Upfront, Mark served as vice president of production management at Salesforce.com, after the company was acquired by Koral, where he, in turn, was one of the founders and CEO. Prior to Koral, Mark ran his own firm, BuildOnline, a European software company (SaaS), which was subsequently acquired by the SWORD group. Mark is always looking for enthusiastic entrepreneurs to invest in projects in the early stages of technology development. His areas of interest include digital content and distribution, AdTech, consumer Internet technologies, and SaaS companies; Mark has impressive experience in this sector, given that he founded and sold two companies already. Follow the link to read his articles on his blogBoth Sides of the Table (“On Two Chairs”).

The original article can be read on the link on the AlwaysOn blog .