SoftBank Overtakes Toyota in Market Cap in Japan for First Time Since 2016

Amid the AI boom, SoftBank Group shares have surged, and founder Masayoshi Son's net worth has exceeded $100 billion. SoftBank became Japan's most valuable company, surpassing Toyota.

"Atlas Shrugged": How Masayoshi Son's SoftBank Buried Toyota and Ushered in the Era of Japanese AI

Analytical Note: Insights into the True Cost of SoftBank's "Coronation" and Why the Market Was Wrong a Second Time

June 4, 2026

Introduction

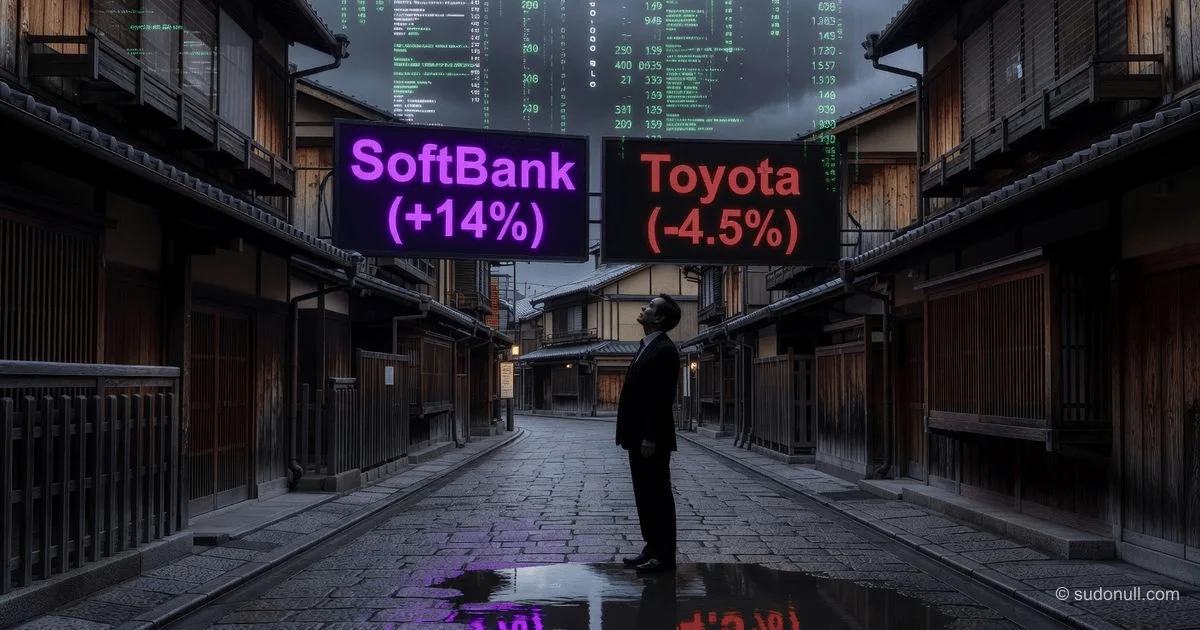

When SoftBank Group shares soared 14% on June 1, 2026, and its market capitalization overtook Toyota for the first time in 22 years, exceeding 48 trillion yen (about $305 billion), the world began talking about a "changing of the guard." And when Masayoshi Son's net worth crossed $100 billion a day later, returning him to the title of Asia's richest person, euphoria peaked.

But watching this spectacle from Tokyo, I recall the year 2000. Back then, the internet bubble also lifted SoftBank to the top of the Japanese market—briefly. And today, two days after the triumph, we already see SoftBank shares correcting 10% amid a global sell-off in the tech sector.

I have been closely following the Japanese stock market and Son's strategy since the WeWork era. And I assert: what we are seeing is not a "new Toyota." It is a "new Nokia" at the peak of hype. SoftBank today rests on three pillars: $100 billion in debt, a bet on OpenAI, and the belief that AI will be 50 times bigger than the internet. The problem is that two of these three pillars are phantoms. Let's break down why investors are celebrating a victory that may prove pyrrhic.

[The Core]: What Is Really Happening

Forget the nice story about a "changing of the guard." The core here is that the market has stopped valuing companies based on their current profits and started valuing them based on "holding the keys to the future." Toyota sells 10 million cars a year, has real factories, and generates cash flow. SoftBank has a stake in Arm, a check to OpenAI, and a promise to build data centers in France.

But there's a nuance: SoftBank does not officially manufacture chips, build AI models, or operate data centers. It is a financial intermediary that borrows money from banks (accumulating $100 billion in debt) and invests it in startups. A market cap of $305 billion is not a valuation of its assets, but a valuation of its ability to guess. In 2021, at the peak of the fintech boom, the same logic led SoftBank to $27 billion in losses.

The key point being overlooked: SoftBank became Japan's most valuable company largely due to expectations of an OpenAI IPO. Currently, SoftBank owns about 13% of OpenAI, having invested around $34.6 billion, and plans to increase its stake to 13% with investments up to $64.6 billion by October. But an OpenAI IPO is not a certainty; it's a hope. If it falls through or the valuation is lower than expected, SoftBank will be left with a liquid but not giant stake in a company that has yet to prove its ability to generate sustainable profits.

And finally, the geopolitical backdrop. The "Choice of France" with a €75 billion ($87.3 billion) investment in data centers is a brilliant PR move. But 5 GW of capacity by 2031 is not a revolution. It's roughly equivalent to five nuclear reactors. And it's more a signal to European regulators—"We're here, we're building, don't tax us"—than a real profit driver for the next five years.

Timeline and Context

To understand how fragile this "crown" is, we need to reconstruct the sequence of events of the past few days—they resemble a classic "pump and dump" scenario, albeit on a national economic scale.

Late May 2026: Son's net worth is estimated at "only" $56 billion. SoftBank's share growth over the year is impressive, but Toyota is still ahead.

May 31 - June 1, 2026: The turning point. At the "Choose France" summit in Paris, alongside President Macron, Son announces plans to invest up to €75 billion in French data centers. This is the largest foreign investment in France. The market explodes: SoftBank shares surge 14%, market cap reaches 48.8 trillion yen.

June 2, 2026: Euphoria continues. Market cap hits 49.3 trillion yen, and Forbes records Son's net worth at $100.4 billion. Analysts start talking about a "new era." But another fact stands out: on the same day, Toyota loses 4.5% amid rising oil prices due to the conflict in Iran. That is, SoftBank's victory is partly driven by its competitor's geopolitical troubles.

June 3, 2026: Key moment. A correction begins in the US tech market after a series of records. Nasdaq falls 0.9%. The Japanese market, unlike the US, trades with a lag. But the alarm bell has rung.

June 4, 2026 (now): Sell-off in Asia. SoftBank shares fall more than 10%. Investors are "taking profits" and starting to ask uncomfortable questions about debt and growth sustainability. Symbolically, on the same day, Kioxia (formerly a Toshiba division, in which SoftBank has a stake) briefly overtakes Toyota in market cap, taking second place. The market is in turmoil.

Who Wins and Who Loses

An analysis of the consequences of this market upheaval shows that the "winners" may be trapped, while the "losers" may be in a favorable position.

Winner #1: Masayoshi Son (personally). He has regained his status as Asia's investment king. A net worth of $100 billion is not just a number; it's leverage over partners and politicians. Every time Son enters a negotiation room for Vision Fund 3, he can now say, "I've put $100 billion of my own money on the line. What about you?"

Winner #2: Vision Fund 3. Investor confidence in the new fund (which Son announced earlier this year) has surged. Sovereign wealth funds from the Middle East, burned by WeWork, now see the Japanese "samurai" back on his horse. Capital inflows in the coming quarters could reach tens of billions.

Winner #3: France and Emmanuel Macron. €75 billion is a victory for French diplomacy. Macron gains an argument ahead of elections: "The world's largest investor believes in France." The creation of a 1 GW campus in Bosquel, partnerships with Schneider Electric and Sesterce—these are real jobs and technology.

Loser: Toyota shareholders. They are not to blame. Toyota is doing everything right: hybrids, hydrogen, electric vehicles. But the market is punishing the "old economy." Oil prices due to the war in Iran hurt car demand, and competition from BYD and Tesla squeezes margins. Toyota shareholders watch their "safe haven" turn into a "sinking ship" before their eyes.

Loser: Retail investors who bought at the peak. Buying SoftBank on June 1 on news from France and hopes for an OpenAI IPO is a classic "herd" mistake. As soon as euphoria fades (as we see today, June 4), the stock corrects. Those who entered at 14,000 yen and exited at 12,600 (a 10% drop) are left with losses while Son celebrates his $100 billion.

What the Media Isn't Saying

Now for what Forbes and Bloomberg are silent about, but what is known in private equity circles.

Insight #1: The "Golden Parachute" for OpenAI is an "Iron Anchor" for SoftBank.

SoftBank owns 13% of OpenAI. That sounds impressive. But the deal documents include a clause: if OpenAI fails to meet certain financial targets by 2028, SoftBank is obligated to buy out other investors' stakes at a predetermined price. This is called "downside protection" for OpenAI, but for SoftBank, it's an "abyss." If generative AI doesn't live up to expectations (and competition from Google, Meta, and Anthropic is growing), SoftBank could be left with a giant stake in a company worth three times less than at entry. And it will have to buy it out with hard cash.

Insight #2: The $100 Billion Debt Hasn't Gone Away.

SoftBank officially has about $100 billion in debt. That's a debt-to-equity ratio of about 2.5. To service this debt, SoftBank needs its portfolio companies to grow 15-20% annually. In 2025, it managed that thanks to Arm. But Arm is no longer a startup; it's a public company with limited potential for exponential growth. The next "unicorn" needs to deliver 10x in three years. With high key interest rates in the US and EU, finding such a startup is a tall order.

Insight #3: The "2000 Syndrome"—History Repeats.

In 2000, SoftBank was already Japan's most valuable company. Back then, it seemed the internet would change everything. And it did. But before that happened, the bubble burst, and SoftBank lost 99% of its market cap. Today, Son says, "AI will be 50 times bigger than the internet." That's true; AI will be huge. But the road to that future is littered with the corpses of companies that were overvalued in the moment. Right now, we look at AI in 2026 the same way we looked at Pets.com in 2000. The difference is that Pets.com didn't survive, but Amazon did. The question: Is SoftBank Amazon or Pets.com?

Forecast: Next 30 Days and 90 Days

Given the volatility that has already begun on June 4 and the upcoming OpenAI IPO, I see two scenarios.

Next 30 Days (July 2026):

Expect continued correction. SoftBank shares could pull back another 10-15% from current levels as global funds lock in profits after a six-month rally. Bad news from the US on inflation or the Fed rate will be a trigger. Good news: if the price falls low enough, Son will announce a share buyback to protect his $100 billion empire. This will create a local bottom.

Next 90 Days (September-October 2026):

The key moment is the official announcement of the OpenAI IPO date. According to SoftBank's plans, this should happen in Q4 2026. If confirmation comes in September that registration documents have been filed, SoftBank shares will soar another 20-30%, hitting new all-time highs. If the IPO is delayed due to regulatory issues (e.g., an antitrust investigation in the EU), panic will set in. SoftBank will lose its status as the "exclusive gateway to OpenAI" and fall 30-40%, ceding leadership to Toyota or even Kioxia.

The main risk I see: The "Iran factor." Oil prices are currently the main driver of Toyota's decline. But if the Middle East war expands, oil could rise to $150 per barrel. In that case, everyone suffers: Toyota (high fuel costs) and SoftBank (high inflation → high rates → flight from tech stocks). The correlation between them will become positive, and the "changing of the guard" will lose meaning because both will fall.

Summary: The change of leadership on the Tokyo Stock Exchange is not a victory for SoftBank. It's a diagnosis of the market. A diagnosis of "euphoria." As investors flee the real sector (autos, manufacturing) for the virtual (AI, data), they are creating a bubble. Elon Musk said, "The market punishes the patient and rewards the reckless—but only until recklessness becomes bankruptcy." Son's SoftBank is the biggest reckless player on the board. Time will tell whether his triumph becomes a legend or a death dance.

— Editorial Team

No comments yet.